Another Personal Finance tutorial by GenX @ http://www.GenXGenYGenZ.com

Update April 2019

Below are two screenshots taken from RHB Website in April 2019 which is damn misleading (or maybe a more appropriate word is irresponsible) giving the impression that is is okay to be in debt if you have no money to go holidaying!!! And the joke is RHB is own by the government indirectly as the major shareholder is EPF!

15% interest rate Bros & Sis! I tell you, your credit card interest rate may be even lower if you pay off your debt sooner.

I tell you, Personal Loan is the fastest way to being poor. The moment you sign on the dotted line you are already poorer by the same amount of the personal loan amount PLUS interest!

Unfortunately our government (previous BN and current PH) don’t give a damn and have not taken steps to educated the Rakyat on the detrimental effects of Personal Loans. Yes, politician talk this and that but no actions to help the Rakyat by educating them.

If the Education Minister really wants to help the Rakyat, instead of implementing black socks and shoes, he should instruct that Personal Finance subjects be taught in secondary schools.

I tell you, all those so called Finance Websites that recommend Personal Loans are parasites as they make money promoting Personal Loans by the banks. On one hand they try to teach you how to save money but on the other hand they are enticing you to sign up for Personal Loans.

I have mentioned in my article titled Be Prepared For Tomorrow So That You Can Sleep Soundly (click here to read it) that the secret to being rich is not how much you earn but how much you save.

Whatever it is, do not apply for Personal Loans. If you are in debt, suspend your credit card accounts and go find ways to increase your income, e.g. be a part-time Grab Driver (no kidding) or a part time waiter.

If you are really in the shit hole of debt, DO NOT opt for Personal Loan to pay of you credit cards’ debts but instead seek help from AKPK.

The contents below is to educate you so that you won’t be fooled by the banks and tricked into the shit hole of debt.

Below contents were published in February 2018

For years I have been telling you guys that you should avoid loans with upfront interest and I have produced several articles on it.

Basically most, if not all of my articles is about not paying a sen of interest to the banks. I keep reiterating this over and over again – Do Not Be A Slave To The Bank. Instead I teach you guys about compound interest where if you constantly save money and deposit it into FD, by depositing a mere RM300 a month, you will have RMxxx,xxx.xx in 20 years time!!! If you have not taken my FREE Fixed Deposit Tutorial 2018 – it is to your own benefit that you click here now and read it.

If you follow the principles that I have kept repeating over the years, i.e. no debt so that you are not paying a sen in interest to anybody and depositing regularly into FD for your retirement and together with your EPF savings, you will have a comfortable retirement. Of course you will remain financially challenged if you constantly burn your money on non-essential stuff like holidays, fashion, gadgets, up sizing to a bigger home when you should be down sizing as you are near to retirement age and eating at Korean, Japanese and Western restaurants instead of One Ton Mee at the road side, hahahaha.

If you still do not comprehend the above, go talk to a rags to riches old man and I bet he will be more than happy to share with you how poor he was and how he saved and saved every penny. And if you observe carefully, you will see him pay for everything in cash and he will never ever buy a cup of exorbitantly priced Starbucks coffee. But the sad part is, he doesn’t know how to spend his children’s future inheritance, hahaha.

Anyway, recently I published my thoughts on how one can save 20% of his/her PTPTN Loan by utilizing 0% Balance Transfer Plan. For years, I will only teach you guys how to utilize 0% Balance Transfer and never ever asked any of you to sign up for any Balance Transfer Plans that impose 0.01% or more upfront interest!!!

However, it has come to my attention that some of you still do not comprehend that so called “low” interest rate offered with Personal Loans and/or Balance Transfer Plans with upfront interest makes you poorer instantly!!!

Below is a comment recently at my Facebook:

In respect to the above comment by one of my Followers, here are my comments:

- Firstly, if one is to go with 3 years BT Plan, it means that person is tight on cash.

- The person who opts for the 3 years BT Plan will be instantly poorer where he/she will immediately make the bank richer with the upfront interest.

- PTPTN interest rate is freaking low 1% to 3% on reducing balance.

- 36 months is a very long time. To start off with, this person is already tight on cash. What if the person suddenly cannot settle his/her credit card Statement Date in Full? He/she will then be imposed 18% interest!!!

- Therefore, if one cannot settle his/her PTPTN loan in full to save 20% by utilizing 0% BT Plan where he already has the cash in his savings, he/she should just repay his PTPTN loan via Direct Debit and save 10% which is basically risk free from being imposed additional interest up to 18% with credit cards.

- Khiang Ko Ho, Mien Keh Khiang.

So, I thought that I should once again highlight to each and everyone of you young GenYs who think that “low” upfront interest rate loans are good and that you “think” you can save some money by utilizing them.

Below contents were published in October 2016. Hopefully after you have read it, you will avoid upfront interest loans, regardless of how “low” the interest rate being offered is, so that you do not become poorer the instant you sign up and the loan is approved.

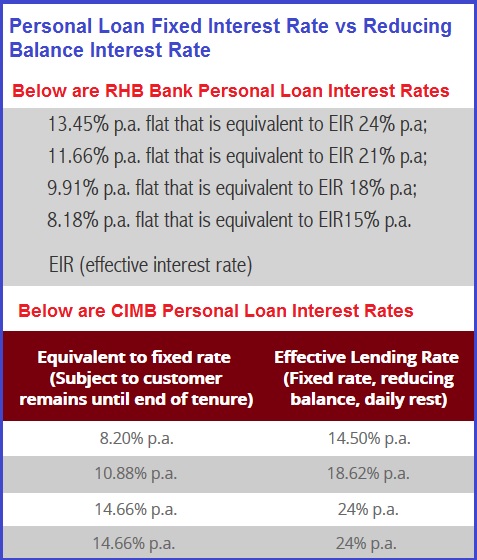

QUIZ – which is lower? 8.18% Personal Loan (Balance Transfer) Fixed Upfront Interest Rate OR 15% Credit Card Reducing Balance Interest Rate?

According to RHB website, they are the same!!!

However, according to CIMB website, 8.20% Fixed Rate Personal Loan is equivalent to 14.50%

For Personal Loan Fixed Rate – you are imposed interest immediately upon signing on the dotted line. i.e. You become poorer as you now owe the bank the Principal Sum + Interest. And the longer the tenure, the poorer you are. And you DO NOT save on interest charges if you make or settle any part of the debt in advance.

For Reducing Balance Loan, interest is imposed only on the outstanding amount. So, the sooner you pay up your debt, the less interest charges you incur.

I have been reminding you guys to avoid Personal Loan. Well, I did go check out some Personal Loans Interest Rates and I was shocked to find that it can go as high as 14.66% Fixed Rate with CIMB which is equivalent to 24% Effective Interest Rate!!! And what shocked me further is that some banks are offering Personal Loans to Pensioners (retired civil servants)!!!

If you have been paying your credit card bills promptly, you would be imposed Reducing Balance Interest Rate of 15% which is similar to Personal Loan with approximately 8.5% Fixed Rate for 5 years tenure according to a calculator by MoneyCamel dotcom.

So, from the above, you can observe that Fixed Rate Interest Rate is approximately 1.7X higher than Effective/Reducing Balance Interest Rate. Or round it up to a single digit, it’s 2X.

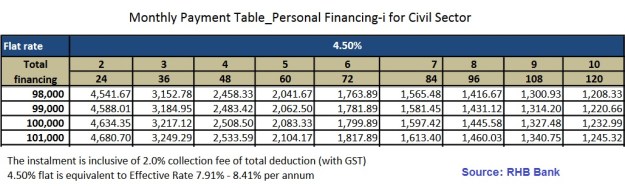

Most civil servant have Personal Loans and the reason is our government encourages it!!! Bank Rakyat, MBSB and RHB (all 3 are government or EPF controlled) promote Personal Loans to those employed by the government where the loan repayments are automatically deducted from their salary. For example, RHB offers 4.5% Fixed Rate Personal Loan to civil servants and charges an additional 2% (PLUS 6% GST, too) as collection fee on the monthly collection. Wow! With 6% GST imposed on the 2% Collection Fee, the government is taxing the poor civil servants who are already in debt by making them even poorer! Once again, 4.5% Fixed Rate is approximately 8.41% Effective Interest Rate (please refer to Notes in RHB’s table below).

Yesterday I read an article that household savings of public servants is 0.7% of their salary. My God that’s like no savings at all. With civil servants having easy access to Personal Loans, making them poorer, it’s a no brainer that they don’t have savings as most of their salary goes straight to repaying their Personal Loans! I tell you, if the government really wants to help the civil servants, they should put a stop to Personal Loans and instead encourage Housing Loans where at the end of the day the civil servant will own a home. Now, most of the civil servants do not really need to worry about saving for their retirement unlike most of us because when they retire, they still have access to very affordable (if not free) medical treatment and pensions where the government will give them money (amount based on a certain percentage of their last salary) until the day they die (which in turn the money would be given to the spouse). But what these civil servants must realize is that our lifespan is increasing. If one was to live until 100 years old and taking inflation into consideration (and without considering that Ringgit may weaken further in the future), the pension amount would be insufficient in the future.

There are 1.6 million civil servants who make up about 11% of the total work force in Malaysia. Guess how many retirees the government is paying pension to today? FYI, it is about 700,000!!! Therefore, the government is paying out money to 2,300,000 people monthly (that’s close to 10% of Malaysia’s population)!!! Let’s say each of them is paid RM1.2K (the minimum wage for civil servants), that means our government is paying out RM2,760,000,000 per month or RM33.126B a year. If you increase the average to RM2K per month per person, that’s equal to RM66B a year!!! According to Bloomberg, our government spends about 1/3 of our annual budget on salaries, pensions and gratuities. Therefore, with RM267.2B allocated for expenditure in the 2016 Budget, the total amount we pay to past and present civil government servants amount to RM89B!!! With the low oil price, our government has basically lost its main source of income and it’s a miracle that our government has money stashed somewhere to pay all the civil servants and pensioners monthly….. oh maybe it’s not a miracle but we have a visionary PM who saved the country from the brink of destruction by implementing the 6% GST. Click here to read article titled “PM called GST country’s saviour”.

Yes, if GST was not implemented, there would have been a very good chance that civil servants won’t be paid and the entire country will go into chaos because the police, army, teachers, government medical/clinic/hospital staff, etc will all go on strike and we the Rakyat will suffer. The civil servants also will not be able to repay their Personal Loans which will then result in Financial institutions like Bank Rakyat, RHB and MBSB going kaput (we the hard working Rakyat will also be at the losing end as EPF is the major shareholder of MBSB and RHB). One thing will lead to another and eventually our economy will be destroyed. I tell you, we are so lucky to have a visionary brave warrior PM and a wife who supports him. However, based on the current situation and at the rate we are paying the civil servants and pensioners, sooner or later the country will go bankrupt….. but Malaysia is one lucky country and eventually oil price will have to rise and we will all be saved…. and if oil price does not increase, well, we have to then depend once again on our PM (who is brave enough to go against the Rakyat’s wishes) to increase GST to 10% and once again be the saviour of our country. Conclusion – the government sooner or later will need to downsize the civil service sector plus stop the pension scheme as there’s no way our country can continue with the current situation unless all of us are willing to accept GST of 15%.

Coming back to how to get poorer the fastest way –

If you did not know, Car Hire Purchase Interest Rate Loan is exactly the same as Personal Loan Fixed Rate. To save on interest charges, it’s better to opt for a quicker loan repayment period, e.g. 3 years versus 9 years.

For example, if you were to borrow RM50K at 4.5% for a Myvi:

The amount of interest you would have paid for 3 years loan = RM50K x 4.5% x 3 years = RM6,750

versus

The amount of interest you would have paid for 9 years loan = RM50K x 4.5% x 9 years = RM20,250

Difference = RM20,250 – RM6,750 = RM13,500. If one was to invest this savings instead of handing it over to the bank and making the bank richer, come the end of the 9th year, one would have much more than RM13.5K cash in hand.

Or looking from another angle, you would have paid interest of RM20,250 plus the Principal Amount of RM50,000 = RM70,250. In 9 years time, how much do you think your top of the range Myvi would be worth? It’s junk!!! You would have burned RM70K for nothing (and I did not even include the down payment/balance cash paid for the car). The smarter option is to get an Axia that cost RM20K cheaper than a Myvi and opt for 3 years tenure and save more than RM30K in the process. And if you invested this saved money of RM30K into an investment that pays 5% interest, in twenty years time, it will grow to more than RM60K. That’s RM60K extra money for your retirement years to go pamper your grandchildren.

Those who opt for 9 years car loans are those who don’t have money and by opting for a longer loan period, they are actually getting poorer. That’s why I cannot comprehend how BNM can allow 9 years loan tenure for cars. I tell you, the government should put a stop to 9 year car loan tenures and impose even higher taxes on cars as there are just too many damn cars on the road today. Credit should be given to the Selangor government for launching FREE bus service.

Last but not least, if you have debt issues, especially credit card Outstanding Balance, the best people to talk to is AKPK. Do not borrow more money utilizing Personal Loans AND never entertain people who call you on your handphone offering debt restructuring as you can’t verify if it’s a con job. Even it it is not a con job, people who call you offering assistance on your credit card debts are just basically offering you Personal Loans which also makes you poorer instantly.

CONCLUSION

Loans that impose upfront interest, i.e. Personal Loans or Balance Transfer Plan or Hire Purchase (Car Loan) – they are all the same but termed/called differently. All these upfront interest rate loans makes you poorer instantly!!! The moment you sign up for these types of loans you are deeper into the shit hole of debt, your debt/liability becomes Principal Loan Amount + Interest Charges.

Once again, for example, you borrow RM10,000 with upfront interest of 7% for 3 years, the moment your loan is approved, you owe the bank RM12,100!!!

You should avoid Personal Loans and Credit Card Balance Transfer Loans (except 0%) at all cost. If you are signing up for any of these types of upfront interest loan(s), it means you are spending beyond your means and should seriously look into your spending pattern and lifestyle.

Except for car loans, where most of us have no choice in our early working years where we do not have much cash, and have to rely on it. And if you are smart, you should save more money to pay more towards the down-payment of the car and sign up for a shorter tenure loan period. And for those who think a car company offering 0% interest is good, well it means 2 things – the car has no demand (also translates to lower resale value) and you will definitely save thousands of Ringgit if you negotiate and pay cash for it!!!