A Credit Card Tutorial by GenX @ http://www.GenXGenYGenZ.com

INTRODUCTION

In my Introduction to Credit Cards – CC 101 (you should read this first if you have not), the very first lesson I taught you is that you should not give the banks any opportunity to impose any fee and/or interest for owning their credit card(s).

I use credit cards for convenience and to enjoy the benefits that come along with the cards such as discounts, points redemption, up to 40 days interest free for purchases, etc. I have never paid any annual fees for more than a decade, and should any bank not waive my annual fees in full, I would cancel the credit card with that bank as it does not make any sense to pay for services that I can get for FREE.

Today’s first lesson is, you should get FREE FOR LIFE Credit Cards or those that come with auto annual fee waiver mechanism with minimal conditions where you are able to satisfy easily.

If you are using your reward points to offset your credit card annual fee, you are actually paying in kind and losing out on the opportunity to earn FREE cash vouchers or other stuff. Also in my Introduction To Credit Cards – CC 101, I shared with you all that the best credit cards that earn you the most returns monetary wise are those that are FREE!!! And I listed some of the FREE FOR LIFE credit cards too.

The credit card industry is a very lucrative business for banks/credit card issuers as they charge exorbitant interest rates (almost as high as Ah Longs/Loan Sharks) on outstanding balances if you fail to settle in full your Statement Balance monthly. I have also shown you previously that 70% of card users fail to make full settlement monthly and thus making the banks richer by the day. And with the banks making so much money, many of them are willing to issue you credit cards for FREE.

I am going to repeat, always pay in full the Statement Balance before the Due Date to avoid paying interest to the banks.

For today’s post, I have incorporated what I have mentioned in my previous articles at blogspot to come up with what I think is a comprehensive article on matters relating to credit card interest rate and 0% interest rate plans. It’s best that you always settle in full your Statement Balance prior to the Due Date so you will never need to utilize nor have to worry about any of the items mentioned below.

INTEREST FREE PERIOD

All credit cards have a Statement Date where all your transactions prior to that date will be accumulated and must be paid before the Payment Due Date otherwise you will be charged interest on the Outstanding Balance after the DUE DATE. The time between the Transaction Date and the Payment Due Date is the interest free period. It is usually about 20-45 days.

Here is an example:

STATEMENT DATE is on the 10th of every month.

PAYMENT DUE DATE is on 30th of every month.

Lets say you made a purchase on 7th March 2016 and the said transaction shall be due for payment on or before 30th March 2016, thus you get about 23 days interest free credit.

To enjoy a longer interest free period, purchase the item on 11th March 2016 (after the STATEMENT DATE) and payment will only be due the following month on 30th April 2016. This means you enjoy more than 40 days interest free credit. If the said purchase was RM10,000, you could have deposit the money in Fixed Deposit for a month and earn interest of approximately RM25 (based on interest 3% PA) for the said purchase.

Please note that Interest Free Period only applies if you have settled in full the previous Statement Balance.

However, if you only make the Minimum Payment, finance charges are imposed immediately onto your Outstanding Balance which may include new transactions too.

CREDIT CARD TIERED INTEREST RATES

Many years ago, the banks would impose 18% p.a. interest on Outstanding Balances if one fails to settle in full prior to the Due Date. However, a few years back, in line with BNM’s wish to reduce the burden of interest charges on credit card users, the banks revised the rates to range from 13.5% to 17.5%. This tiered interest rates are suppose to reward cardholders who pay the minimum amount promptly. I tell you this tiered interest rate thingy is a joke. Reward it seems, what is the difference between 13.5% and 17.5%? If you do not settle in full every month, your debt will still balloon up with interest rate of 13.5% which I consider as damn freaking high.

Beginning March 2012, some banks have revised the highest tiered rate to 18% and the lowest starting at 15% instead of 13.5%.

As far as I am concerned, if you are paying interest to the bank because of your credit card usage, it’s immaterial if the interest rate is 13.5% or 18%, you should cancel your credit card immediately and switch to Debit Cards for the simple reason that you are spending beyond your means and getting poorer by the day with daily interest imposed on your Outstanding Balance.

CREDIT CARD INTEREST CHARGES

Credit Card Interest Rate is Damn Freaking High – always remember this.

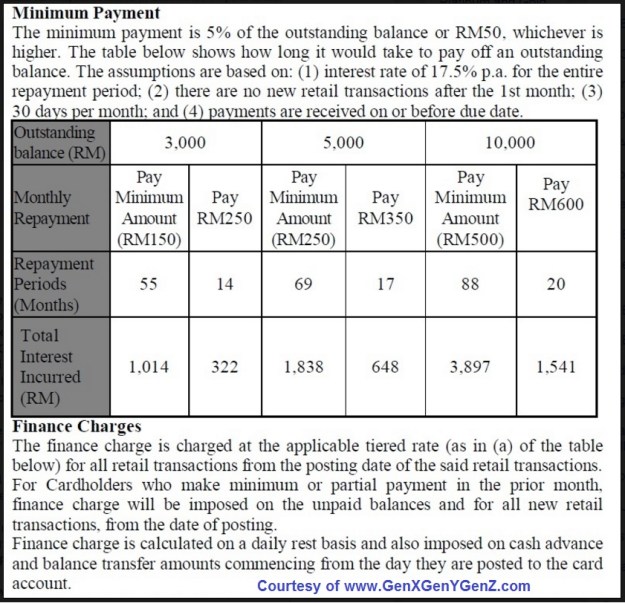

1. In order to enjoy the FREE interest period of up to 20 days (usually counted from the day of your Statement Date), one has to settle in full the Statement Balance amount stated in the monthly statements prior to the Due Date. Even if you can only afford to pay the minimum 5%, make sure you pay it before the Due Date as not to tarnish your credit history.

2. The moment you fail to settle in full prior to the Due Date, for new users to a particular credit card who is holding the card for less than a year, you will be imposed interest rate of 18% on your outstanding balance including all new transactions.

3. If you have an Outstanding Balance of RM3,000 and you were simply paying the minimum monthly payment of 5%, it would take you 55 months to settle the total debt and over and above that, you’ll be paying RM1,014 in interest based on interest rate of 17.5% And if you have Outstanding Balance of RM10,000 and once again you only pay the minimum 5% required, it will take you 88 months to settle the debt! See following example:

Now, remember if you have Outstanding Balance, the Interest Free Period mentioned above shall no longer be applicable and all new transactions shall be imposed interest charges. So if you do have Outstanding Balance – USE ANOTHER CREDIT CARD that has no Outstanding Balance. And if you also do not settle in full for this other credit card and are being imposed interest charges, then it is confirmed that you are stuck in the shit hole of debt. I wish you the best of luck and better pray hard that you strike Jackpot or 4D OR you can do the smart thing by cutting up your credit cards and seeking assistance from Agensi Kaunseling dan Pengurusan Kredit (AKPK).

4. How are interest imposed on credit card outstanding balance? Well, to be frank, I don’t really know because I always practice paying in full every month prior to the Due Date to avoid being charged a single sen of interest. However, I believe it should be something like this. I may be wrong but you will get the idea.

Say you did a Transaction on 5th May 2016 for RM10,000. Your Statement Date is 10th May 2016 and your Due Date is 30th May 2016. Therefore, the minimum amount Due is RM500 (5% of RM10,000).

You pay RM500 on 30th May 2016, without interest charges, your Outstanding Balance should be reduced to RM9,500 and carried forward.

However, this may not be necessarily the case for credit cards.

I believe the interest charges are calculated as follows, I might be wrong, but it will not be too far off.

Interest charges up to 30th May 2016 = 17.5% x RM10,000 x 25days/365 = RM119.86. (25 days = 5 May to 30 May).

Therefore, outstanding Balance as of 30th May 2016 after you pay RM500 adds up to RM10,000 + RM119.86 – RM500 = RM9,619.86

So from 30th May 2016 onwards, you will be imposed daily interest calculated as follows:

RM9,619.86 x 17.5% x (days/365)

AND if you make another RM2,000 transaction with the same credit card on 5th June, additional interest charges will be added as follows:

RM2000 x 17.5% x (days/375) commencing from 5th June 2016.

So come end of 30th June 2016, your interest charges will be:

RM9619.86 x 17.5% x (30days/365) = RM138.37

+ RM2000 x 17.5% x (24days/365) = RM23.01

and total Outstanding Balance on 30th June will be 2016 =

RM9619.86+RM2,000+RM138.37+RM23.01 = RM11,781.24

See, from the above example on credit card interest charges, you spend a total of RM12,000 in the months of May and June and you have already paid RM500 in May but come end of June, the amount with interest adds up to close to RM12,000 again.

Now, let’s say you pay another RM2,000 on 30th June 2016 and do not use your credit card for any other transactions in the entire month of July (no money, so use the card for what), the interest imposed on your account will be as follows:

New Outstanding Balance on 30th June 2016 = RM11,781.24 – RM2,000 = RM9,781.24

Interest from 1 June 2016 to 29 June 2016 = RM9,781.24 x 17.5% x (29day/365) = RM135.99

Therefore your new Outstanding Balance on 30 July 2016 = RM9,781.24 + RM135.99 = RM9,917.24

See, even though you paid RM2,000 on 30 June 2016, the outstanding balance keeps increasing daily as long as you don’t make payment in full.

So from the example above, here is the summary:

a. Total amount transacted in months of May, June and July = RM12,000.00

b. Total payment made at the end of May and June = RM2,500

c. Total Outstanding as of end of July 2016 = RM9,917.24 (for comparison purposes RM12K – RM2.5K = RM9.5K)

d. Total interest imposed from 5th May 2016 and up to 30 July 2016 (Due Date and you have to make another payment) = RM417.23.

Please note from item c above, you made transactions of RM12,000 and you paid RM2,500 which means that without interest charges, the outstanding balance should be reduced to RM9,500. But because you did not settle in full, interest charges were imposed on your outstanding balance and you will end up having to pay more every month.

As for item d, the bank made RM417.23 from your own doing without them doing a single thing. You made the transaction, you made partial payments and then you went and swiped your card again. Once you fail to pay in full, every time you swipe your card, you are generating tons of money for the bank, that is why I say you are working for the banks for FREE or are a slave to the banks.

5. Once again, I want to stress that if you really need to have outstanding balance in your credit card account, DO NOT use the same credit card but use another card (from a different bank) that has no outstanding balance so that your new transactions are not imposed interest charges for nothing. And make sure you settle in full the Statement Balance of this other said card so that you would not be imposed any interest. As for the first card, pay off as much as you can every month and the goal is to be debt free as soon as possible.

0% INSTALLMENTS PLANS with CREDIT CARDS

There are two reasons I can think of why people opt for 0% installment plans.

1. The first is that we cannot afford to pay for the purchase in full. So it is wiser to opt for 0% installment plans instead of paying interest on the outstanding balance in our credit card account. However, if you only pay 5% minimum monthly, then once again you will be imposed high interest rate of 18% which defeats the purpose of you opting for the 0% installment plan. And once again, all new transactions with the card will also be imposed interest charges.

2. The second reason is, we think that the 0% interest installment plan we are getting is a good deal. Like I mentioned previously, many of the merchants offering the 0% installment plans have included the cost of subsidizing these plans into the purchase price. Many times I have come across merchants giving me a further discount when I do not opt for the 0% installment plans. Always ask if you can get further discount if you pay in full (one swipe) or pay with cash.

The other thing is, we may think we can utilize this so called benefit by making our money grow with the unpaid portion of the stuff we bought. Well, most of us are just kidding ourselves and you know what I mean because every month we are short of cash. I will present to you later on an article titled 0% Installment Plan with Credit Card – IT IS a Trap CC 164.

Having said the above, if the purchase is of a substantial amount, AND we have the funds on standby to pay it off in one go, then maybe we may earn some pocket money by opting to go with 0% installment plan. By depositing the available standby fund into FD, we can earn some pocket money along the way. I will touch on this later on in my article Benefits of Credit Card CC – 118

The next time you want to go with a 0% installment plan, ask yourself this – do I have the cash in hand to purchase the stuff? If the answer is no, then you are simply living beyond your means if you opt for the installment plan, since you cannot afford it in the first place. What you are doing is “live now earn later” instead of save now and live better in the future.

A Credit Card Tutorial by GenX @ http://www.GenXGenYGenZ.com

0% INTEREST FOR 3 to 6 MONTHS ON ALL RETAIL PURCHASES

This is another trap by the banks to make you spend more than you can actually afford to. Some banks offer new cardholders up to 6 months interest free period for all transactions. So happily we go swipe our cards thinking we are getting free money. Come end of the honeymoon period, we are stuck with a huge outstanding balance and only realize that we have spent beyond our means and can only pay part of the amount owing. Thus, the unpaid balance is imposed high interest rate. So, the ones who think they are “smart” will go perform a Balance Transfer. If we are really smart, we would not have accumulated the huge debt in the first place.

CONVERT YOUR RETAIL PURCHASES INTO “0%” INSTALLMENT PLANS

Some banks promote so called 0% interest installments for any kind of transaction anywhere but it is not really 0% because they charge between 2% to 7% upfront for the easy payment plan. Always read the terms and conditions for any promotions offering 0% interest plans. And once again, if you can only afford to pay the minimum 5% of your Outstanding Balance, please do not sign up for these plans as you will be charged interest and thus end up paying more that if you did not opt for these kind of plans.

When you opt for installment plans with Upfront Admin Fees/Charges, the effective Interest Rate is much much higher than what is quoted. But most of the banks will never tell you this. The banks that are offering this installment plans as of 31st December 2015 are BSN, AmBank, CIMB, Maybank, RHB and Public Bank and they name them FlexiPay, Smart Pay, Easy Pay or Ezy Pay.

Bank Simpanan Nasional Installment-Pay Paln – 3% to 5% Upfront Interest.

AmBank Flexi-Pay – 3% to 6% Upfront Interest.

Citibank FlexiPayment Plan – 9.84% to 10.57% Upfront Interest.

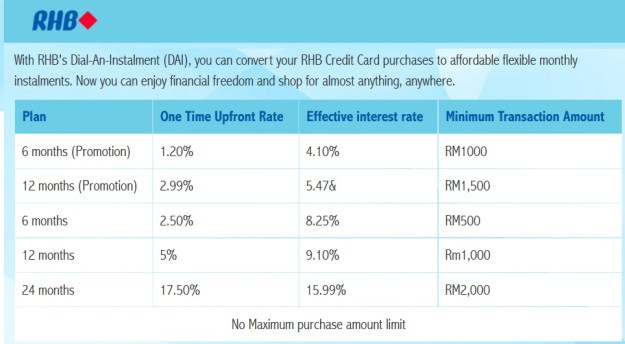

RHB Dial-An Instalment 1.2% to 17.5% Upfront Interest.

Public Bank FlexiPay – 0% to 5% Upfront Interest. There really have a 0% Installment Plan for 12 months tenure!

If you have checked out the above offers, Bank Simpanan Nasional is the only bank which states that their plan is ZERO INTEREST which is bull shit since it does charge upfront fee and BSN is owned by our government!

Public Bank on the other hand does offer true 0% interest free for their 12 months Flexi Pay for amounts more than RM2K where the promo is valid until end of June 2016.

If you have checked out Citibank FlexiPayment Plan’s link above, they are transparent enough to tell you that the Effective Interest for their plans is 17.9%

RHB is better still, they tell you what are the exact Effective Interest Rates for different tenures:

If you ask me, it is not worth it to go for an installment plan that charges us upfront fee unless it is really 0%, i.e. no upfront fee. Why would you want to pay interest? Look for merchants that actually offer true 0% installment plans without any upfront fee, e.g. All IT at Low Yat Plaza, Harvey Norman, SenQ, Dell, Courts, Poh Kong, Wah Chan and etc.

CASH WITHDRAWAL WITH CREDIT CARDS

Banks love it when you withdraw cash with your credit cards. The moment the cash is dispersed from the ATM machine, the bank is laughing at you because not only have you been imposed a one time fee of 5% on the amount withdrawn, BUT you are imposed daily interest charges of 18% (per annum rate) until you make full payment.

For example, if you withdraw cash with your credit card, and you pay back in full within a month, the fixed 5% withdrawal fee will be something like 60% interest rate (5% x 12 month)! And I have yet to even consider the daily interest charges of 18%p.a. Once again, never ever withdraw cash with credit cards.

If you really need to do cash withdrawal for emergency purposes, go get a debit card. If you withdraw cash with your credit card to purchase stuff that is not required for your survival, well, you must be really lazy to go read the Terms and Conditions to educate yourself or you are just plain stupid (which I doubt is the case since you know how to come here and read this post, hahaha).

If you are withdrawing cash using your credit card on a regular basis, it means that you are living beyond your means and you should cut the card in two.

EASY CASH WITH CREDIT CARDS

Some banks have this plan where you can request for cash by utilizing your credit facility. The difference between this plan versus cash withdrawal is that usually only an upfront fee is imposed and if you settle your Outstanding Balance in full prior to Due Date, no other interest charges are applicable.

Some of the banks currently (as of 31 December 2015) offering this kind of plans are:

AmBank Quick Cash 8.99% Upfront Interest.

BSN Easy Cash 8.5% Upfront Interest

A Tutorial by GenX @ http://www.GenXGenYGenZ.com

Hong Leong Bank Call For Cash 9.88% Interest Rate

Maybank EzyCash 3.88% Upfront Interest

Now, just like the Convert to 0% Installment Plan, don’t be fooled by the “low” Upfront Interest/Admin Fee. The effective interest is much much higher.

For example, if you had read AmBank’s Terms and Conditions for their AmBank Quick Cash, you would have noted the following:

A special interest/management fee rate of 8.99% flat per annum (equivalent to effective interest/management fee rate of 16.23%) will be charged to the Cardmember’s account based on the amount approved.

See, upfront fee of 8.99% is equivalent to effective interest of 16.23% which is not much lower than the interest rate of 18% imposed onto Outstanding Balance. In actual fact, you may even pay less in interest with your credit card tiered interest rate which is based on reducing balance.

So before you go sign up for so called Easy Ezy Fast Quick Cash offered by AmBank, BSN, Hong Leong Bank, Maybank or RHB Bank, please read the terms and conditions to see if there is any Upfront Admin Fee/Interest Charges.

Comparison of Upfront Interest Plan versus Credit Card Tiered-Interest

If you are thinking of going with any of the Upfront Interest Plans (Convert Purchases to Installment, Balance Transfer and Easy Cash), do a comparison with your credit card tiered interest rate by using the AKPK’s credit card interest calculator below and see which method with the same repayment amount will be imposed less interest charges :

AKPK Credit Card Interest Rate Calculator

BALANCE TRANSFER

Many of us are in deep shit because we have over spent as a result of our own doing and thank god that some banks are offering 0% interest free Balance Transfer plans.

Well, if you are one of the millions having outstanding balance with your credit card and are paying interest of 13.5%-18%, it makes sense to perform a 0% Balance Transfer. Thus, you will be forking out less on interest payments.

However, if you do a Balance Transfer and then start to use up the available credit which has been transferred to purchase unnecessary things which are not needed for your survival and can’t settle in full come payment date, my advise is, you better just cut up the card in half and settle your debt or else you are just going deeper down the shit hole and being a slave to the banks.

[Note: For those who have been following my blog, you will note I keep repeating the above. This is because I want to highlight that by doing a Balance Transfer, one is still in debt. And if one still goes and swipes his or her credit card after doing a Balance Transfer Plan, then he or she is just accumulating more debt and getting deeper into the shit hole.]

You have to admit that you are living beyond your means once you do a Balance Transfer. The fact is that you are in debt. And remember, for balance transfer plans with equal installments (and no separate account created), if you only pay the minimum or do not settle the Outstanding Balance in full prior to the Due Date, once again you’ll be imposed interest charges.

Generally for Balance Transfer, most banks offer lower interest for shorter Balance Transfer repayment duration. Why is this so? Well, the banks know that most people who have outstanding balances have no discipline when it comes to spending. Therefore, they will attract you by offering a lower interest rate for the shorter Balance Transfer duration program and hope that you won’t be able to settle in full so they can then charge you 18% interest after the “promotion period”.

Generally the different types of Balance Transfer Plans are:

1. 0% Interest Balance Transfer where no interest is imposed through out the duration nor any Upfront admin fees AND a new account is created for the Balance Transfer.

2. 0% Balance Transfer where NO new account will be created and the installment towards the BT is included along with your old and new transactions. Your repayment towards the Outstanding Balance may be based on the bank’s own hierarchy system. So, for 0% Balance Transfer, if no new account will be created, please understand the terms and conditions and the bank’s payment hierarchy. If you don’t understand the payment hierarchy but you need to do a Balance Transfer, my advise is it is best for you not to have any Outstanding Balance before you do the BT and don’t use the card until the Balance Transfer amount is settled in full. This is to ensure your payment is purely towards the Balance Transfer debt only so you won’t get any headaches. I strongly recommend that you avoid HSBC Balance Transfer Plan where no new account is created for the Balance Transfer Amount. Long ago, I called HSBC to confirm that I won’t be charged a single sen for their 0% Balance Transfer Plan; and their Customer Service representative couldn’t confirm that I wouldn’t be imposed any interest. Neither could she explain what their payment hierarchy means in relation to Balance Transfer Plan.

3. Reducing Balance where interest is imposed on balance outstanding. E.g. Alliance FlexiPay, HLB BT and Citibank Ready Credit. The earlier you pay towards the Balance Transfer debt, the less you pay in interest.

4. Upfront Interest Balance Transfer where you are imposed Upfront interest upon approval. This type of Balance Transfer may even have you paying more in interest compared to your credit card tiered interest rate on Outstanding Balance (i.e. the earlier you pay the less interest charges).

In respect of the above plans, you must read and understand the terms and conditions because there are many clauses that allow the banks to impose fees and interest charges. If you fail to understand the terms and conditions (most probably the person who drafted the Terms and Conditions did not understand them and that is why he couldn’t come up with a clear and precise write up in English. Thus, the Customer Service representatives who read it is also as blur as you and me, hahahaha). Don’t be surprised when you are charged interest even though you thought you have signed up for a 0% Interest Balance Transfer Plan (especially if no new account is created and it’s not based on fixed equal installments).

To learn more about Balance Transfer Plans/Programs offered by banks and facts you need to know, please read my tutorial on Balance Transfer.

CONCLUSION

Our credit cards do come with many “benefits” and the card issuers also have regular promotions which make us think that we are getting a good deal. Sometimes, these promotions and benefits entice us to spend on things we otherwise would not. Some credit card issuers are even worse, they encourage us to spent on things we cannot afford with advertisements brain washing us to buy stuff for our loved ones or go for overseas holidays.

Whatever plan you sign up for, always remember to pay in full the amount stated in your Monthly Statement before the Due Date or else you’ll be imposed interest which defeats the purpose of you signing up for 0% interest plan.

So, always remember to be smart and not spend on unnecessary stuff with your credit cards. Neither does a credit card dictate your lifestyle nor make your life any better. Credit Card is a tool just like money, use it wisely and you can reap benefits from it. But if you have no discipline in controlling your spending, DO NOT hold a credit card. If you think that credit cards make it affordable to splash on stuff you otherwise cannot afford, with the many installment schemes, you are deeply mistaken because you failed to realize that you opt for these plans because of the simple fact you don’t have the money in hand. And the value of stuff you purchase with credit cards usually do not appreciate with time and as such you are actually losing out in the long run i.e. making you poorer.

If you had read the prelude to this series of articles on Credit Cards for Beginners, I mentioned that Malaysians have a total of RM30.8 Billion owing to card issuers and 50% of them earn less than RM36K per year. In 2009, the amount owing to banks was about RM22.13 Billion. Therefore, in just 2 years, the amount owing to banks increased by RM8,670,000,000.00!

Imagine, how much do the banks earn with RM30,800,000,000 outstanding credit card balances from Malaysians. Hard to imagine right, too many zeroes. My calculator also cannot handle the zeroes!

Now, the banks not only make money from outstanding balances, but every time we swipe our cards, the banks make money from our transactions. That is why the higher level cards (Premier Cards like Visa Signature, Visa Infinite and World MasterCard) have more benefits. The banks love the big spenders as they also contribute to the banks’ bottom line (and more so if they have outstanding balances). The banks don’t need to waste their resources by offering many benefits to Entry Level cards since they are already making tons of money from these category of people as most cannot afford to settle their outstanding balances in full every month.

I guess big spenders coupled with the interest earned from outstanding balances from the people who spend beyond their means, make the banks that are well managed able to register record profits every quarter.

I tell you, Credit Card is the best product in this entire world to make money. You tell me, where can you find a product that you can give out for free to people that can generate continuous profit without needing to actually produce a physical product which requires labour and or resources? Credit cards make money for the card issuers out of nothing (you can see this from the example above, the banks are making huge profits from interest charges). We, the card holders, are like soldier ants (slaves). Millions of us with credit cards make the banks richer every single minute with our cards. And when we fail to perform our duties in making payments (with interest charges), the enforcers (debt collectors) will come after us and ensure that we dutifully carry out our duties (making payments) to the banks (the Queen Ant).

Yes indeed, sometimes we need to spend above our normal monthly budget in emergency cases (like you are short of cash in the middle of the month but you need to pay your car insurance; and ladies – emergency does not apply to wanting the latest Louis Vuitton handbag). In order to save some interest charges, I recommend to those of you with Fixed Deposit in the banks to pledge it towards an overdraft (OD) facility tied to your current account. Generally the interest for OD is between -1% to 1% of BLR for FD pledged. Presently, the current BLR is around 6%-7% which is much much lower than any interest charged by credit card for outstanding balance. Use the OD to pay your credit card bills to save on interest and at the same time you are earning interest on the FD pledged to the bank. Of course you still have to budget your expenses to clear your OD. The sooner the better.

Seriously, if you are a wage earner and you have credit card outstanding balance that is more than your monthly salary, I strongly recommend that you stop using your credit card. Even go to the extend of cutting the card in two. The reason I say this is because it shows that you are living beyond your means or you have no discipline in controlling how you spend. For people in this situation (giving banks more profits and being a slave to the banks), use whatever cash not required for your daily survival and make payment towards your outstanding balance and save on interest charges.

The first and foremost reason why banks are in existence is to make money. Banks are not here to make your life any better. BUT for the smart ones, they can actually benefit with credit card usage. Nowadays, with Debit Cards, the argument of Credit Cards being more convenient than cash no longer applies. The primary reason why one uses a credit card is because he has no cash in his CASA (Current Account Savings Account).

So, be smart and do the following:

1. Always settle your STATEMENT BALANCE in FULL prior to the Due Date to avoid interest charges.

2. Do not be fooled and tricked into spending beyond your means with the many 0% interest plans and promotions. Remember that you are in debt if you have an installment plan or balance transfer. Ask yourself before you swipe your card – Do I have the cash in hand to pay for the purchase? If the answer is no and you go swipe the card, you are living beyond your means.

3. Do not ever withdraw cash with credit cards. If you really really need cash, look into Hong Leong Bank’s Call For Cash where they deposit the money into your Savings Account and the interest rate is much much less than withdrawing cash from ATM with credit cards. But there is also a penalty fee if you settle the debt a day earlier!

4. Credit Card is a tool just like cash. If you choose to use it wisely, it can reward you. Alternatively, well, most of the time, a credit card can make you poorer faster than you can imagine.

5. If you currently have outstanding balances with your credit card, you are advised to keep the card in the drawer or even better if you cut it in half.

6. Last but not least, the next time the stock market crashes, go buy bank stocks and then you can fantasize that you are the Queen Ant and laugh every time millions of your soldier ants go swipe their credit cards, hahaha.

I hope the above have been informative and helpful. Thank you for reading.

A Credit Card Tutorial by GenX

A Credit Card Tutorial by GenX

![]() Click here t o GenX GenY GenZ Facebook Page

Click here t o GenX GenY GenZ Facebook Page

Click here to my Credit Card Tutorial Page/Menu for your next FREE lesson.