If you are a follower of mine for years, this tutorial on FD will be kind of useless to you. However if you are new to GenX GenY GenZ and would like to invest/park your money in Fixed Deposit or Term Deposit, then you have come to the right place.

Then again, if you are a long time follower of mine, you will know that the contents of my articles may not necessary reflect the title; and since I am freaking long winded, I will end up telling you this and that which has nothing to do with the title, hahaha.

Why Park Your Money In Fixed Deposit?

- Fixed Deposit or Term Deposit pays higher interest rate compared to Savings Account.

- You can choose the tenure as to how long you want to park your money in FD starting from 1 month. However most banks require placement of RM5K for 1 month FD. The good news is for 2 months and above tenures, you only need to deposit RM500.

- Once you placed a Fixed Deposit (to be exact today many banks call it Conventional), the interest rate is guaranteed. What this means is that the interest you earn from the Principal Sum will not vary but guaranteed, you cannot lose money (the bank collapse is a different story). However please note that Islamic Banking Term Deposit may not be necessary so, please read the TnC of the Islamic Product you are interested in. Also take note that there is another product called Step Up FD where the interest rate can also go up or down depending on OPR.

- FD is as good as cash where you have access to your money instantly anytime and with online banking it is really anytime day or night. However if you uplift/withdraw before the maturity date, you may not earn any interest but will still 101% get back the Principal Sum.

- Fixed Deposits are insured by PIDM per account per bank up to RM250K. Google Perbadanan Insurans Deposit Malaysia for more info. However there are some Islamic Banking products similar to Term Deposit which are not covered by PIDM, so read the TnC and do not assume anything.

- And best of all, FD interest are compounded! This is where many people do not understand the magic of compound interest and are conned by salespeople claiming that their products (including bank and insurance products) offer higher interest rate compared to saving your money in the bank! In respect to this paragraph, you are to go and educate yourself on compound interest and risk of a product plus any fees so that you are not conned by Sales Personals and especially Insurance Agents that their products are more superior than banking products. However I will tell you this, most non-bank Savings products have fees which the agent never tells you, example Unit Trust or Mutual Fund or Insurance Funds……. I am not stating that Unit Trusts or Insurance Products are not good (as it depends on your needs) but I am pointing out that you are imposed fees.

- There is technically no limit as to how much you can place in FD (either in 1 bank or many banks) and the interest is tax free (for personal accounts)!

- We can have Joint FD Account. To me this is extremely important because if anything happens to the other party, either one can withdrawn the money. All my FDs are Joint Accounts except for my eFD purely to park money to pay my credit cards.

Magic of Compound Interest

Say you deposit RM100K into 12 months FD at current Board Rate of 2.8% p.a. (Maybank’s Board Rate for 12 months FD as of 10th Jan 2024).

After the 12 months, you would have earned interest of RM2,800 and your Principal Sum becomes RM102,800 if you renew the same FD (Principal Sum + Interest) which has matured.

Assuming you do not uplift the above said FD and let it continue to be reinvested/renewed, at the end of 10 years you would have RM131,804.78 if the interest rate maintains at 2.8%. If the interest rate increase then you would have more but then again interest rate fluctuates and can even go down.

And if you still continue for another 10 years assuming the interest rate maintains at 2.8%, your FD Amount would balloon to RM168,993.18

OR let’s say you deposit RM12K per year into Fixed Deposit which is equivalent to RM1K per month:

Say you deposit RM12K on 10th January 2024 into a 12 months FD at interest rate of 2.8%. Come 10th January 2025 you would have earned RM336. And then you add another RM12K to the amount you already have, your new Principal Sum will now be revised to RM24,336 (Original Principal Sum RM12,000 + Interest Earned RM336 + New Deposit RM12,000).

You continue depositing RM12K per year into the above mentioned FD and assuming the interest rate maintains at 2.8%, you would have RM152,122.75 and RM315.964.24 on the 10th year and 20th year respectively!

Once again above is you only depositing like RM1K per month into a FD that pays 2.8% interest rate. If you deposit RM30K per year into FD (equivalent to RM2.5K per month), you would have RM789,910.60 in FD in 20 years time!

Another important thing about Fixed Deposit is that for personal FD accounts, whatever interest you earn are all tax free (unless the government change it).

And the most important thing of all is that Fixed Deposit is almost risk free with PIDM – not totally risk free but one of the lowest risk investment where the interest rate is guaranteed – i.e. you can hardly lose money with FD unlike Unit Trust or Share Market.

Same case with EPF dividends, they are tax free too. However we do not know how much yearly dividend we will earn from the money we have in EPF until EPF announces it. However there is one major advantage that EPF has over FD – even if you bankrupt or you die, the money is guaranteed to be transferred to your nominee(s) and nobody else.

My advice to you is, you must save money in both EPF and FD for your retirement years. The biggest mistake I think that most people do is that they withdraw periodically their EPF to pay their monthly housing loan. Well, when you retire and have no income, if you only have one house/property, you can’t sell it to have cash so you have money to eat and pay medical bills! Fact – you need to save for your retirement years unless you have guaranteed passive income.

The average lifespan of Malaysians have been increasing and now stands at about 75+ years old. If you die 5 years after you retire at at 65, then I guess you do not need much money BUT what if you live until 100 years old! I tell you, you better start saving now so that you have enough funds to have a comfortable life until 100 years old.

However, some Financial Advisor/Consultant will tell you that FD interest rate can’t beat inflation, that may or may not be true BUT one thing for sure is that the interest rate from FD can’t keep up with the weakening Ringgit! The thing is, when you are young, you can take risk, especially if you do not have children (which is a liability) and can invest in higher risk investments (share market or unit trust) compared to FD. But after your retirement where you do not have much income and have limited funds to survive to 100 years old, I would think you should not be taking much risk but ensure you have money till the day you die! Same thing if your child is about to enter university, you have to ensure you have money in your hands to send him/her to the best uni on earth and can’t be taking much risk.

As for investing in properties, I won’t touch it in this article except to say that if you have less than 3 landed properties when you are old (above 75 years old which is above the average which means anytime you can die) – sell one or 2 of them and enjoy life instead of living like a poor man relying on the rental income! Well you may say you don’t need much money when you are old as your expenses should be nominal – well let me tell you, when you are old, you need a lot of money on standby in the event you are hospitalized and need money to survive in the ICU! And don’t forget there are also your funeral cost and if you want to be buried you need money for the land too. This is where the Joint FD comes into play where the other party has access to your funds.

OMG! I detoured from FD!!! Back to the subject on FD.

Why You Should Chase After FD Promos if you have more than RM10K to deposit a year.

Today, we can get Fixed Deposit Promos offering interest rate as high as 4% p.a. for 12 month tenure compared to Board Rate of around 2.7% to 2.8%.

Assuming you can get a 12 Months FD offering 3.8% Promo Interest Rate and you have RM100K to deposit, this means you are earning RM1K buta money over Board Rate!!!

Case 1

So once again, assuming you have a one time off RM100K to place into a 12 months FD Promo offering 3.8% and assuming the interest rate maintains at 3.8% for the next 20 years, what this means is that at the end of the 10th and 20th year, you would have RM145,202.31 and RM203,118,61 respectively.

Let’s compare 2.8% (12 months FD Board Rate) versus 3.8% (12 months FD Promo Rate).

Assuming you deposit an initial RM100K only.

At the end of 20 years, you will have RM168,993.18 if the interest rate remains at 2.8% versus RM203,118.61 for FD Promo offering interest rate of 3.8% for 20 years too.

The above difference is RM34,125.43 FREE Money!

Case 2

Assuming you deposit RM12K per year into a FD Promo offering 3.8% interest rate, at the end of 20 years, you would have a total of RM350,011.95 versus RM315,964.24 the earlier example where the interest rate was 2.8%

With respect to the above said paragraph, the difference is RM34,047.71 additional money.

FD interest rate can go as high as more than 10%, no joke.

See table below which was posted by a Bro back in 2012 at LYN FD Forum which I was quite active back then haha.

From the above chart, it can be observed that between 1996 and 2011:

- EPF dividends except for 1 year is higher than FD interest rate; and

- Inflation is lower than FD Interest Rate except for 2008!!!

For the last 10 years or so, FD Interest Rate has been hovering around 3% and 4% for Board Rate and Promo Rate respectively except for years 2020 to 2022 where it was lower than 3% even for FD Promo rates.

As for inflation rate in Malaysia, I tell you it is meaningless as many essential stuff/food are either subsidized or price controlled. But all of us know that the price of eggs was one stage damn high last year and today RM100 can’t buy us much at the grocer. And if you have been reading my articles, you will know that Chanel Classic Double Flap handbags has risen close to 100% since pre-covid!!! When Apple iPhone was first launched it was about RM2.5K (I know because I bought it for my daughter) but today a new iPhone cost RM4.5K!!! So it is not only inflation that we should be worried but we should be more concern that our Ringgit weakening over time plus new taxes and removal of subsidies.

One thing I can tell you is, if you are a bachelor, it may be worthwhile to go work in Singapore for a few years especially if you can earn more than SGD10K (you have to consider rental in SG which is damn high); BUT if you have schooling children and you want to bring them over with you, then you better be earning freaking damn high because you may need to send your children to International School and eventually end up with no savings!

Once upon a time SGD1 = MYR1. Today SGD1 = almost RM3.5!!!

With the above, I hope you understand why it is a smarter move to chase after FD Promos, especially if you have substantial amount to deposit into FD; because you will earn more in the long term. And if you are into online banking, there is practically no extra cost (e.g. parking) or wasting time at the bank by you placing your money in a FD Promo versus happily going with Board Rates and end up earning less. Once again, there is no limit as to how much you can deposit into FD and guaranteed not to lose a sen.

Also you can deposit into Foreign Currency FD Accounts; but you must also know that Ringgit may also strengthen again US Dollar or other currencies and I do not know the future short or long term.

OMG again!!! I detoured from the subject in hand – back to FD.

WARNING – Inactive Account

In Malaysia, if you do not have any activity with any bank products (e.g. Savings, Current, FD and even Gold Investment Account and etc), after 7 years it will be transferred to Jabatan Akauntan Negara Malaysia! FYI, you can easily check if you or your loved ones have any money with Jabatan Akauntan Negara Malaysia by visiting the link below:

Now read carefully, for Fixed Deposit or Term Deposit where you have instructed auto-renewal for your FD/TD Account, it is best that you uplift/withdraw the FD at the 5th or 6th year from the date you made the initial placement to ensure that your money is not transferred to Jabatan Akauntan Negara Malaysia!!!

What the above means is, on the 5th or 6th year on the day of your FD Maturity Date, uplift the FD and transfer the money to your Savings Account and then you can immediately again placed a new FD. Get it? If you don’t get it ask the bank officer to explain until you get it. Once again this also applies to Gold/Silver Investment Account.

BUT if you are chasing after FD Promo to earn more in interest rate, you do not need to worry about the above 7 years nonsense because you will be placing a new FD every time!

You see, for years, in order to be eligible for FD Promo Interest Rate you need Fresh Fund and not auto renew. However if you are a high net-worth client, your Relationship Manager can seek approval from HQ for you without needing to satisfy the Fresh Fund condition.

How To Transform Your Existing FD Fund Into Fresh Fund

Please note for FD Promo, in addition to Fresh Fund, in order to be eligible most banks also require a minimum deposit.

Option 1 – for old timers like me who still has a Checking/Current Account where I can issue cheque.

Step 1 – On the FD Maturity Date, go to the bank (we will call it Bank A) in the morning and uplift the FD and transfer the money to a Savings or Current Account.

Step 2 – Then perform Interbank Giro from Bank A to Bank B (which you have a Current Account and can write cheque).

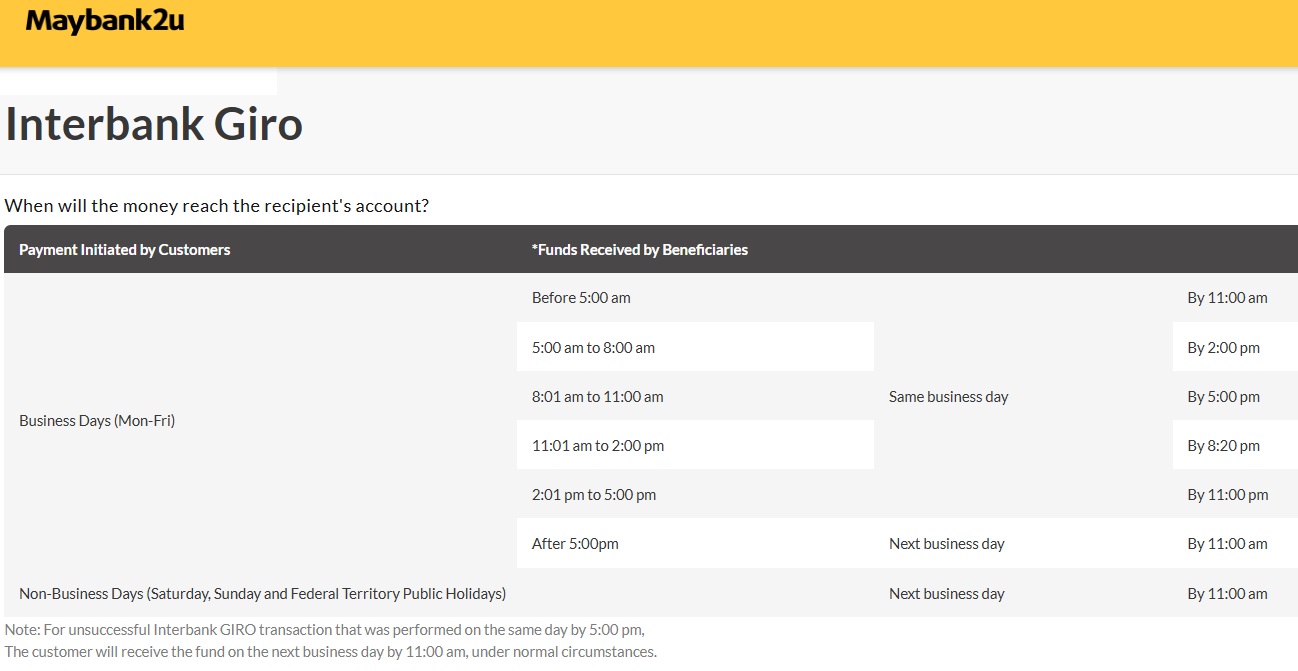

Below is the time line for Interbank Giro from M2U:

In respect to the above image, what it means is that the money will be credited into Bank B on the same day if you personally go to the bank and perform the transfer before 4pm (most banks’ closing time).

Step 3 – After you performed the Interbank Giro (up to RM1M per transaction) from Bank A to Bank B, you immediately write a cheque from Bank B and make a new FD Promo placement to enjoy the FD Promo Interest Rate 🙂

If you have a current account, you will know that the cheque from Bank B won’t be cleared on the same day; therefore you have nothing to worry about.

Option 2 – For People Who Prefer Online Banking.

Step 1 – Uplift the Matured FD (say in Bank C) on Maturity Date to your Savings Account if you have instructed Auto-Renew. If you have instructed that the Principal Sum and Interest from the FD be credited into your Savings Account upon maturity then you do not need to do this Step 1.

Step 2 – Duit Now the money in your Savings Account to another Bank (say Bank D).

Step 3 – If Bank D is offering better FD Promo Rate than Bank C, then just pace a new eFD with Bank D.

Step 4 – However, if Bank C’s FD Promo Rate is the best or you only want to place FD with Bank C, then all you need to do is perform Duit Now back to Back D and the money credited will be considered as Fresh Fund 🙂

My Recent Case

Case 1 – My Son

My son who is overseas has a Joint FD with me at UOB and his FD matured on 3rd Jan 2024 but I only returned back to Malaysia on 7th January 2024. So the FD was auto-renewed at Board Rate of 2.7% for 12 months tenure.

FYI, UOB does not offer eFD and therefore I need to go to the bank personally to get the FD Promo Rate of 3.75%.

Like I showed you, FD Promo interest rate is way better and thus we can earn more. So I decided to uplift my son’s FD and lose a few Ringgit (less than RM100) and place the money into a FD Promo and earn more than RM500 extra FREE money!

But it was close to 3pm when I decided to do the above and therefore decided to uplift the UOB FD online and transfer the money to my Maybank Current Account. Please note I can perform Option 1 mentioned above where I go to the bank in the Morning and transfer the money via Giro but I thought I save some time at UOB on paperwork by transferring the money to another bank a day earlier).

But then only I found out that UOB Daily Duit Now Transfer for personal account via online was only RM50K!!!

So I contacted my UOB Relationship Manager and she taught me that we can transfer RM50K via Duit Now and another RM50K via Giro 🙂 What this means is I can transfer up to RM100K online from my UOB account to another bank 🙂

I did the above, i.e. first I uplifted the FD online with my own Online Banking Account (UOB now can uplift FD online) and had the money credited into our Joint Savings Account. Then I transferred the money in the Joint Savings Account via both Duit Now and GIRO to my Maybank Current Account. The money that was transferred via Duit Now was instantly credited into my Maybank Current Account and the Giro a bit later but on the same day.

Then the next day I wrote a Cheque from my Maybank Current Account and went to UOB Branch to make a new placement with FD Promo to earn extra FREE Money.

I tell you the above method (uplifting the FD and transferring the fund to another bank) was so much quicker where I saved a few steps on paper work (i.e. uplifting the FD at the Branch and then have it transferred to the Joint Account and then GIRO out).

Case 2 – My daughter

For my daughter’s case, she also had more than RM50K. So she transferred part of the matured FD fund from her own Personal UOB Online Account (which means she has a separate daily limit as I have almost used up my limits) to her CIMB Savings Account via Duit Now and the remaining via GIRO to my Maybank Current Account.

The next day, she transferred back the money from CIMB to UOB and the money would be considered as Fresh Fund. She followed me to UOB to make 2 FD Promo Placements – one with the money transferred from CIMB into a single name FD and another with my Maybank Cheque for a Joint FD.

CONCLUSION

As I have shown there are many advantages to have a FD. To me the most important thing is that I can have Joint FD Accounts with my wife and children where anyone can withdraw the money; thus ensuring that my wife has access to money if something happens to me.

Also by placing the FD over the counter, there will be a paper trail which is extremely important in the event my loved ones need to go to court to gain access to their inheritance.

I have mentioned many times before, if you place eFD, there is no paper trail (if you did not print it out) and in the event you die, your loved ones not only have no access to your Online Banking (as you were so secretive in guarding your password) but they also can’t submit the bank account number to the court to get access to the money you left behind!

Once again, I still had to go to UOB for the Promo FD and the reason why I did not go to the bank and perform online transfer at home was because by the time I decided to uplift my son’s FD it was close to 3pm. If I had remembered about his FD in the morning I would have gone to the bank and perform Option 1 above.

I did not know that the Daily Limits to transfer fund via Duit Now and GIRO was RM50K each. I thought it could be as high as RM200K. Luckily I contacted my Relationship Manager at UOB and she told me that Duit Now and GIRO has separate Daily Limits which means we can transfer up to RM100K online per day. For amount more than RM100K per day, we will need to go to the bank, as I mentioned, GIRO limit is RM1,000,000.00 per transaction at the bank.

This article is mainly for UOB customers and also previous Citibank Customers because UOB does not offer eFD.

On the other hand, RHB and HLB do offer very competitive eFD Promos – which means if you have both these accounts, you can easily switch between them to enjoy the higher interest rate without needing to go to the bank. AND the best part is these banks you can transfer RM200K via FPX.

Below is HLB Promo and the steps to transfer via FPX.

Last but not least, if you are still reading this, it means you are educated and if you have the right degree and/or attitude, your income would increase at an exponential rate as you progress up your career. I have shown you that by you depositing regularly/periodically into FD, you would have saved a substantial sum in just 20 years only. So if you continue to be discipline and regularly/periodically deposit money into FD and not burned your money on materialistic stuff or taking frequent overseas holidays or into the standard vices (i.e. Asian Dolls, Toy Boys, Gambling and Drugs) PLUS your other investments and combine with the money in EPF, you will be freaking rich and not having to worry about money when you retire.

Of course there are many ways to make much more money than depositing in FD, the higher the risk the better the returns but it also means you can lose more too….. it all depends on your risk tolerance but I will tell you this, make sure you can sleep soundly when you invest your money then you are doing alright 🙂

And if you really want more pocket money, you can be a Grab Driver instead of wasting time lazying around doing nothing…… and you have to do it now because very soon Grab Drivers will be history with driver-less cars/taxis.

You must be logged in to post a comment.