Last Update: 21 May 2018 – Maybank

Just as expected, around this time of the year, many credit card issuers would have made announcements informing their card holders that they are revising their card benefits and/or inflating their reward redemption program.

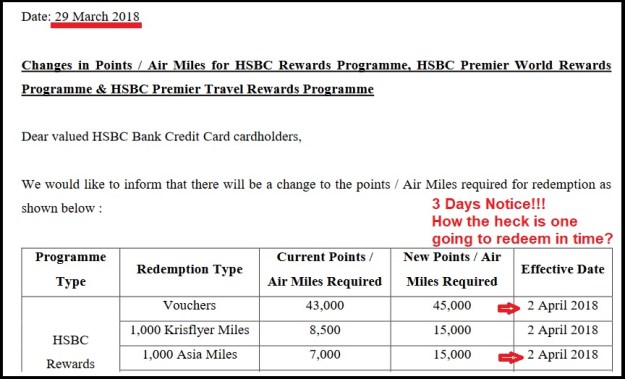

However, unlike western banks (i.e. HSBC), our local banks are more sincere where they will give us adequate time to redeem our reward points before their inflated reward redemption comes into effect.

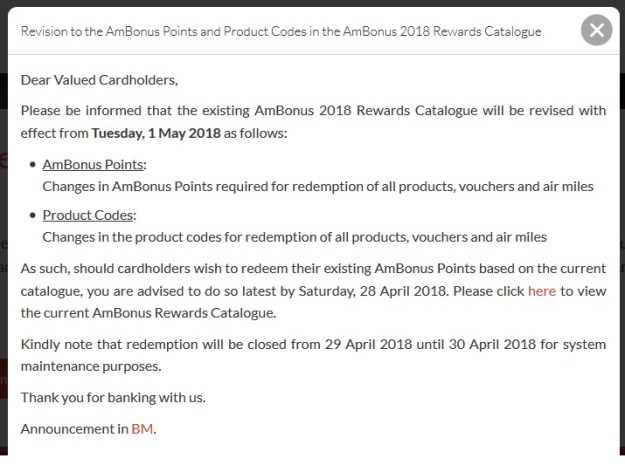

For example, on 5th April 2018, AmBank announced to its customers that they are revising the reward redemption effective 1 May 2018. Thus giving ample notice to their customers unlike HSBC which only gave their customer 3 days notice (and 2 of the days were on a weekend)!!!

Update 5th May 2018 – AmBank Reward Redemption Revision 2018

Well, effective 1st May 2018, AmBank inflated their Air Miles redemption by 40%!!!

AmBank WMC and VI cardholders previously only needed 5000 Points to redeem 1000 Enrich Miles or KrisFlyer Miles or Asia Miles. But now they need 7000 Points.

With 5X Points for overseas transactions with the AmBank World MasterCard or Visa Infinite, this works out to 1 EM or KF or AM for every RM1.40 spent overseas (excluding online transactions).

You must be logged in to post a comment.