Credit Card Tutorial by GenX @ http://www.GenXGenYGenZ.com

INTRODUCTION

Time does pass by in a flash, as it has been 7 years since I started blogging on 17th February 2009 at My Credit Cards Blogspot. The very first post I published had the same title as this article – Introduction To Credit Cards – CC101. The article was comprehensive (freaking long) and to my surprise, nobody complained and people actually thanked me for it. That made me realize that many people are oblivious to the pros and cons of credit cards and the problems/cost that may arise with owning a credit card. Since that day, I have published many articles relating to credit cards to assist credit card users to optimize their returns.

First, I will start off with a little bit of background information about my “qualification” to tutor (for FREE, so don’t expect good quality tuition, haha) you about credit cards.

I have been using credit cards for more than 25 years. I got my first Visa credit card while still a student in the USA at the age of 19. American Express upgraded my standard card to Gold status while I was still pursuing my undergraduate degree and my card states Member Since 88. When I came back to Malaysia, I requested that the USA AMEX Gold account be transferred to a Malaysian account. Imagine I was an unemployed bum back in 1991 with an AMEX Gold Card (at that time it was the highest ranked card in Malaysia, no Platinum yet) and people would say that it was a supp card. I also managed to transfer my US Classic Citibank Visa to a local account but subsequently cancelled it after they charged me Late Payment Fee and Interest for late payment as my cheque reached them late through post (that time there was no internet banking) due to the combined Raya and CNY festivals back in the early nineties.

First Lesson Of The Day – DO NOT GIVE THE BANK(S) ANY OPPORTUNITY TO IMPOSE ANY FEES/INTEREST ON YOUR CREDIT CARD ACCOUNT UNLESS YOU WANT TO BE POORER.

Below is a photo of My Credit Cards Collection in 2015 posted at GenerationsXYZ Blogspot. The reason I have so many credit cards is “shiok sendiri” lah, hahaha.

Seriously, no two credit cards are alike. Therefore, each of my credit cards has a purpose of its own.

On 1st January 2011, I “fired” my boss and went back to being an unemployed bum. And today, with the credit cards that I am still holding, the total combined credit limit from all my cards exceed half a million Ringgit. At one time it actually touched RM1,000,000 but I have since then cancelled several cards which are not FREE FOR LIFE as I did not want to be at the mercy of the banks where I need to beg them yearly to waive my credit cards’ annual fees.

Second Lesson Of The Day – if possible ONLY APPLY FOR FREE FOR LIFE CREDIT CARDS without any conditions or minimal conditions so that:

- You do not need to fork out a single sen for your credit card annual fee. Why the heck would anyone want to pay (including paying in kind by using reward points to offset the annual fee) for services/benefits that they can get for FREE is a wonder to me. If I request RM11.18 from you to read my FREE article(s), would you pay me? If yes, please donate RM11.18 to me via my PayPal account at GenXGenYGenZ.hotmail.com. Always remember – Cheap No Good, Good No Cheap BUT FREE IS THE BEST! But to be frank to you, a few of my readers are really generous and wanted to thank me by sending me FREE money and FREE Enrich Miles because they benefited from my articles!!! But I declined their generous offers (with monetary value) because many of my readers are my iFriends and they have provided me valuable information whenever I asked for assistance at my Facebook Page.

- You do not need to go beg yearly for the annual fees to be waived.

- You would not feel like a dumb-ass in the event the bank rejects your request for the annual fee waiver, haha.

Many people would initially apply for a credit card for convenience sake (safer than carrying a bunch of notes). But credit cards were not created to provide convenience. The sole reason why credit cards exist is to make the banks more money. Basically, when one applies for a credit card, one is applying for a loan facility. And the maximum loan amount approved that can be utilized is called the Credit Limit.

30 to 40 years ago, the people who really wanted a card for convenience sake (instead of carrying cash) would apply for a charge card. Those who applied for credit cards were those who were in need of cash as applying for a credit card was the easiest method to get a loan as one does not need to provide any collateral. One could easily obtain a credit card by providing documents to the banks to prove that they earn a mere RM1.5K/month and the banks would happily issue them credit cards.

Like I said, majority of those who apply for credit cards are those who are in need of cash, ie. broke or no savings. So come Due Date to make their credit card payment, most likely they can not afford to settle the bill in full and would only pay the Minimum Amount Due. Whatever unpaid Outstanding Balance will then be imposed freaking high interest rate by the credit card issuer (bank). Thus making the bank richer and the cardholder poorer. OR as I like to put it, the cardholder is a slave working for the bank for FREE!

Studies have proven time and time again that people who hold credit cards spend much more than people who use cash. Not only that, many people have gone bankrupt because of credit cards as they do not have the discipline to control their spending. You can go google this and read the findings yourself.

Third Lesson Of The Day – If you are trying to stay afloat with your current income and have no savings today and then use your credit card, what makes you think you will have money tomorrow to pay the credit card bill? If you are really trying to stay afloat with your current income, DO NOT USE YOUR CREDIT CARD.

For those who intend to apply for a credit card for the sake of convenience instead of carrying cash, the above three lessons of the day is all that one really needs to know and practice when getting a credit card.

But then again, you don’t really need a credit card nowadays as a Debit Card and even Prepaid Visa and MasterCard give you the exact same function in terms of convenience and security.

Before you proceed any further in taking this tutorial, IT IS A PREREQUISITE that you read my article titled LIFE – GOAL IS TO BE DEBT FREE by clicking here right now.

It is imperative that you read the above article as it will show you as to why so many people are in debt nowadays because of credit cards. Only after reading it, only then may you proceed to take the rest of this Credit Card Tutorial or else you may just end up joining the hundreds of thousands permanently stuck in the shit hole of debt and become poorer by the day. I am not joking and you have been warned.

CREDIT CARDS ARE CASH COW FOR THE BANKS

Financial Institutions make tons of money from credit cards and that is why you will find that all banks in Malaysia are credit card issuers.

The card issuer earns a commission whenever you use their credit card. So, the more people using their credit cards, the more money they make.

The banks also make money from cardholders who fail to settle their monthly credit card bills in full. As I mentioned earlier, the bank will impose interest on unpaid balances. And in my article LIFE – Goal Is To Be Debt Free, I have shown you in 2010 that only 30% of cardholders pay their credit card bills in full every month. The rest of the 70% has a total outstanding credit card debt of RM30,8000,000,000!!!

Assuming that all the banks impose a 10% interest on the above mentioned RM30.8 billion, that equates to RM3.800,000,000 in profits for the banks!!! Now, credit card interest rates are much higher than 10%. It can be as high as 18% or even 20%; which means the profits the banks made is much higher than what is mentioned in this paragraph and the combined cardholders who were imposed interest were getting poorer by the same amount yearly.

The credit card industry is a very lucrative business for banks/credit card issuers as they charge exorbitant interest rates (compared to OPR/BLR) on Outstanding Balances. On the other hand, it is also a very competitive business where banks compete among each other to ensure that card holders use their bank’s issued cards.

So, the banks have to constantly come up with “benefits” as marketing gimmicks to attract new customers and retain existing cardholders. Don’t be mistaken that the banks are being generous, because the money they spend in dishing out the benefits is peanuts compared to the profits they make from imposing interest onto those who fail to settle in full their credit card bills monthly.

But for the minority 30% of cardholders in Malaysia who do pay their credit card bills in full every single month, my articles and this tutorial will teach you how you can earn FREE pocket money by optimizing the benefits that come with the right credit card based on your spending pattern.

Before I go into detail as to how you can earn extra FREE Pocket Money by owning the right credit cards, I will present and highlight to you the basics of credit cards first. But, more importantly, credit card is a very dangerous tool that can lead you straight into the shit hole of debt. Once you fall into the shit hole of debt, it is very hard to get out.

BANK NEGARA MALAYSIA GUIDELINES FOR CREDIT CARDS

On 18th March 2011, Bank Negara Malaysia announced 3 very significant new rulings on credit cards:

1. The minimum income requirement to qualify for a credit card was raised to RM24,000 per annum from RM18,000 previously.

2. For those earning less than RM36K per year, he/she can only hold credit cards from two different issuers. One can have as many credit cards from the same issuer, for example, Maybank Visa, Maybank MasterCard, Maybankard MU, Maybank Petronas Visa and etc.

3. For those earning less than RM36K/year, the credit limit shall not be more than 2X his/her monthly salary from a particular card issuer.

If you had read the prelude to this article, i.e. LIFE – Goal Is To Be Debt Free, you will understand why BNM had to take these drastic measures.

Prior to BNM’s announcement as mentioned above, it was pretty easy to get a credit card if one already holds a credit card for more than a year. The banks would issue a credit card to an applicant based on their credit history and assign credit limit of more than 3X one’s monthly salary without any documents. A person earning RM2K/month can have as many as 10 credit cards or more, and each card may have a credit limit of 10X his monthly salary. Don’t believe me, well I became a jobless bum on 1st January 2011 and look at how many credit cards I have today. Previously, while still a salaryman when applying for a credit card, I would just fill in my salary as “> RM100K pa” (never actually stating my real income except once when I wanted to upgrade to CIMB World Master Card) without submitting any documents and guess what? The banks will award me credit limit of 6 figures!???

But that is history. In view of the recent BNM ruling, in particular, item 2 and 3 above, the banks now require most new applicants to submit proof of their income. Not only that, you are now required to state your liabilities (e.g. housing loan and car loan) which must be taken into consideration by the banks when approving a credit card to you.

CREDIT CARD ANNUAL FEE

I have never paid any annual fees for more than a decade, should any bank not waive my annual fees in full, I would cancel the credit card with that bank as it does not make any sense to pay for services that I can get for free.

Seriously, if you are paying annual fee for a credit card and not getting more in returns monetary wise, then you are a fool! Here are two examples:

Citibank Prestige Elite World MasterCard – annual fee RM1060

This card gives you a Priority Pass Membership Card that grants you UNLIMITED access to airport lounges worldwide. If for example, you travel every week by air and you get to utilize your Priority Membership Card every time you travel, the cost to enter an airport lounge equates to RM20.38 (RM1060/52 weeks). For those who do enjoy FREE alcohol at the airport lounges, it may be worth to pay the RM1060 annual fee.

But, on the other hand, if for example you enter airport lounges 4 times in a year, then it cost you RM265 per visit!!!

The Citibank Prestige World MasterCard earns 2X Reward Points for Overseas Spending which can be considered as pathetic compared to many other Premier credit cards which earn you 5X Reward Points (which allows them to redeem for FREE Business Class ticket sooner).

Maybank Visa Signature – annual fee RM583 (including 6% GST)

This card gives you 5% cash back for Petrol and Groceries everyday. The monthly cash back is capped at RM88. You and your supplementary card(s) are entitled to 5X (separate) FREE access to Plaza Premium Lounge.

Say you do use the Maybank Visa Signature and spend RM1200 per month for your groceries and petrol. This means you will earn RM720 per year (RM60 x 12 months) in cash back. Therefore, after deducting the annual fee of RM550, you are still earning extra FREE Pocket Money of RM137.

If you do fly twice a year with your wife overseas and use your Maybank Visa Signature and your wife, her Supp FREE FOR LIFE Visa Signature, to enter KLIA Plaza Premium Lounge; the four visits to the Plaza Premium Lounge cost you nothing since you are already earning extra pocket money as shown in the paragraph above (versus the guy who “paid” RM20.38 every time he visits an airport lounge with his Citibank Prestige Elite World MasterCard!!!)

In this example, it is worthwhile to pay the Maybank Visa Signature Annual Fee of RM550 since you are not losing anything but actually earning RM720 per year with RM1200 per month spending on essential transactions required for your daily survival; and becoming richer by RM137 by simply using the Maybank Visa Signature.

There are many credit cards nowadays that offer some kind of automatic annual fee waiver when you swipe a minimum of 12 times a year or with minimum spending or the best are those which are FREE FOR LIFE without any conditions.

And I am going to share with you a secret – the best credit cards that earn you the most in EXTRA Pocket Money are those which are FREE FOR LIFE without any conditions or with auto waiver mechanism (i.e. you do not need to call Customer Service and beg for annual fee waiver)! You will learn more in due time as you read my many credit card reviews.

Examples of FREE FOR LIFE Credit Cards without any conditions.

- AmBank – Visa Infinite, World MasterCard, Visa Signature, Platinum/Gold Visa and MasterCard.

- CIMB – Visa Infinite, World MasterCard, Visa Signature, Cash Rebate Platinum MasterCard, Platinum/Gold Visa and MasterCard.

- Hong Leong Bank – Visa Infinite.

- Maybank – Maybank 2 Platinum/Gold Cards, Maybank Islamic MasterCard Ikhwan Platinum/Gold and Petronas Visa Platinum/Gold.

- OCBC – Blue/Pink MasterCard.

- Public Bank – Visa Infinite and Petron Visa Gold

- RHB – Visa Infinite, World MasterCard and Visa Signature.

Examples of Credit Cards where the Annual Fees are auto waived with 12 swipes a year. (Please note not 1 swipe per month but total in a year).

- AEON – Gold MasterCard/Visa and Watami Visa

- Alliance Bank – Platinum and Gold Visa and MasterCard.

- Hong Leong Bank – Essential Visa and MATTA Visa

- Public Bank – Visa Signature, Platinum Visa/MasterCard and Gold Visa

Examples of Credit Cards where the Annual Fees are auto waived with minimum spending.

- Alliance Bank – Visa Infinite (RM30K)

- Maybank – Maybank 2 Cards Premier (RM80K) and Visa Signature (RM50K)

- CIMB – Enrich World Elite MasterCard (RM1,000,000!!!)

The above are just some of the credit cards which you can get for FREE. So, if your credit card charges you annual fee, then you have to waste your precious time calling up Customer Service to request for waiver. And if they refuse to waive the annual fee after you have begged them, then you will feel like a dumb-ass for not getting a FREE FOR LIFE credit card, hahaha.

CREDIT CARD Versus CHARGE CARD

A tutorial by GenX @ http://www.GenXGenYGenZ.xom

CREDIT CARDS

In the case of Credit Cards, the banks will assign you a Credit Limit where you can transact with your credit card up to the said limit. For example, you are assigned a credit limit of RM3,000. You then can use your credit card for a single transaction or many transactions up to a total of RM3K only. Once you hit your credit limit, your transaction may be declined (why I say “may” is because some credit card issuer may allow you to go beyond the credit limit assigned to you and then charge you a fee!)

Still don’t understand? Say on 28 February 2016, you were approved your very first credit card and the credit limit is RM3K. You then go transact with the card as follows:

On 2nd March 2016 – you pay for petrol costing RM100 (credit available RM3,000 – RM100 = RM2,900)

3rd March 2016 – flowers for date RM50, dinner with date RM100 and clubbing RM150 (credit available = RM2,900 – RM300 = RM2,600)

4th March 2016 – buy a new smartphone that cost RM1800 but with 12 months installment plan (credit available = RM2,600 – RM1,800 = RM800). Yes, installment plan will use up your credit available.

5th March 2016 – take girlfriend to movie RM30 and dinner RM50 (credit available = RM800 – RM80 = RM720)

11th March 2016 – spend RM300 on clothes (credit available = RM720 – RM300 = RM420)

14th March 2016 – power lunch with client, bill comes to RM488. Pass the credit card to waiter and waiter comes back to you and say your card was declined. Why? Because you have used up RM2,580 credit (inclusive of the installment plan) and only have remaining available credit of RM420 and with the RM488 bill, it would surpass your credit limit of RM3K. Luckily you have RM500 cash in your wallet to pay the bill, hahaha.

FYI, you can pay back to the bank anytime even before the Due Date. Say if you had repaid RM500 on 11th March, your credit available will then increase by the same amount, i.e. RM420 + RM500 = RM920 and the transaction of RM488 on 14th March 2016 would have gone through.

Now, you don’t have to repay anything to the credit card issuer until the PAYMENT DUE DATE. When you are approved a credit card, a STATEMENT DATE will be assigned to your account. All transactions prior to the STATEMENT DATE will be compiled and a MONTHLY STATEMENT will be generated and sent to you (either by mail or via email).

In most cases, the PAYMENT DUE DATE is generally 20 days from the STATEMENT DATE. Assuming your STATEMENT DATE is every 8th of the month, in this case, the PAYMENT DUE DATE will fall on 28th March 2012.

Here is an example which you would most probably see if log into you Internet Banking Account on 15 March 2016:

STATEMENT DATE: 8th March 2016

PAYMENT DUE DATE: 28th March 2016

STATEMENT BALANCE: RM630 (sum of all transactions before or on 8th March 2016, in this case RM100 (on 2nd March 2016) + RM300 (on 3rd March 2016) + RM150 (4th March 2016 Smartphone 0% installment plan – RM1800/12 months) + RM80 (on 5th March 2016)

OUTSTANDING BALANCE: RM930 [Statement Balance (RM630) + whatever transactions after Statement Date (RM300 on 11th March 2016)]

MINIMUM PAYMENT RM50 (5% of Statement Balance which is RM31.50 but the minimum must be RM50)

AVAILABLE CREDIT (this may or may not be shown to you) : RM420 (remember, installment plan will take up your credit available).

To avoid paying a single sen of INTEREST and or LATE PAYMENT PENALTY, you must SETTLE IN FULL THE STATEMENT BALANCE (RM630 in the case above) prior to the PAYMENT DUE DATE (28 March 2016). But if you are paying by cheque (or even via GIRO), make sure you allow 2-3 working days for the payment to be cleared. If you miss the payment date by 1 or 2 days because of some valid reason, you can always call up Customer Service to request that they waive the LATE PAYMENT PENALTY.

Now, if you don’t pay in full the STATEMENT BALANCE before the PAYMENT DUE DATE, you will be imposed INTEREST CHARGES on the unpaid balance on a daily basis! So, it is imperative that you SETTLE THE STATEMENT BALANCE IN FULL prior to the DUE DATE. If you cannot pay in full, my advise is don’t get a credit card because you are spending beyond your means and you’ll get poorer every day until you make full payment. I will touch on this again in the next post on my series on Credit Card for Newbies: CC114 – Credit Card Interest Rate.

CHARGE CARD

Unlike credit cards, charge cards do not have a credit limit. Now, it is not to say that you can charge whatever you like to the card. There will still be a “Credit Line” or some call it “Shadow Credit Limit” just like credit card’s Credit Limit. You can always call Customer Service and ask them what is your Credit Line amount, so that you won’t be in a face losing situation when your transaction is declined because you have gone beyond the Credit Line assigned to you. The card issuer will increase your Credit Line with time based on your spending pattern and ability to repay back.

For charge cards, a MONTHLY STATEMENT will also be issued. Unlike Credit Cards, where the card holder can only pay minimum payment, charge card holders are required to SETTLE IN FULL whatever amount that is stated in the MONTHLY STATEMENT before the DUE DATE.

INTEREST FREE PERIOD

All credit cards have a Statement Date where all your transactions prior to that date will be accumulated and must be paid before the Payment Due Date, otherwise you will be charged interest on the Outstanding Balance after the DUE DATE. The time between the Transaction Date of a particular transaction and the Payment Due Date is the interest free period and it is usually about 20-45 days.

Here is an example:

STATEMENT DATE is on the 8th of every month.

PAYMENT DUE DATE is on 28th of every month.

Lets say you purchased on 7th March 2016. The said transaction shall be due for payment before 28th March 2016, thus you get about 21 days interest free credit.

To enjoy a longer interest free period, purchase the item on 9th March 2016 (after the STATEMENT DATE) and payment will only be due the following month on 28th April 2012. This means you enjoy more than 40 days interest free credit. If the said purchase was RM10,000, you could have deposit the money in Fixed Deposit for a month and earn interest of approximately RM25 (based on interest of 3% PA) for the said purchase.

Please note that Interest Free Period only applies when you don’t have a single sen of outstanding balance. Finance Charges may be imposed immediately onto all new transactions if you have not Settled In Full the previous Statement Balance prior to the Payment Due Date.

CREDIT CARD INTEREST RATES

As I mentioned before, credit card interest rates for outstanding balance is exorbitant. If you pay the minimum 5% payment it will take years to clear your outstanding balance.

Once again, please take note that Finance Charges may also be imposed on new transactions if you have failed to pay in full the Statement Balance prior to the Payment Due Date.

This subject will be revisited in my second article in my series for credit card beginners.

My principle is never to let the banks charge me a single sen of interest from my credit card usage. You should adopt this principle too, and never say just once, because if you break your principle once, what’s there to stop you from breaking it a second time.

If you are a salaryman without any savings in the bank and you just manage to scrape through monthly, think twice before you swipe your card. If you don’t have money today, what makes you think you’ll have money to pay back tomorrow? Yah, if “kena” Jackpot or 4D then different story lah, so “kena” first then only talk.

Here is a free advise to you, if you do have OUTSTANDING BALANCE and are paying interest, DO NOT use that card because you’ll be imposed daily interest on new transactions from the day you swipe the card. If you need to use a credit card, USE ANOTHER CREDIT CARD WITHOUT ANY OUTSTANDING BALANCE and you will enjoy the interest free period like I mentioned above.

DO NOT WITHDRAW CASH WITH CREDIT CARD

Do not practice withdrawing cash from ATM or transferring funds into banking accounts using your credit cards as you are charged 5% advance interest on the same day and then daily at 18% (per annum rate) until you make full payment. If you are withdrawing cash using your credit card on a regular basis, it means that you are living beyond your means and you should cut the card in half.

If for instance you withdraw cash with your credit card, and you pay back in full within a month, the fixed 5% withdrawal fee will amount to 60% interest rate (5% x 12 month)! Once again, never ever withdraw cash with credit cards.

CREDIT CARD Versus CASH

Always use your credit card when you can instead of paying with cash if the merchant does not charge any surcharge for using your card. The benefit of using your credit card is that you get reward points which you can redeem later or even get cash back if your card has the program.

However, most credit cards have expiry dates for their reward points such as CIMB, Maybank and UOB. Some credit cards’ rewards points are evergreen BUT ALL credit card issuers will inflate their redemption program with time, i.e. you will need more reward points to redeem for stuff.

So if you do not use credit cards often, it is better to get cash back credit cards where the cash back is credited monthly into your credit card account to offset your bill.

However, if a merchant imposes a surcharge of 2% with your purchase, then it may be more logical to pay cash as 2% is “like” equivalent to 24% interest when annualized, assuming you will be paying for the purchase within a month.

At times you get discounts at participating outlets when using your credit card whereas you don’t even get a single sen if you pay with cash. As different credit cards offer discounts at different outlets, this is the only reason I would think it is beneficial to have several cards.

DISCOUNTS AND OFFERS

Most credit cards issued by major commercial local banks and foreign banks offer limited time discounts at many outlets.

Always ask if there is any discount for any credit card especially if you have several credit cards before paying the bill. I can’t keep track of which credit cards have discounts at a particular merchant but by asking this simple question it has saved me money on several occasions.

Also during festive seasons, CIMB, Citibank, HSBC and Maybank usually give free gifts for using their cards when you swipe above a certain amount. During past Christmas and Chinese New Year periods, HSBC was giving free gifts at Gardens and Mid Valley, CIMB was giving free gifts at Sunway Pyramid and Maybank at 1 Utama.

Therefore, do check out your card issuer’s website frequently to find out the latest offers and promotions.

REWARD POINTS REDEMPTION

Generally, RM1 spent = 1 Point. However, some cards may offer 2X to 5X Reward Points for every Ringgit spent.

But Reward Points required for redemption varies for each credit card, i.e. Citibank has different Reward Redemption Catalog for different cards.

So, when choosing a Reward Points Credit Card, the above two criteria must be taken into consideration. The best way to compare Reward Points credit cards is to convert them to equivalent cash back when redeeming for cash voucher(s). Here are some examples as of 1st January 2016:

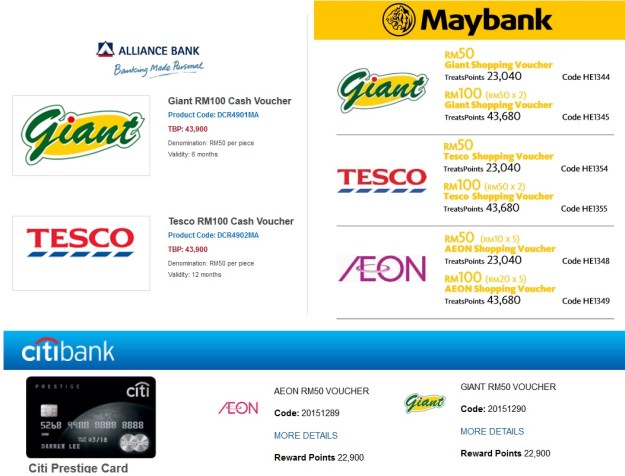

Alliance Bank Visa Infinite non PB – Annual Fee waived with RM30K Spending. 43,900 Timeless Bonus Points are required to redeem for RM100 Giant or Tesco Cash Voucher.

- 2X Timeless Bonus Points for local spending. Therefore this works out to 0.45% equivalent cash back.

For those who are blur as to how I came up with the equivalent cash back above, I will now show you a sample calculation:

In order to earn 43,900 Timeless Bonus Points from your local spending, you will need to spend RM21,950 with the Alliance Bank Visa Infinite.

Therefore the equivalent cash back =

RM100 Cash Voucher/RM21,950 spent x 100% = 0.45558%

- 5X Timeless Bonus Points for overseas spending. Therefore this works out to be 1.14% equivalent cash back.

Citibank Prestige World MasterCard – Annual Fee RM1060. 22,900 Reward Points are required to redeem for RM50 Giant or AEON Cash Voucher.

- 1X Reward Points for local spending. Therefore this works out to 0.21% equivalent cash back.

- 2X Reward Points for local spending. Therefore this works out to 0.44% equivalent cash back.

ENTRY LEVEL Maybank 2 Gold Cards – FREE FOR LIFE. 43,680 Treats Points are required to redeem for RM100 AEON/Giant/Tesco Cash Voucher.

- 5X Treats Points with the AMEX for local spending. Therefore, this works out to 1.14% equivalent cash back.

- 5X Treats Points with the AMEX for overseas spending. Therefore, this works out to 1.14% equivalent cash back.

From the above, you are shown that Premier Credit Cards DO NOT necessarily give you more in returns compared to a FREE FOR LIFE Entry Level Credit Card. So, do not blindly apply for a Platinum Credit Card without comparing the benefits versus a Gold Card. For example, Hong Leong Bank Wise Platinum and Gold Visa cards have the exact same benefits but the Platinum’s annual fee is higher.

I have bad news for you guys, over the years, card issuers have been increasing the points required to redeem cash vouchers. In actual fact, many banks now require more than 20,000 points to redeem for RM50 cash vouchers. So, it is better to redeem your reward points yearly and always check for announcements by your card issuer as most of the local banks would give you advance warning before they inflate their rewards redemption program.

The good news is, nowadays, more and more card issuers allow their cardholders to redeem their points on the spot at selected merchants and not requiring us to call Customer Service. One benefit of this redemption at merchants is that we can use the points to pay for the bill in full or partially. We no longer need to wait until we have 10,000 points, for instance to redeem cash vouchers. Best of all, it is easier for us to use up the remaining points when we intend to cancel a particular card. Examples of On The Spot Redemption/Pay With Points as of 1st January 2016:

CIMB – Pay With Points RM1 = 250 Points

Citibank – Instant Rewards Points RM1 = 400 Points

Maybank – On The Spot Redemption RM1 = 400 Treats Points

CASH BACK CREDIT CARDS

As you can observe above, nowadays the returns we get with Reward Points credit cards are damn freaking pathetic, almost negligible especially from local spending except with the Maybank American Express where we still can earn above 1% equivalent in cash back when redeeming for cash vouchers.

The credit card industry is a very lucrative business for banks/credit card issuers as they charge exorbitant interest rates (compared to BLR) on Outstanding Balances. The competition is so intense that card issuers have to come up with more benefits (gimmicks) to retain or attract new customers. One way is by giving their customers the impression that they are offering better than 0.5% returns.

The current trend now is to award Cash Back/Rebate to card holders for swiping their cards. These cash back benefit can either be a permanent card feature or a limited time promotion.

Examples of Cash Back Credit Cards (local spending only) where the cash back is guaranteed as it is a standard card feature (please note, most cards do not reward any cash back for Petrol):

Citibank Cash Back Visa or MasterCard (Annual Fee will be imposed) – 2% to 5% Cash Back on Selective Transactions with monthly cap of 0.2% cash back for general retail spending.

CIMB Visa Infinite FREE FOR LIFE – UNLIMITED 0.5% and 1% cash back for local and overseas spending respectively.

CIMB Cash Rebate Platinum MasterCard FREE FOR LIFE – 5% Cash Back for Online Transaction but there is a cap on the monthly cash back plus other Terms and Conditions.

Hong Leong Bank Essential FREE with 12 Swipes – UNLIMITED 1% cash back for all types of transactions except petrol.

Hong Leong Bank Wise Visa (Annual Fee will be imposed) – 10% Cash Back on 2 Categories (where one of the category can be for Petrol) with T&C.

OCBC Titanium MasterCard FREE FOR LIFE – UNLIMITED 1% cash back for online and overseas spending. 0.1% cash back on all other retail spending!

Public Bank Credit Cards FREE with 12 Swipes – 0.3% cash back for Classic, 0.3% – 0.5% for local spending with the Platinum.

RHB Visa Signature FREE FOR LIFE – 1% to 6% Tiered Cash Back for Online with monthly cap. Overseas 0.5% to 2% Cash Back with monthly cap.

RHB World MasterCard FREE FOR LIFE – 1 % to 6% Tiered Cash Back for Travel, Petrol and Dining with monthly cap. Others 0.20% cash back.

UOB One Card (Annual Fee will be imposed)- 0.2% to 5% Cash Back depending on the type of transaction with monthly cap and other Terms and Conditions..

Once again, the above cards’ cash back are standard card features where you are guaranteed the cash back (up to the maximum monthly cap where applicable).

Now, please be informed that nowadays many credit cards issuers will also promote their credit cards claiming they offer 5% cash back for this and that. But, in actual fact they will allocate a certain amount to be given away for the promo and the cash back awarded based on first come first serve basis. I.e. the cash back is not guaranteed!

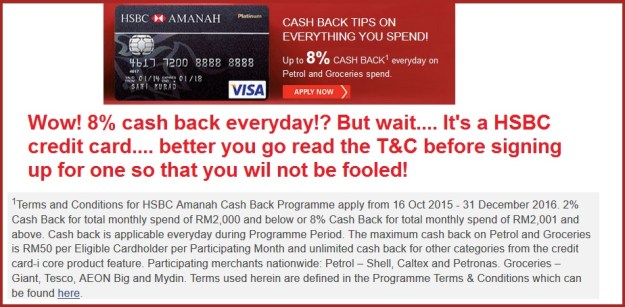

If you have been following my blog(s) for years, you will know that I always reiterate that HSBC is the most insincere credit card issuer in Malaysia as they will mislead us with their marketing gimmicks.

For those of you who are new to my blog, if you ever want to apply for a HSBC credit card, make sure you read the terms and conditions. This is because what HSBC advertised as benefits are usually limited time promotions and are designed to fool you by giving you the impression that their cards are better than their competitors. Here’s an example of how you may be fooled by HSBC marketing people when they promote to you their so called 8% cash back for petrol and groceries with the HSBC Amanah MPower Visa Platinum Credit Card-i.

The terms and conditions state that you will get 2% cash back for Petrol and Groceries for spending RM2K and below and 8% Cash Back for total spending of RM2001 and above. Also please note that cash back of 2% is only applicable for Petronas, Shell and Caltex. For Groceries, the 2% cash back is only at AEON Big, Giant, Tesco and Mydin. All other transactions will only earn you 0.2% cash back.

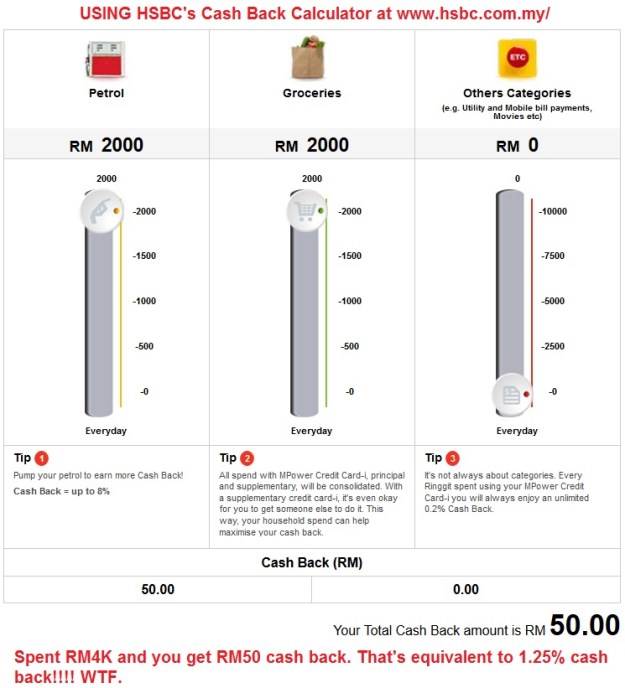

Let’s use the Cash Back Calculator at HSBC website and see how much we can earn with RM2K spending for Petrol and RM2K spending for Groceries.

Spend RM2K on Petrol and RM2K on Groceries and you will only get 1.25% cash back and not 2%!!

Okay, you may argue that the above is not a very good example to show how insincere HSBC is, since the monthly cash back is capped at RM50. Well, please reread HSBC advertisement above again where it states that one earns up to 8% cash back for petrol AND groceries everyday. I have just proved to you that by using HSBC’s own cash back calculator that it is impossible for anyone to earn 8% cash back for petrol AND groceries!

If HSBC was really sincere, their ad should have stated up to 8% cash back for petrol OR groceries and not both.

Let’s say we spend RM3K on petrol, let’s see how much we get. WTF! How come HSBC calculator won’t let me spend more than RM2K for petrol to see how much I can earn from the 8% cash back before I hit the RM50 cap?? I guess I have to go calculate manually.

We will get cash back of RM40 from the first RM2K spent on petrol. I.e. RM2K x 2% = RM40.

So for the next RM1K spent on petrol, I expect to get 8% right. So RM1000 x 8% = RM80. Wait a minute, the monthly cash back cap is RM50 only. Therefore, I am actually only earning RM10 in cash back for this said RM1K spent on petrol, i.e. RM40 cash back for the first RM2K spent + RM10 for the next RM1K spent. This means my actual cash back is 1.67% (RM50/RM3000 x 100%)!!!

From these two examples, I am already pissed off with HSBC!! But I will tell you what is the real deal with HSBC’s so called up to 8% cash back.

Once again, if you spend RM2K on petrol, you will earn RM40 cash back, i.e. 2%. Since the cash back is capped at RM50 per month, that means you have remaining RM10 cash back for the 8% cash back portion or in other words, good for petrol spending of another RM125 only!!! RM125 for 8% cash back portion is really freaking pathetic/insignificant to those who spend more than RM2K on petrol.

What a joke! Whoever came up with the marketing gimmick of 8% cash back for Petrol AND Groceries with the HSBC Amanah MPower Visa Credit Card -i, should be awarded the title of the greatest bullshitter on earth, hahaha.

The actual fact about the HSBC Amanah MPower Platinum Credit Card -i is that it will earn you UP TO MAXIMUM 2.35% (RM50/RM2,125) for Petrol OR Groceries (not both) and not up to 8% as claimed/mislead by HSBC.

I tell you, I am insulted that HSBC, a global bank, have been misleading the general public and thinks that all Malaysians are fools. Only my readers/followers and those who actually read and comprehend the T&C of HSBC credit cards won’t be fooled. For the betterment of the general public who don’t read my articles, I hereby demand that Bank Negara Malaysia revoke HSBC’s Credit Card License with immediate effect. And all those people who market HSBC credit cards (including those co called Financial websites that recommend to their readers that they earn 8% cash back for petrol AND groceries with HSBC Amanah MPower Platinum -i and earns commission whenever one applies for a HSBC credit card through them) be charged in the court of law for fraud!!!

HYBRID CREDIT CARDS

And then there are some credit cards that reward you both UNLIMITED Reward Points and Cash Back with monthly cap.

Maybank 2 Platinum/Gold Cards FREE FOR LIFE – UNLIMITED 5X Cash Back for both local and overseas spending (except for Education, Insurance and Government 2X) PLUS 5% cash back for Dining every weekend with monthly cap of RM50.

Maybank Islamic MasterCard Ikhwan FREE FOR LIFE – 5% guaranteed cash back for petrol at ALL PETROL STATIONS every Friday and Saturday (monthly cap RM50) and 1X Treat Point for every RM1 spent locally or overseas.

Maybank Visa Signature Annual Free waived with RM50K spending – 5% cash back for petrol and groceries EVERYDAY ( monthly cap RM88) and UNLIMITED 1X and 5X Treats Points for every RM1 spent locally and overseas respectively.

Public Bank Visa Signature FREE with 12 Swipes – 6% cash back for Dining, Online and Groceries (where the monthly cash back is capped at RM50) and VIP Points.

PETROL & GROCERIES PURCHASES

Petrol and groceries are essential items required by most. As such we should get a credit card that gives us some returns whenever we purchase groceries and/or pump petrol.

Most credit cards do not offer reward points for purchase of fuel. American Express on the other hand rewards its members points for transactions at petrol stations. The Best Credit Cards for Petrol (and Groceries) are those which offer 5% guaranteed cash back without any conditions, i.e. Maybank Islamic MasterCard Ikhwan FREE FOR LIFE without any conditions where the monthly cash back cap is RM50 and Maybank Visa Signature where the annual fee is auto waived with RM50K spending and the monthly cash back is capped at RM88.

Once again, other credit cards may claim that they offer 5% cash back for Petrol and Groceries but I can tell you they are simply marketing gimmicks and not guaranteed. You are hereby warned to read the terms and conditions of any credit cards before applying for one especially when it comes to HSBC credit cards.

Citibank Cash Back gives you guaranteed 5% cash back for Petrol BUT the monthly cash back cap is really low and you need to pay the card annual fee; and after taking these matters into consideration, you will earn peanuts in return from your Petrol Transactions.

A really good credit card for Petrol is the Hong Leong Bank Wise Credit Card where you can earn 10% cash back for petrol and best of all, the monthly cash back cap is RM100! However, in order to be eligible for the cash back, you need to swipe minimum RM50 at least 10 times within a month. In my article The Best Top 10 Credit Cards in Malaysia 2016, I will teach you how you can benefit from the Hong Leong Bank Wise Visa credit card.

0% INTEREST FREE INSTALLMENTS

Most banks offer some kind of interest free installment plan for purchases like handphones, computers, furniture and other electrical goods through third party vendor(s) or participating merchants. These interest free offers can be viewed in the respective bank’s websites and sometimes it comes in brochures together with your statements. However, prior to purchasing the items advertised in their website, I would recommend that you check out the item in the malls first as sometimes the offers are more expensive than what is being sold in the market.

Courts, Harvey Norman, SenQ, Best Denki and many other merchants also have 0% installment plans. But in Harvey Norman’s case, I suggest you always ask if there’s a further discount as I have managed to get discounts for electrical goods there.

Sometimes when purchasing an item using the 0% interest free installments, you may end up paying more for the item. For example, years ago I was informed at Cellini, Subang Parade that I can get 12 months 0% installments for certain cards but they give 5% additional discount on top of the sale price if I were to pay in full using the same credit card. When I bought my son a HP notebook at Harvey Norman many years ago with my AMEX, they gave me RM100 discount with the condition that I don’t go for 0% installment plan. Same case at OTO, I wanted to get a foot massager, I got further discount from the promo price when I paid in full with my AMERICAN EXPRESS instead of opting for 0% installment plan.

So, from the above, always ask if there is any further discount even if you are told the item is on promotion because the merchant would have most probably included the “cost” of the installment plan into the promotional price. If you can save 5% (even better lah), that’s even better than current Fixed Deposit interest rates.

Having said the above, in late 2014, I wanted to get a Gaming Notebook which was selling like hot cakes for my son and eventually I bought it at All IT at Low Yat Plaza. Most other shops did not have stock or were selling the Gaming Notebook at retail price, i.e. no discount. All IT had stock, and I was expecting to pay retail price for the Gaming Notebook; but, to my surprise, I was given a discount by simply asking and best of all, I could use my Maybank Visa Infinite and earn 2X TP and opt for 0% installment plan without being charged a single sen extra!!! If you are new to my blog, almost all my articles have something to do with credit cards. Therefore, it is best to shop around before buying anything.

Some banks may also claim that they offer so called 0% interest installments for any kind of transaction anywhere but it is not really 0% because they charge between 2% to 7% UPFRONT for the easy payment plan. Once again, you should avoid paying any kind of interest from your credit card usage.

Now, I always say 0% installment is a trap by the banks, especially if you don’t have the cash in hand. You may argue that the reason you are opting for 0% installment plan is you don’t have the cash in hand. Well, my answer to you is that you are spending beyond your means if you are buying the stuff not required for your daily survival – no money but want to buy material stuff for temporary happy moments.

I will show you later that 0% Interest Rate Installment Plan with Credit Cards Is A Trap to trick you into falling into the Shit Hole of Debt soon.

BALANCE TRANSFER

Credit Card Tutorial by GenX @ http://www.GenXGenYGenZ.com

If you are using this facility (the credit card issuer calls this a Card Benefit), then most probably you are living beyond your means. Some banks may even offer 0% Interest Balance Transfer Plan for a few months. This is because they know that since you can’t pay up at the other bank, the probability of you paying them 18% interest and giving them fantastic profits after the expiry of the 0% period is very high.

Actually this is my favorite subject relating to Credit Cards, especially if it is 0% Interest Free Balance Transfer Plans. I will also touch on this in my Tutorial CC 254.

EASE OF PAYMENT

Those of you who do online banking, paying credit card bills via this method saves you time.

But for those who do not believe in internet banking for security reasons (kiasulah), choose a card where you can make payments at the issuer branches at whatever time most convenient to you. For example, your office is walking distance to the bank or there is a branch near your home for you to make payments anytime (via Cash Deposit Machine or Cheque Deposit Machine). This will save you the hassle of getting stuck in traffic jams or looking for parking space or burning extra petrol just to go make a single payment.

24 CUSTOMER SERVICE

Some of us may be very busy during the day. Therefore, only have time to call customer service late at night. Also making calls after 7pm on my Maxis postpaid saves me money and calling late in the night also reduces the probability of me being put on hold for too long. Banks with true 24 hour Customer Service that I know of are Maybank and UOB where you can even redeem reward points at midnight! Some banks may claim they offer 24 hour customer service for its Platinum card holders; but most of the time the operator can’t help you much after 10pm except for reporting lost cards.

From my years of experience calling Customer Service, the best 24 Hour Customer Service are Maybank Premier Cards Customer Service and American Express. And best of all, they are Toll FREE!

FRAUD RELATING TO CREDIT CARD AND SMS ALERT

Having a credit card may also cause you headaches when your card is cloned or stolen. In the event your credit card is stolen and you are not aware of it, some banks will hold you fully responsible for all fraudulent charges up to the point when you call in to report the card was lost or stolen! So, no point in having a high credit limit should you not require it, you can always call Customer Service to request for your credit limit be reduced to the amount you actually need.

And nowadays, with online shopping, anyone having access to your Visa or MasterCard 16 digits card number and the 3 digits CCV security number (behind the card) can go purchase anything worldwide. However, many of the major commercial banks have implemented better security features for their credit cards, for example, a password will be sent to your mobile phone via SMS for you to key in before the transaction can be approved.

And in 2015, BNM instructed banks to disallow overseas online transactions with debit cards unless it is requested by the cardholder. But some banks went even further and will not allow online transactions with specific merchants, e.g. Stream where many purchase credit for online games!

Another fraud that is rampant is that you may get fake calls from people claiming they are from the bank or even police conning you into giving out your personal information like credit card number, the 3 digit CCV security number, IC Number and so on. And the calls are not only from mobile phones but your caller ID may show actual genuine telephone land line numbers from banks and even police stations. My advise is, never ever release any information to anyone who calls you over the phone, hang up and call Customer Service (telephone number behind your card) to verify any calls claiming they are from the banks.

Effective 1st January 2012, banks are supposed to sent out SMS whenever a transaction is performed with our credit cards. Most banks will sent out SMS to the card holder for online and auto debit transactions BUT NOT NECESSARILY for face to face transactions where you present your card personally. This is because most of the banks have set their own default value to trigger the SMS Alert. The good news is some banks do allow you to change the default value, and if they don’t, send an email to BNM.

Please read CC 201 – Credit Card Fraud and Bank Value for SMS Alert so that you will not regret later should you get a fraud call and get conned. This is free info that should not be missed and don’t give me the opportunity to say – “I told you so”.

OVERSEAS USAGE

Having a credit card makes it convenient for us to make payments without having to carry much cash with us. This is especially useful when we go overseas. However, you are to note that you’ll be charged an overseas admin fee/conversion factor. That is why card issuers can give you up to 5X Reward Points for overseas transactions.

And if you do go overseas often, make sure you have at least 2 credit cards from two (2) different issuers, just in case one of them cannot be used for whatever reason. We do hear of people not being able to use their credit cards overseas. However, I have not encountered any problems using any of my credit cards so far.

Having said the above, I would still recommend that you inform Customer Service when you are going abroad so that it can be reflected in your card issuer’s system. IF you don’t inform them, you may receive a call from the card issuer to verify the transaction and that means you’ll end up paying for the overseas call!

BEWARE OF CREDIT CARD INSURANCE PROMO

Many many years ago, I signed up for a Personal Accident Insurance Policy with my UOB credit card. It had a trial offer where I got a certain period of the coverage for free. After the trial period, if I did not cancel the policy, it would be deemed that I agreed to continue with the policy. At that time I just started working and PA insurance was a cheap way to insure myself, so I continued with the policy. Then a few years back I wanted to cancel my UOB Platinum credit card because the card does not offer much benefits. I called the insurance company to transfer the auto debit payment to another credit card and I was told that I couldn’t do so because the insurance policy was a joint promo with UOB! Therefore, I had no choice but to keep the damn card till today, unless I am willing to give up the policy. Take note of this, do not sign up for insurance policies offered by credit cards because you may have to give up the insurance policy when you want to cancel the card.

CONCLUSION

From the above, credit cards do benefit us instead of using cash. There are only a few simple rules to owing a credit card so that we do no end up in the shit hole of debt:

- Never ever release your personal and card information to anyone.

- Never ever withdraw cash from ATM with a credit card.

- Most importantly, do not let the bank(s) charge you a single sen of interest.

- You must have the cash in hand prior to swiping your credit card so that you are able to settle in full the Monthly Statement Balance prior to Payment Due Date.

And there isn’t a single credit card that is the “best” as each card has different benefits.

If you don’t use credit cards often, you should get a card that offers FREE FOR LIFE without a single condition.

With proper planning and the right credit card(s), we can actually optimize our earnings from credit cards and even earn FREE Business Class tickets.

And after you complete my entire FREE tutorial, you will be an expert in credit cards and maybe even join me in collecting credit cards 🙂

A Credit Card Tutorial by GenX

A Credit Card Tutorial by GenX