This is going to be a semi long rant. I would not pretend to know it all. But having talked to Gen X and Gen Y, there is an alarming amount of individual that do not kept a regular check on their Credit History. So let’s start with the basic again, what is credit history, why is it crucial to have one and the importance of maintaining a good credit score.

So how does bank knows if you have a good credit history?

Bank Negara maintains a list commonly known as Central Credit Reference Information System (CCRIS)

Banks and other financial institutions will each month submit to Bank Negara your repayment record. If you had never miss a payment, you get an egg. With each prompt payment, you accumulate more and more eggs each month. Therefore, Egg is Good!

If you start missing a payment, your Egg will hatch. First missed payment, you get 1 Chick, second missed payment you get 2 Chicks, third missed payment you get 3 Chicks, well you get my drift… So just remember, Chicks is Bad, Egg is Good. And you will be fine.

Other than CCRIS, there are also private credit reporting agencies that made it a business to keep track and sell your financial health info to interested parties. One of the more popular one is CTOS. They differentiate themselves by offering more information such as blacklist from non-financial institutions (telcos for example), CTOS Score, etc etc. They also allow easier access to your personal financial history without any delay from the comfort of your home, for a fee of course.

Keeping it clean

Starting your financial history usually starts with what could be the first “devil” in your life. Another loan…

Usually this happens when you began earning a steady income. But beginning from 2016 those taking PTPTN study loans will also get their repayment history submitted to CCRIS. Once you get the ball rolling, here comes the tricky part.

Maintaining a good financial history;

- Always observe your statement due dates. Paying one week ahead of the due date, just to be safe. Sometimes payment faced some problem that is out of your control. It would give you some leeway to resolve it. For some people this should be ok. Especially for those with low credit card usage. But if you want your history to look cleaner, read on below to understand how CCRIS inner works.

- If there is a dispute about outstanding payment, resolve it!! Don’t ignore and hope it goes away. It won’t and will likely come back to bite your ass. From time to time you can see a user dispute with telcos that ended up getting blacklisted in CTOS

- Don’t write bad cheques!! Always make sure there is adequate balance in your current account to clear the cheque.

- Apply only the credit card you need. Cancel the one you don’t use.

This is the ones I can think of so far… “You may suggest in the comments if you have a tip of your own to share.”

How early should I start be concern about my financial history?

I would say immediately after your own your first secured or unsecured loan (Car loan, Credit Card) or once you graduate (PTPTN repayment clock will start ticking 6 months after you graduate)

Understanding the inner working of CCRIS

As always, the devil is in the details. To make use of the system to your advantage, you need to understand a few basic mechanisms;

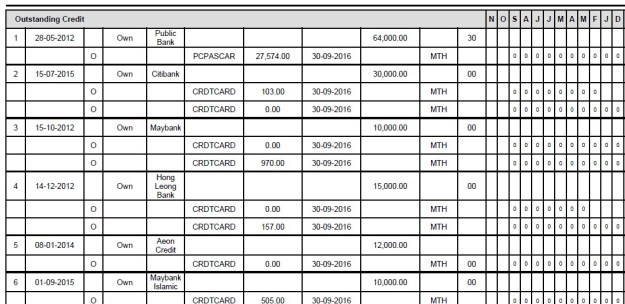

- Credit history is reported to CCRIS at the last day of each month.

- CCRIS will update their system with all the info on the 15th of following month

Why is this important to know?

Bank calculates your Debt Servicing Ratio (DSR) partly based on your outstanding as shown in CCRIS.

Example: If you were to pay only strictly based on the due date as stated in Rule 1 above, which may not be end of the month, in this example let say 13th of the month. Your statement says the payment due total is $5,000. You then pay it on the 6th of the month, a week ahead of the due. By the time CCRIS report is generated, it will show that your outstanding for that particular bank is still $5,000. This is because as of last day of the previous month, you still owe them $5,000 and this is what is reported to CCRIS.

But if you were to pay before the end of the month, this outstanding amount will be $0. As if you have not spend a single cent. Improving your DSR.

The same can also be said for not only statement balance but outstanding balance in general. Your statement might say $5,000 but then you made a big purchase worth $10,000 soon after the statement is out and now the total outstanding is $15,000. Paying only what is on the statement will still result in an outstanding balance of $10,000 at the end of the month. This $10,000 amount will still get reported and reflected in CCRIS. If you need your CCRIS to look clean come next 15th, you have to pay ALL outstanding by months end, not just the one in your statement.

Understanding this mechanism and timing your future loan application will make the system works to your advantage and not against you. Of course if you are not planning to take on any new loan, who cares…. as long as your egg don’t hatch, you will be fine.

Where do I get my credit history from?

I will share two most common sources,

- Direct from Bank Negara (http://creditbureau.bnm.gov.my/reportobtain.html)

- CTOS website (http://www.ctoscredit.com.my/)

Direct to Bank Negara is the best because it’s free. Who no like free things right? Just walk into any of their branch with your MyKad and print it out. Alternatively they also allow you to print a form online, fax or email it to them. They will then request some verification info and will you will get it once it is verified. This way is slow… very slow. In my experience it took at least 1 week.

My preferred way is via CTOS. Of course this is not free, as they run a business. Each new request is charged RM25. You simply register an account on their website, attach a copy of your identification card, and once the account is verified, you can start using it. Once a CTOS report is purchased, you may download that copy as many times as you want.

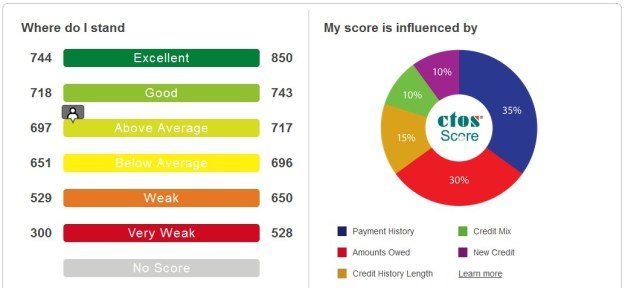

CTOS report will include your latest CCRIS, the CTOS own portion of the report, and the new CTOS Score. The score is a neat addition as it gave an idea of how well is our overall credit score. Remember it is only for your reference. Each bank still has their own credit scoring system which is unique only to them.

CTOS also provides some general guidelines to improve your score.

So confirm I can get that loan?

None of this will guarantee you will get that loan you desire. At best, it will signify that you are in good credit health and that you might be eligible to take on further commitment.

Each bank has their own way to asses a person’s credit worthiness. And there are other additional factors to take into account like your type of employment, your tax filing and payment history, etc etc…

So how often should I check?

I would say at least every 6 month. And definitely before you decide to make any large loan applications to make sure all your Eggs are still Eggs.

Conclusion

The world today has become more complex than what it was X years ago. Gone are the days where people can skip on their PTPTN loan and still buy million dollar houses. The days of our fathers and grandfathers securing easy cheap loans are long gone.

Tightening regulation by banks to curb another financial meltdown has made securing loans that actually matters, a much more challenging task. And yet bank still dangles easy access to quick personal loans and easy payments scheme to entice spending. Your only protection is constant education.

So if you know someone that is still clueless about this basic financial prudence, please encourage them to start caring.

A word of wisdom,

You can only help those that choose to help themselves

Posted by Jerie Lim