A Credit Card Tutorial by GenX @ http://www.GenXGenYGenZ.com

INTRODUCTION

In my Introduction to Credit Cards – CC 101 (you should read this first if you have not), the very first lesson I taught you is that you should not give the banks any opportunity to impose any fee and/or interest for owning their credit card(s).

I use credit cards for convenience and to enjoy the benefits that come along with the cards such as discounts, points redemption, up to 40 days interest free for purchases, etc. I have never paid any annual fees for more than a decade, and should any bank not waive my annual fees in full, I would cancel the credit card with that bank as it does not make any sense to pay for services that I can get for FREE.

Today’s first lesson is, you should get FREE FOR LIFE Credit Cards or those that come with auto annual fee waiver mechanism with minimal conditions where you are able to satisfy easily.

If you are using your reward points to offset your credit card annual fee, you are actually paying in kind and losing out on the opportunity to earn FREE cash vouchers or other stuff. Also in my Introduction To Credit Cards – CC 101, I shared with you all that the best credit cards that earn you the most returns monetary wise are those that are FREE!!! And I listed some of the FREE FOR LIFE credit cards too.

The credit card industry is a very lucrative business for banks/credit card issuers as they charge exorbitant interest rates (almost as high as Ah Longs/Loan Sharks) on outstanding balances if you fail to settle in full your Statement Balance monthly. I have also shown you previously that 70% of card users fail to make full settlement monthly and thus making the banks richer by the day. And with the banks making so much money, many of them are willing to issue you credit cards for FREE.

I am going to repeat, always pay in full the Statement Balance before the Due Date to avoid paying interest to the banks.

For today’s post, I have incorporated what I have mentioned in my previous articles at blogspot to come up with what I think is a comprehensive article on matters relating to credit card interest rate and 0% interest rate plans. It’s best that you always settle in full your Statement Balance prior to the Due Date so you will never need to utilize nor have to worry about any of the items mentioned below.

INTEREST FREE PERIOD

All credit cards have a Statement Date where all your transactions prior to that date will be accumulated and must be paid before the Payment Due Date otherwise you will be charged interest on the Outstanding Balance after the DUE DATE. The time between the Transaction Date and the Payment Due Date is the interest free period. It is usually about 20-45 days.

Here is an example:

STATEMENT DATE is on the 10th of every month.

PAYMENT DUE DATE is on 30th of every month.

Lets say you made a purchase on 7th March 2016 and the said transaction shall be due for payment on or before 30th March 2016, thus you get about 23 days interest free credit.

To enjoy a longer interest free period, purchase the item on 11th March 2016 (after the STATEMENT DATE) and payment will only be due the following month on 30th April 2016. This means you enjoy more than 40 days interest free credit. If the said purchase was RM10,000, you could have deposit the money in Fixed Deposit for a month and earn interest of approximately RM25 (based on interest 3% PA) for the said purchase.

Please note that Interest Free Period only applies if you have settled in full the previous Statement Balance.

However, if you only make the Minimum Payment, finance charges are imposed immediately onto your Outstanding Balance which may include new transactions too.

CREDIT CARD TIERED INTEREST RATES

Many years ago, the banks would impose 18% p.a. interest on Outstanding Balances if one fails to settle in full prior to the Due Date. However, a few years back, in line with BNM’s wish to reduce the burden of interest charges on credit card users, the banks revised the rates to range from 13.5% to 17.5%. This tiered interest rates are suppose to reward cardholders who pay the minimum amount promptly. I tell you this tiered interest rate thingy is a joke. Reward it seems, what is the difference between 13.5% and 17.5%? If you do not settle in full every month, your debt will still balloon up with interest rate of 13.5% which I consider as damn freaking high.

Beginning March 2012, some banks have revised the highest tiered rate to 18% and the lowest starting at 15% instead of 13.5%.

As far as I am concerned, if you are paying interest to the bank because of your credit card usage, it’s immaterial if the interest rate is 13.5% or 18%, you should cancel your credit card immediately and switch to Debit Cards for the simple reason that you are spending beyond your means and getting poorer by the day with daily interest imposed on your Outstanding Balance.

CREDIT CARD INTEREST CHARGES

Credit Card Interest Rate is Damn Freaking High – always remember this.

1. In order to enjoy the FREE interest period of up to 20 days (usually counted from the day of your Statement Date), one has to settle in full the Statement Balance amount stated in the monthly statements prior to the Due Date. Even if you can only afford to pay the minimum 5%, make sure you pay it before the Due Date as not to tarnish your credit history.

2. The moment you fail to settle in full prior to the Due Date, for new users to a particular credit card who is holding the card for less than a year, you will be imposed interest rate of 18% on your outstanding balance including all new transactions.

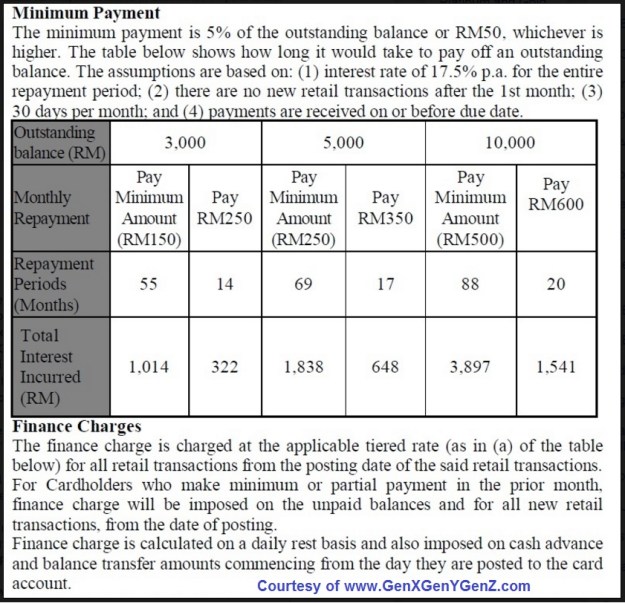

3. If you have an Outstanding Balance of RM3,000 and you were simply paying the minimum monthly payment of 5%, it would take you 55 months to settle the total debt and over and above that, you’ll be paying RM1,014 in interest based on interest rate of 17.5% And if you have Outstanding Balance of RM10,000 and once again you only pay the minimum 5% required, it will take you 88 months to settle the debt! See following example:

Now, remember if you have Outstanding Balance, the Interest Free Period mentioned above shall no longer be applicable and all new transactions shall be imposed interest charges. So if you do have Outstanding Balance – USE ANOTHER CREDIT CARD that has no Outstanding Balance. And if you also do not settle in full for this other credit card and are being imposed interest charges, then it is confirmed that you are stuck in the shit hole of debt. I wish you the best of luck and better pray hard that you strike Jackpot or 4D OR you can do the smart thing by cutting up your credit cards and seeking assistance from Agensi Kaunseling dan Pengurusan Kredit (AKPK).

4. How are interest imposed on credit card outstanding balance? Well, to be frank, I don’t really know because I always practice paying in full every month prior to the Due Date to avoid being charged a single sen of interest. However, I believe it should be something like this. I may be wrong but you will get the idea.

You must be logged in to post a comment.