INTRODUCTION

On 1st April, I read at Mr-Stingy’s Facebook that BNM says a family needs RM6,500 per month to survive in KL:

Click here to Mr-Stingy.com where he has many interesting articles that are sure to benefit you one way or another.

So, I went googling and according to the Department of Statistics Malaysia, those living in Putrajaya are worst off where the median household expenditure is close to RM7K (in 2016)!

From the above, the median household expenditure in Selangor is RM5,183. What this means is that many people spend more than RM5K per month. And since most of you who are reading this are educated and should be earning big bucks, I would reckon your monthly household expenditure (combined spending of all members of your family) will be more than RM8K per month (total year expenditure divide by 12).

But the GLC financial institutions in Malaysia (i.e. Bank Rakyat, MBSB, RHB) are very generous, they will happily grant civil servants personal loans claiming they offer “low interest rate” where the repayments are auto deducted from the government employees’ monthly salary.

![]()

Well, unless you are a follower of mine, most likely you also will be fooled by banks offering so called “low interest” upfront personal loans. I tell you, signing up for personal loan(s) is the fastest way to becoming poor. If you are new to my blog, I strongly recommend that you click here now to read my article titled “Upfront Interest Rate Personal Loan or Balance Transfer – The Quickest Way To Being Poor”.

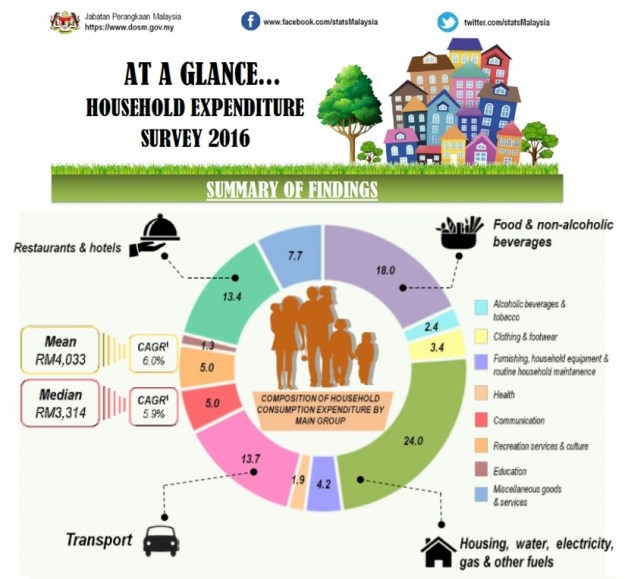

Malaysian Household Expenditure

Based on Department of Statistic Malaysia website, below shows Malaysia Household Expenditure for 2016:

From the above here is the breakdown again:

- Housing – 24%

- Food and Beverages – 18%

- Transport – 13.7% <— Car loan included?

- Restaurants and Hotels – 13.4%

- Miscellaneous goods and services – 7.7%

- Recreations services and culture – 5%

- Communications – 5% <— This is damn freaking high

- Furnishing, household equipment and routine household maintenance – 4.2%

- Clothing and Footwear – 3.4% <— today it may be more due to online shopping

- Alcoholic Drinks and Tobacco – 2.4%

- Health – 1.9% <— Insurance Premium?

- Education – 1.3% <—- education is basically free unless you sent you child to international school

Now, from the above, you will note that car loan is not mentioned, maybe it is categorized under transport. Education is kind of low at 1.3%. And the joke is Alcoholic & Tobacco 2.4% is higher than Health 1.9%. What about Insurance premiums?

Anyway, based on the results published by DOSM, except for housing (I will assume it is purely for housing loan repayments), all the expenditure can be paid using credit cards!!!

So based on BNM report that one’s household expenditure is RM6.5K per month for a couple with 2 children, what this means is RM4,940 (76% of RM6.5K) of the family expenditure can be paid using credit cards!!! That’s about RM60K per year.

In view that credit card issuers are getting stingier and inflating their redemption program almost yearly (e.g. most recent CIMB where 10,000 Bonus Points = 1,000 Enrich and HSBC 15,000 Reward Points = 1 KrisFlyer Miles), very soon we will be earning nothing or close to nothing from using our credit cards.

Therefore, before all the card issuers stop rewarding us with meaningful returns, I have come to a decision that I will teach my die hard followers, who do spend RM60K a year on top of their housing loan repayments, the Ultimate Benefit Of Owning Credit Cards where they can brag and brag for the rest of their lives. And I announced this decision at my Facebook Page on 6th April 2018.

As for young GenYs who just started working, if you and your partner are graduates, in due time you will also be earning and spending big bucks too. BUT then the credit card issuers may have inflated their reward program to the extend you earn basically nothing in return. For those of you in this category, what I would strongly recommend is that you instead save as much as you can and when we are in a recession where there is a big possibility that Maybank would drop to RM4 again you would then have the cash in hand to buy buy buy and make lots of money when the economy is on the uptrend again. Therefore, you also get to brag and brag that you bought Maybank for less than RM4, for the rest of your lives. If you have yet to read my article titled Be Prepared For Tomorrow, please click here.