All of you reading this article are educated but that does not mean that you are smart in investing your money. Why? Because the smarter you are the less risk you are willing to take… which is a good thing if you have a good paying job and a family to feed. And never be greedy because you will be punished by the universe…. seriously, most of the scam reports we read in the media are because many people get scammed simply because they were after fast & easy money and more importantly, are too lazy to educate themselves on scams.

Time flies, in a blink of an eye you will be 55 years old…… I know because I started blogging in my early forties and now I am already in my mid fifties. Many of you, my die hard followers, started reading my articles in your 20s or 30s while still a bachelor and now you have kids of your own.

Besides credit cards and fixed deposit promos to earn you FREE Money, over the years I have also influenced many who have extra money to invest in certain models of Rolex watches and Chanel Handbags so that they get to shiok sendiri and see the value of their Rolex watches and Chanel Handbag increase with time. You see, certain models of Rolex watches and Chanel Handbags are pretty good investment where they will appreciate in price beating the inflation rate….. it is just another form of wealth preservation but we get to enjoy it, haha.

But eventually all of us will come to the conclusion that money does not bring us happiness or having more does not make our lives any better. That’s why I started My Air Miles Project to enable those who have faith in me to experience First Class which most of us are too kedekut to pay for the ticket, haha.

Yes, money is the root cause of many problems/stress but money can also provide us with a pretty comfortable life.

In respect to the above, many are stressed from many angles….. That was why I had Project 0.0 Love & Gratitude and Project Health to improve the quality of life of those who once again had faith in me and many have thanked me for these projects as they are more meaningful than having money.

Like I said at the beginning, all of you reading this are educated and if you are a graduate with the right degree then you should be earning a pretty good salary, i.e. salaryman where we actually have less stress than the boss and we can fire the boss anytime we want.

If you are a boss, this article will also benefit you. Towards the later part of the article I will tell you what you should do in regards to EPF Contributions.

Like I mentioned, not everyone who is a graduate is good in investing their money. If you have a pretty good paying job and have no clues as to where to invest your money, then this article on EPF Contribution is great for you.

Over the years I have published many articles on EPF and recently FREE Money From The Rakyat To Your EPF Account (click here to read it) for the self-employed.

In the article mentioned above, I also mentioned about a super smart lady having close to RM2M in her EPF and she is still in her mid 30s and you will learn that she has been self-contributing in addition to the mandatory EPF contributions.

Well, yesterday (9th Dec 2025) a Sis messaged me to thank me for her and her husband’s recent First Class Emirates flight to Europe (Airbus A380 & Game Changer) and Singapore Airlines Suite Class London to Changi. And she then mentioned that she just read my article on EPF and would like to share that she had previously during Covid-era, increased her EPF Contribution by submitting Form 17 where the companies cannot reject. However, recently she reduced her contribution amount as she intended to clear her housing loan asap (which is a super smart move as I have been telling you all the Goal Of Life Is To Be Debt Free).

Detour a bit – to me the Flexi Housing Loan is a con-job by the bank to make the borrower remain in debt longer. And the joke is many think this Flexi Loan is actually good where the money deposited into a dedicated Savings Account will offset interest of the housing loan…. but eventually many will withdraw the money and burn it away! What this people don’t realise is that the money in the linked Savings Account gives them the false impression that they have savings to burn when in actual fact they are in debt!

In regards to the above said paragraphs, that is why I said the Sis is super smart as she wants to clear off her housing loan asap and get out of any debt.

Oh yes, if you have any credit cards Outstanding Balances which you are paying interest on, or even worse if you have Personal Loans, you can stop reading all my articles including credit card articles and instead cut your credit cards and clear off your debts.

Holy Cow, you know lah I am long winded…. back to the subject in hand – EPF Voluntary Contributions.

Before I go into EPF Voluntary Contributions, first we will touch on Mandatory EPF Contribution for Employee

EPF Mandatory Contribution for Employee & Employer

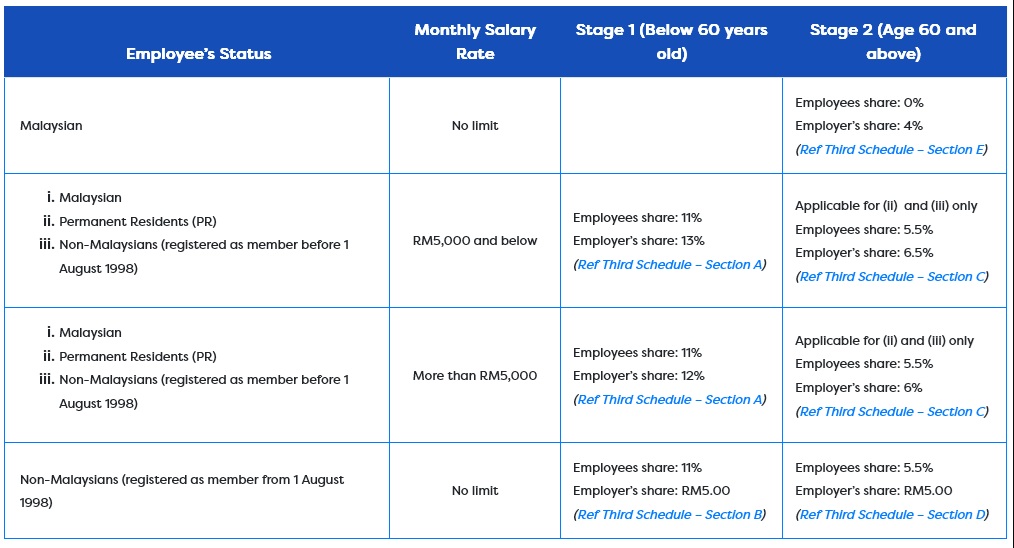

Below is a table from EPF which shows the rate of Contribution for both Employee and Employer:

From the above, all working people who are paid salary must contribute 11% of their monthly salary including bonuses. However for Employer, the rate can be ether 13% or 12% depending if the person is earning more or less than RM5K per month.

So, the above is straight forward.

Today it is very easy to check if your Employer has been paying the monthly EPF Contributions to your EPF Account. Just sign up for KWSP i-Akaun App and you will have all your EPF information at your fingertips. If you are near to an EPF Branch, you can sign up for the o-Akuan App instantly as your bio metrics will be verified on the spot.

Contributing More Than The Statutory Rate (Voluntary Excess)

You can contribute more than the Mandatory Contribution and it is very easy – it is termed as EPF Voluntary Excess.

What is EPF Voluntary Excess? So I asked uncle google:

From the above, you can voluntarily increase your EPF savings maximum up to RM100,000 per year

Below is from EPF webpage:

So, all you need to do is download the Borang KWSP 17A or 18A and submit to your HR Department and they must follow your instructions.

Click here to EPF Webpage on Voluntary Excess to download the form and read the User Guide

So How Much More Voluntary Excess Should You Contribute?

If you ask me, the more you contribute the better and the reasons are as follows:

No.1 – EPF has been paying higher dividends than FD Promo Rates

Below is once again reply from uncle google.

No.2 – Your savings in EPF are compounded!

If you are earning RM6K per month, the total amount that will be contributed to your EPF Account is RM1,380 per month (Employee 11% and Employer 12%) or RM16,560 per year (not including bonus).

Assuming you are earning RM6K per month and you increase you EPF Contribution to 20% (Statutory 11% and Voluntary Excess 9%), it means you will have total RM1,920 per month credited into your EPF Saving Account or RM23,040 per year (not including bonus).

With the difference from the 2 annual amounts above and EPF savings being compounded, it will make a huge difference in 10 and 20 years time! To make your life simple, below is a sample calculation assuming EPF will be paying 5% dividends yearly.

As you can observe from the above table, with 9% Voluntary Excess contribution, in 10, 20 and 25 years time you will have additional 39% more money!!!

Above is just a sample calculation as you should be earning more with time and thus you will have much more in your EPF; moreover the above did not include bonuses.

Here is a fact, as you get higher salary most will tend to spend more (some call it upgrading but to me we just need a comfortable place to sleep, good nutritious food to eat and a place to shit). So if we perform Voluntary Excess, we will have less income to burn on non-essential and non-durable goods and we will be forced to live within our means.

No.3 – With Account 3 You Can Suka-Suka Withdraw Your EPF Savings

Today 10% of your EPF Contributions will go into Account 3 which you can withdraw anytime!!! So you tell me, is it smarter to park your money in EPF versus Bank Deposit Products which pay you less in interest compared to EPF Dividends?

Also Account 2, you can withdraw for Education and once again going back to No.2 EPF Savings are Compounded, you will have more for your child’s education with Voluntary Excess contributions. I am not telling you to spend your retirement fund on your child but this EPF Voluntary Excess contribution can also be a form of saving for your child’s education…. and if your child pisses you off you can keep the money for yourself, haha.

Employer Can Also Contribute More To EPF

Once again, below is taken from EPF Webpage on Voluntary Excess and you will note that Employers (bottom right) can also contribute more than Statutory Contribution.

Some of you may recall, years ago I mentioned that instead of you getting a pay rise, ask your Employer to contribute more to your EPF because it is not taxable under income tax!

And if you own the company, it makes sense to pay yourself more via Employer Share! Moreover, the current government with effect from 1st January 2025 punishes investors by imposing 2% tax on company dividends.

EPF Self-Contribution

If you had read my previous article on EPF, you will also know that we can Self-Contribute to our EPF Account up to RM100K per year.

If you have funds parked in FD where you won’t be using anytime soon, I would think it is smarter to move your extra funds into EPF.

On the other hand, as for your monthly salary you should start now with Voluntary Excess as a form of forced savings so that you do not burn it on non-essential and non-durable goods.

BENEFITS OF EPF

Besides the dividends from your savings in EPF, there are many advantages which most people do not even consider and they are:

- You can nominate anyone as the beneficiary. To be exact more than 1 person and it cannot be contested. Even if your child is below the age of 18 years old, he/she can also be the sole nominee or with other people.

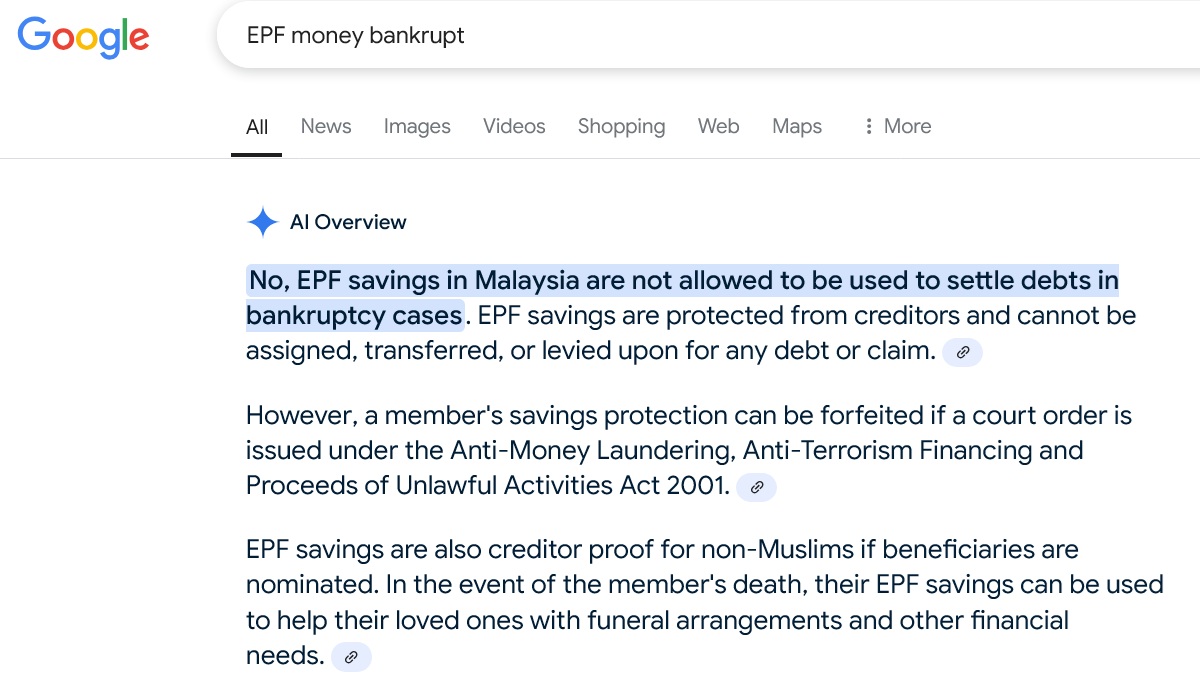

- Nobody can touch your money in EPF even if you are declared a bankrupt! Only a Court Order issued under the Money Laundering Act can forfeit your EPF Savings which should not be an issue for all of us law abiding citizens.

CONCLUSION

The Voluntary Excess contribution of course if not for everyone. If you have a housing loan you should clear it off asap so that you are no longer a slave to the banks. Now for the blur people, there is no point clearing of a car loan (hire purchase) as you won’t be saving any interest because Car Loans are just like Personal Loans where you become poorer the moment you sign on the dotted lines as the interest has been calculated upfront!

Today, with Akaun Fleksibel (Account3) where one can suka-suka withdraw his/her EPF money, it makes more sense to perform Voluntary Excess contribution so that one will still have more savings in the future after retirement even if one had to withdraw from Account 3 in the event of an emergency before the age of 50.

I tell you, you better start saving for your golden years and never rely on your child/children for support (you will be lucky if they don’t ask you for money).

With KWSP i-Akuan, we can perform withdrawals via the App, this one time I am going to tell you that you should never tell anyone, and I mean anyone your KWSP password. Nowadays it is very common that we hear that older people who are not familiar with mobile banking will ask a relative to assist them and eventually get conned by the relative!

EPF is your money and nobody should touch it so never tell anyone how much money you have in your EPF including your spouse! Because EPF is for the future when we retire and people around you can change with time…………….

You must be logged in to post a comment.