This article is for penyibuks who has nothing better to do and wishes to enter my sick imaginary grumpy old man’s mind. This article is rated XXXXXXXX and please leave immediately if you are below the Age of 18 and also if you are attached to money and want to take it to your grave.

Previously, in Wealth Preservation Part 1, I mentioned seven lessons which you should practice once you reach the level of Chiak Bui Liow.

Today in part 2, I will dwell on buying gold where you are not burning money but actually just changing one form of your assets to another form. For example, from imaginary value of your gold in a Bank’s Gold Savings Account you see on the computer screen to physical gold.

Converting Imaginary Money Seen On The Computer Screen To Physical Gold

I will tell you my case. Many years ago I bought gold via a Bank’s Gold Savings Account, I bought only once when gold was about close to RM190/gram (which was the high at that time!). Gold price then dipped and remained below RM180/gram for several years before it climbed up to above RM200/gram.

Here is the question related to my Gold Savings Account- did I lose money when gold price went below RM180/gram or did I make money when gold price went above RM200/gram?

Well, the answer to the above is the same as playing stock market or investing in a property where either I was hit with paper (today pixels on the computer screen) loss or gain…. nothing physical I can use to make my life any difference until I sell the stock or property and convert it to cash!

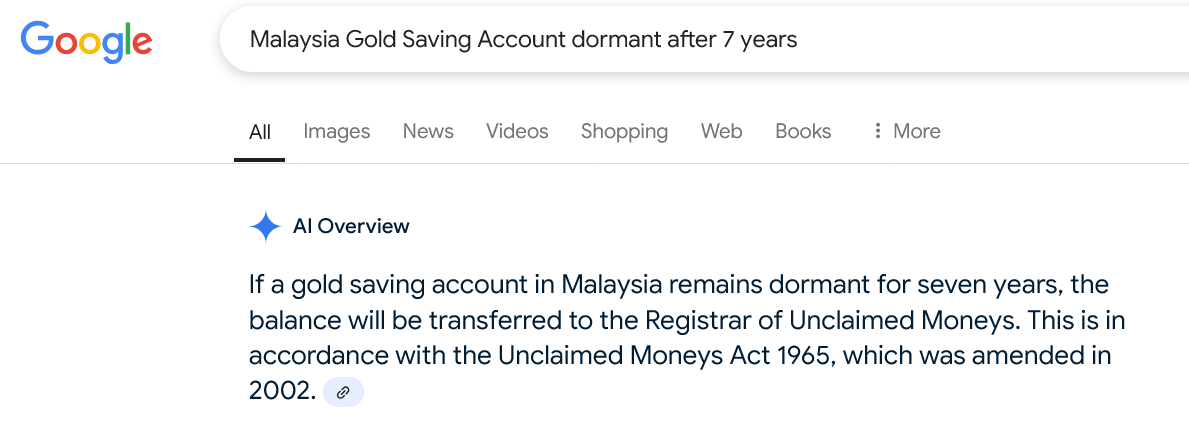

Gold price started to move above RM200/gram sometime after year 2019 and kept increasing but once again it made no difference to my life as long as I don’t sell the Gold in my Gold Savings Account and convert it to cash and use it to experience life! Actually my Gold Savings Account became DORMANT after a year because I did not perform any transaction. And if I were to leave the account dormant for 7 years, the money will then be transferred to the Registrar of Unclaimed Moneys!

YES! You better perform transactions with any banking products including Fixed Deposits which are auto renewed before Year 7!

For example, if you have a Fixed Deposit which is auto renewed together with interest, YOU SHOULD PHYSICALLY UPLIFT IT at Year 6 and place it back again so that the 7 years thingy does not come into play! However, if we playing/chasing after Fixed Deposit Promos, then we will not have this issue as we are constantly depositing into a new FD Promo.

What about Unit Trust you bought via a bank but did not perform any transactions for 7 years? For this you better ask your bank, as I don’t know.

In respect to the above, I thought I should highlight to you on the 7 Years thingy for FD and now I shall get back to GOLD.

So basically you have 3 main options to invest in Gold:

Option 1 – buy gold bars and put them in the safe box and never get to enjoy the gold unless you sell it.

Option 2 – buy and sell gold with Gold Savings Account but you better remember about the 7 Years thingy.

Option 3 – Buy gold pendants, necklaces, bracelets and bangles and enjoy it before you die.

All 3 options (not the only options as there are many other Gold Investment methods) do not guarantee you that you will make or lose money just like any other investment BUT with option 3 you get to enjoy wearing the gold jewellery while you are alive (when you are dead it makes no difference if you had RM1 or RM1,000,000,000,000,000.00 or 1 ton of physical gold).

So coming back to my Gold Savings Account, before the seventh year I had to perform a transaction where I withdrew 5 grams to reactivate the account. But today this said account is dormant again as I have not made any transactions since years ago, haha.

Today Spot Gold price is about RM380/gram which means technically I have made 100% from my initial purchase of gold with the Gold Savings Account more than 10 years ago.

Is 100% returns in 10 years good? Well, to answer this question I shall deposit RM100K into FD/EPF and assuming that the interest rate remains constant at 4% to 6% for the next 10 years, let us see how much would the FD be in 10 years time?

So for the amount to double (RM100K to RM200K) in 10 years, the COMPOUNDING interest rate should be about 7% per year.

In other words, I have been getting about 7% p.a. compound interest rate. from my Gold Savings Account! Way better than FD/EPF but who knew 10 years ago that Gold will appreciate 100% in x number of years!!!

So what is the point of the above paragraphs? Well, like I mentioned in Wealth Preservation Part I – you should invest 10% of your assets into other riskier investments and never put all your eggs in one basket. As for Magic The Gathering cards, a selected few may appreciate more than 100,000% in 20 years!

Now, if you ask me if Gold or Bitcoin or Share Market can appreciate 100% in x numbers of years from now….. my answer is I don’t know. If I can tell you the answer than I am either God or I have traveled into the future and returned back.

However, I have learned not to be greedy…… and my Gold Investment had appreciated 100% and I should take profit. So if I were to sell 50% of the Gold in my Gold Savings Account, it means whatever amount remaining is totally FREE! Yes this is what I am going to do, i.e. sell 50% of the value in my Gold Savings Account to realise profit.

And since whatever that is remaining in my Gold Savings Account is pure profit, i.e. FREE money, it makes no difference to me if the amount should go down or up. If it goes down I won’t be losing money from my Gold Investment since I have taken out the Principal Sum (not considering inflation). If Gold price goes up another 100%, I have more FREE money 🙂

And once I withdraw part of the Gold in my Gold Savings Account, I have another 7 years to perform another transaction before the 7 years thingy comes into effect.

Now in order to preserve my wealth or transferring my wealth to my daughters, instead of burning the money from the Gold I sold from my Gold Savings Account on non-durable stuff (e.g. smartphone, car, makan and holidays), I will use the money to buy Gold Jewellery which has value! Therefore, in other words I am just converting the Imaginary Gold Value in my Gold Savings Account to Physical Gold which can be enjoyed! And since I am buying the Gold Jewellery for my wife and daughters while I am still alive, I get to hear them say thank you and they will remember me as a generous dad.

Same thing, if you have RM1,000,000.00, go lah buy gold jewellery…. up to RM100K worth of Gold Jewellery (999 24 karat, 916 22 karat, Tiffany or VCA all have value) which is 10% of your assets is actually insignificant! I will tell you why, you place RM900,000.00 into FD earning you 3.3% and buy RM100K worth of gold jewellery, in 3 years time your assets (Cash in FD and Gold Value) 101% will be more than RM1M!

If you do not understand the above paragraphs where technically your actual assets did not change but increase and yet you feel you are burning money on gold jewellery then most probably you get joy from seeing the “amount of money” you have on your computer screen, which is fine as long as you are alive but if there is a nuclear war or internet kaput or Godzilla emerges or we are attacked by aliens or a new Disease X like Covid-19/Spanish Flu (all these scenario are possible including Godzilla but the form may not be what we see in the movies) then you will regret not buying physical gold for your loved ones when you still can hear them say thank you and most importantly the physical gold can be exchange for food during time of chaos for your survival.

The point of the above paragraphs is that once you reach the level of chiak bui liow (i.e. you have more than enough money to survive until the day you die), you can still preserve your wealth by transferring it to your loved ones and hear them say thank you. BUT you must also understand once you give part of your wealth to you loved ones, it is no longer yours and your loved ones can do anything with it!

FYI, spot gold is traded in USD, therefore if USD strengthen against MYR, then gold will be worth more if the spot rate remains constant. Like wise, if MYR strengthen against USD and gold spot rate remains constant, then gold price in MYR will drop! But because gold is traded in USD, basically today gold can be converted to any currency and that is why you can convert your physical gold to cash anywhere on earth.

Landed Freehold Property

I want to revisit the earlier excel calculation, shown again below:

In respect to the 4% interest shown above, say you bought a house with cash for RM500K, after 18 years if you do not sell the property for RM1M or above it is damn stupid right because you would have RM1M if you had deposited the money in FD (assuming you get constant 4% interest)! If you take a loan then effectively your cost will be higher and you may need to sell the property much much higher than RM1M.

What is the point of the above paragraph? It is to tell you that FD is an excellent method to preserve your wealth as it is (1) tax free for individuals, (2) headache free, (3) you have cash to do anything you want including paying for your hospital bills, funeral and burial plot! HOWEVER, if MYR weakens then we will be fools loving FDs deposited in RM currency, hahaha.

So if anyone tells you that FD is stupid, I can tell you that person has not reached the level of chiak bui liow and most probably is trying to sell you something for his/her own interest and not yours.

Once again, the point is never put all your eggs in one basket which means you should diversify and have many different types of assets as we do not know what the future holds.

Even the Thai PM has properties in UK and Japan, watches and handbags besides cash and other assets in Thai Baht – click here to read 200 handbags, 75 watches, and $400 million in luxury assets: Know how rich Thailand’s PM is?

Now now, don’t suka-suka go buy apartments anywhere on earth including in Malaysia for the sake of investment. Many investing in apartments in City of Melbourne are experiencing loses and if they had bought when AUD/MYR was 3.4 more than 10 years ago, most probably they be worst off because today AUD/MYR is about 2.8!!!! Then again we never know the future……..

Like I mentioned in Wealth Preservation Part I, there are risk associated in investing in anything including physical gold (wearable and liquid) and properties (non-movable and non-liquid) but generally it is good to have gold plus one or two or more FREE hold landed properties where there is demand (location, location, location) as a method of wealth preservation as the value will increase because of INFLATION.

Once again, never put all your eggs in one baskets but have many ways to preserve your wealth and if one investment goes kaput you can still sleep soundly.

And when you are old, don’t be attached to the properties you have but sell one or more and convert it to cash so that you live the remaining life you have in comfort where you can go anywhere you want (employ a driver) and/or eat anything you want (at any restaurant where money is no issue) and/or buy your medication from any pharmacy that is most convenient and/or go to any hospital you want and/or chose the best burial plot with good feng shui.

Long ago in my Children Education Path series, I mentioned if we send our child/children overseas for their education, there is a big possibility that the child/children will start their career and family overseas leaving us all lonely in our old age. If this was to be the case, it means the child is no longer serving you or your spouse and your child/children can survive without you. If this was to be the case, don’t be stupid by not selling your properties/non-liquid asserts and allowing your child/children who don’t give a damn about you suffering in silence in your old age to inherit all your assets but instead convert your non-liquid assets to cash and enjoy life in a luxury nursing home!

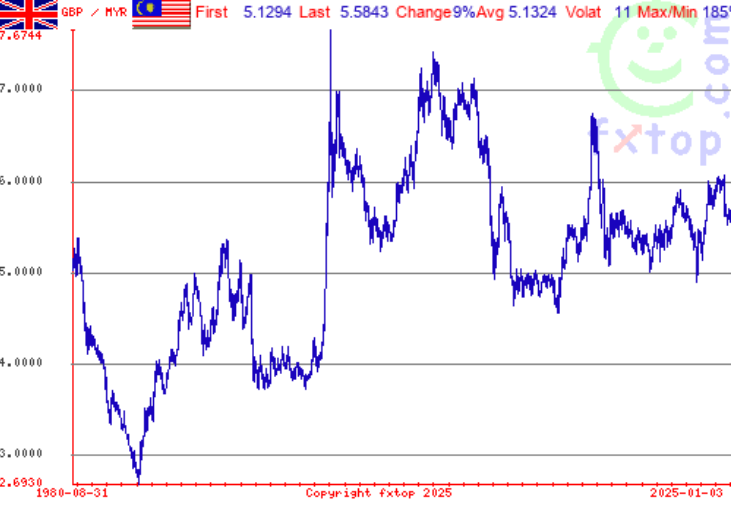

Below are some charts starting from 1980 for your info:

If you refer to above chart AUD/MYR, well AUD/MYR today is close to early 80s!!! Question is how low can AUD/MYR go? Nobody knows!

Now see Gold price below – it generally increased over time regardless of what currency! Then again no one can guarantee you that gold price cannot collapse back to before year 2000 price!

Last but not least click here to read Rolex hikes prices for gold watches

Prior to covid era, the Yellow Gold Rolex President shown below was selling for less than RM150K. Today Rolex Gold President Watch cost close to RM200K or more….. almost enough to get a new Entry Level Mercedes Benz!