Credit Card Tutorial by GenX @ http://www.GenXGenYGenZ.com

Update September 2016 – Maybank is offering 0% 12 Months Balance Transfer until March 2017 where 3% Admin Fee Waived during Promo Period.

INTRODUCTION

If you are new to credit cards, before you proceed to read this article on Balance Transfer, I suggest click here to my CREDIT CARD TUTORIAL or at the very least, read the articles below to have a better understanding of credit cards:

Prerequisite Course: Life – Pay Now With Credit Card Earn Later OR Save Now For Retirement – Goal Is To Be Debt Free.

CC 101 – Introduction To Credit Card 2016.

CC 114 – Credit Card Fees and Interest Rates.

There are 2 ways how one can benefit from 0% Balance Transfer Plans.

Benefit No.1 – For Those Who Have No Outstanding Balances, They Can Earn FREE Pocket Money

Besides earning Reward Points and/or Cash Back with credit cards, 0% Balance Transfer Plan is one of the other “real” benefit of having credit cards. For those who have cash in hand to pay for their purchases in full, Credit Card 0% Balance Transfer Plans allow them to actually earn some FREE Pocket Money by utilizing 0% Balance Transfer Plans.

Say, for example, you want to buy a Rolex Watch costing RM60,000 from Swiss Watch Gallery (Rolex Authorised Dealer) where they have outlets at Pavilion or Bangsar. And you have the RM60K cash in hand to pay in full.

However, Swiss Watch Gallery does not accept Maybank credit cards for 0% Installment Plan.

You want to use your Maybank 2 Cards Premier AMEX Reserve to earn 5X Treats Points (TP) because of the fantastic conversion of TP to either Enrich Miles or KrisFlyer Miles. I.e. spend RM60,000 with the Maybank 2 Card Premier AMEX Reserve, we can earn more than 60K Enrich Miles or KrisFLyer Miles!!! That’s more than enough to upgrade an Economy Ticket to Business Class one way KL to London (or vice-versa) with Malaysia Airline Berhad.

So, you pay for the Rolex watch using your Maybank 2 Cards Premier AMEX Reserve and then go perform a 0% 6 Months Balance Transfer Plan with 6 equal installments.

Month No.1 – Use RM10K to pay for the 1st repayment of the BT Plan. Balance RM50K deposit into 1 Month FD with 3% interest rate.

Month No.2 – Repay another RM10K towards the BT Plan. Your would have earned RM125 from the 1 month FD mentioned in item 1 above. So, balance RM40,125 deposited back into 1 month FD.

Month No.3 – Repay another RM10K towards the BT Plan. You would have earned RM100 from the 1 month FD mentioned in item 2 above. So, balance RM30,225 deposited back into 1 month FD.

Month No.4 – Repay another RM10K towards the BT Plan. Your would have earned RM75 from the 1 month FD mentioned in item 3 above. So, balance RM20,300 deposited back into 1 month FD.

Month No.5 – Repay another RM10K towards the BT Plan. Your would have earn RM50 from the 1 month FD mentioned in item 4 above. So, balance RM10,350 deposited back into 1 month FD.

Month No.6 – Repay the final RM10K towards the BT Plan. Your would have earned RM25 from the 1 month FD mentioned in item 5 above. So after settling the Balance Transfer Plan in full, you would have earned yourself RM375 FREE Pocket Money 🙂

However, sad to say that nowadays, not many banks offer 0% Balance Transfer Plans except for AEON Credit and Public Bank.

Benefit No.2 – For Those In The Shit Hole Of Debt, They Can Save On Interest Charges

Credit Card 0% Balance Transfer Plans were not created to earn you or me any pocket money; but as a marketing gimmick to attract those who have accumulated debt with their credit cards to “switch” their debt from one account to another financial institution’s account.

Generally for Balance Transfer, most banks offer lower interest for shorter Balance Transfer repayment duration. Why are the banks (financial institutions) so generous in offering 0% Balance Transfer Plan? Well, the banks know that most people who have outstanding balances have no discipline when it comes to spending. Therefore, they will attract you by offering a lower interest rate for the shorter Balance Transfer duration program, hoping that you can’t settle in full and then charge you 18% interest.

If you have read my Prerequisite Course titled Life – Goal Is To Be Debt Free, you would know by now that 70% of credit card holders have debts amounting to tens of billions.

Therefore, for those of us who are in the deep shit hole of debt because we have overspent as a result of our own doing, thank God that some banks are offering 0% interest free Balance Transfer plans.

If you are one of the millions having outstanding balance with your credit card and paying interest of 13.5%-18%, it makes sense to do a balance transfer, thus forking out less on interest payments.

However, if you do a Balance Transfer and then start to use up the available credit which has been transferred to purchase unnecessary things which are not needed for your survival and can’t settle in full come payment date, my advise is, you better just cut up the card in half and settle your debt or else you are just going deeper down the shit hole and being a slave to the banks.

You have to admit that you are living beyond your means once you do a Balance Transfer. The fact is that you are in debt. And remember, for balance transfer plans with equal installments, if you only pay the minimum or do not settle the Outstanding Balance in full prior to the Due Date, once again you’ll be imposed interest charges.

Before you sign up for a Balance Transfer Program, you have to consider the following:

1. How much can you afford to repay a month? For equal installment repayments, if you can only afford to pay part of it (minimum 5% or even 90% of your monthly Statement Balance), you will then be charged 18% interest on Outstanding Balance (including the balance of the Balance Transfer monthly installment amount if any) which defeats the purpose of you doing Balance Transfer in the first place. If you opt for equal installment repayments BT Plans, make sure you can afford to settle in full (repay 100%) the monthly installments to avoid additional interest charges.

2. How long would you take to settle the debt in full? For Balance Transfer Plan that only requires you do make minimum 5% payment monthly, there’s no point doing a Balance Transfer for say 6 months to enjoy a lower interest rate and then come end of 6 months you have yet to settle the debt and will be charged 18% again. Generally, the faster you pay up your debt the less interest you will be charged.

Also note that there is a penalty clause for early settlement, which is usually about RM100. Therefore, make sure you keep track of when the Balance Transfer program expires and maintain a nominal amount until expiry date and then pay in full the next day.

3. What is the effective interest rate (annualized). Don’t be fooled by the so called interest rates advertised by the banks. For example, some banks may offer interest rate at 7% a year for 2 years Balance Transfer program but that 7% interest is charged up front per year (like hire purchase/car loan). Therefore, the effective interest rate when annualized is much higher.

4. Free gifts with Balance Transfer. Some financial institutions offer free gift when one does Balance Transfer and the cost of this so called free gift is included in the interest charges. It is better to go for lower interest charges instead of having material stuff which is most probably the main reason one is in debt in the first place.

5. Last but not least, are you willing to put your present credit card(s) in the drawer until you finish paying up your current debt? No point doing Balance Transfer and at the same time have new outstanding balance with your credit card(s) because you are just incurring more debt. The fact is that one does Balance Transfer because he/she is unable to pay his/her debts.

If you have considered the above and are determined to be debt free, then continue reading otherwise don’t waste your time.

FACTS YOU NEED TO KNOW ABOUT BALANCE TRANSFER PLANS

First and foremost, all Banks treat Balance Transfer as a cash advance; and the moment you fail to meet the terms and conditions, an interest rate of 18% shall be levied on the Balance Transfer Amount.

Secondly, once a specified amount of the Outstanding Balances to be transferred has been approved, a corresponding amount of the Cardmember’s existing credit card limit will be reserved for this purpose and shall not be available to the Cardholder.

Thirdly, most banks only allow the principal cardholder to perform a balance transfer.

Fourthly, always check if there is any penalty for early settlement. Most banks impose a penalty fee of RM100 if you settle the balance transfer program before the expiry date. Therefore, it is imperative that you know when is the exact expiry date of the balance transfer plan.

Fifth, some banks will also impose a service fee for making payment(s) to the credit card account.

And most importantly, will there be a new account created for the balance transfer plan. If NOT, beware, especially if the repayment is not based on equal installments. Please understand the terms and conditions especially on the payment hierarchy thingy (I have no idea how it works) so that you’ll not be imposed any interest for nothing. Even if the card issuer states 0% Balance Transfer (and no new account is created), you may be subjected to interest charges for your new transactions with your credit card. I think it is because of the standard clause that states that the Interest Free Period shall not be applicable should one have Outstanding Balance – and the approved Balance Transferred Amount IS an Outstanding Balance.

TYPES OF BALANCE TRANSFER PLANS

0% INTEREST BALANCE TRANSFER PLANS

The best Balance Transfer Plans are those offering 0% Interest Rate that have no Upfront Fee AND a new separate account is created. Always read the terms and conditions. There are also two distinct types of 0% Balance Transfer Plans:

First, I like Balance Transfer plans with new account(s) created where we are required to pay equal installments or only need to pay minimum 5% of the Balance Transfer Amount and no interest will be imposed. For this kind of 0% Balance Transfer Plan, all your new transactions will be separated from the Balance Transfer Account.

The second type of 0% Balance Transfer is where no new account will be created and the installment towards the BT is included along with your old and new transactions. Your repayment towards the Outstanding Balance may be based on the bank’s own payment hierarchy system which I really don’t understand how it works. Once, HSBC called me to offer me their 0% Balance Transfer Plan, so I asked about the payment hierarchy system and I cannot understand what he was trying to tell me and he ended up telling me I don’t have to worry as I always pay in full. Why the heck does he need to tell me not to worry? That got me worried. If you click here and read this post on Balance Transfer at My Credit Cards blog published years ago, Annuar commented/shared with us that he ended up paying RM300 to HSBC because of the payment hierarchy! Or maybe like I mentioned earlier, it is because they consider the Balance Transfer an Outstanding Balance and therefore the Interest Free Period no longer applies for transactions with the card.

So, for 0% Balance Transfer, if no new account will be created, please understand the terms and conditions and the bank’s payment hierarchy. My advise, in the case where no new account is created, it’s best for you not to have any Outstanding Balance before you do the BT and don’t use the card until the Balance Transfer amount is settled in full. This is to ensure your payment is purely towards the Balance Transfer debt. Therefore, you won’t get any headaches.

Currently (January 2016), card issuers offering 0% Interest Rate Balance Transfer Plans are AEON Credit Service and Public Bank.

AEON Credit Service 6 Months 0% Balance Transfer Plan

For AEON’s 6 Months 0% Balance Transfer Plan, the minimum amount to be transferred is only RM1K. You may perform Balance Transfer amounts up to 80% of your credit limit.

Repayment – 6 equal installments.

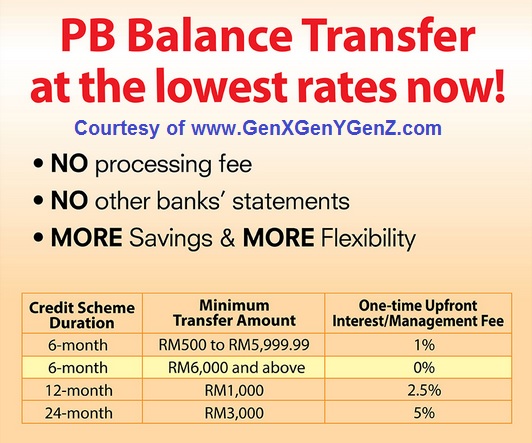

PUBLIC BANK 6 Months 0% Balance Transfer Plan

Public Bank is offering 6 Months 0% Balance Transfer Plans and you can apply for the 0% 6 Months Balance Transfer more than once up to 80% of your credit limit. Repayments are based on equal installments. And note, if you settle the balance transferred amount in full prior to expiry of the plan, you will be imposed RM100 penalty.

Click here to Public Bank Balance Transfer Plans Terms and Conditions.

PUBLIC BANK 12 Months 0% Balance Transfer Plan For New Cardholders

Thanks to hurtedheart of LYN who corrected me and pointed out the below 0% Balance Transfer Plan for those new to Public Bank. Not only do you get 0% BT but they pay you RM50 for signing up!!!

UPFRONT INTEREST BALANCE TRANSFER PLANS WITH FIXED INSTALLMENTS

Most banks have this kind of Balance Transfer Plans where you are imposed upfront interest upon approval and you are to repay it back based on equal installments. They will advertise with a “low” interest rate to attract you but in actual fact you may even end up paying more in interest compared to your credit card tiered interest rate on Outstanding Balance (i.e. the earlier you pay, the less the interest charges).

- AmBank 8.99% Upfront Interest with FREE Gifts. Effective Interest Rate 16.23%!!!

- Public Bank Upfront Interest 1% and 2.5% for 6 and 12 months respectively.

- RHB Upfront Interest 4% and 7% Upfront for 12 ans 24 months respectively. Effective Interest Rate 7.3% and 8.67%

- Maybank 3% Upfront Interest for 12 months Balance Transfer plan BUT Maybank advertise this as 0% Interest Free Balance Transfer Plan!!! Real Bull Shitting here.

- Credit Card Tutorial by http://www.GenX GenY GenZ.com

Well, from the above, Public Bank Balance Transfer Upfront Interest Rate looks like it is the “cheapest”; but, they will charge you RM100 penalty for early settlement.

Most of the balance transfer plans above have early settlement penalty. It does not really make sense why the banks would want to charge us early settlement penalty since they already have made their “profit” with the upfront fee and we do not save a single sen in interest. Only reason I can think of is they are trying to tie you up, the longer the better, and the probability of you not being able to settle the monthly Outstanding Balance in full gets better with time and the chances of you once again spending beyond you means also increases. And once this scenario happens, you will be charged an exorbitant interest rate of 18%.

The banks are aware that people who are in the shit hole are most likely to stay in the shit hole because it is very hard for one to change their habits or attitude when it comes to their lifestyle (i.e. spending money). Like I said in my article Introduction to Credit Cards CC 101 –

My principle is never to let the bank charge me a single sen of interest from my credit card usage. You should adopt this principle too, and never say just once, because if you break your principle once, what’s there to stop you from breaking it a second time.

And if you are a salaryman without any savings in the bank and you just manage to scrape through monthly, think twice before you swipe your card, you have no money today, what makes you think you’ll have money to pay back tomorrow?

When there is upfront interest, the effective interest will be much higher:

For example, the AmBank Balance Transfer 8.99% upfront interest, AmBank mentioned that it is equivalent to an effective interest rate of 16.38%!!! That is why they can offer you FREE gifts. For example, you do a 3 year BT with AmBank for RM20,000. The Upfront Interest will work out to be RM20,000 x 8.99% x 3 years = RM5,394 and you’ll get an Apple iPhone 6 which cost less than RM5K!

For RHB Bank, the upfront interest are 4% and 7% for 12 and 18 Months Balance Transfer Plans respectively. Based on previous RHB BT Plans, RHB Upfront Interest is calculated differently from AmBank. RHB’s upfront interest is a flat one time fee. For example, Transferred amount of RM1,000 with an interest charge of 9% for a 24 month installment plan; the monthly installment is computed as RM1,000 + (RM1,000 x 9%) / 24 months = RM45.4167 per month. The repayment quantum will be 24 equal monthly installments amount. There is no penalty fee if one were to settle the BT earlier.

As you can observe from above, every bank has a different method of calculating the Upfront Interest.

INTEREST REDUCING BALANCE TRANSFER PLAN

This kind of balance transfer plan imposes interest on the Outstanding Balance only. E.g. Hong Leong Bank Balance Transfer. The earlier you pay towards the Balance Transfer debt, the less you pay in interest. This kind of plan is good for those needing a short period of loan not more than 6 months. And you should always read the Terms and Conditions and confirm if a new account will be credited – or else you may end up paying interest on your new transactions. Also, some banks may impose a penalty fee if you settle the debt earlier.

Hong Leong Balance Transfer – 6.99% Interest Rate for 6 or 12 Months Balance Transfer Plan. The Cardholder shall be obligated to pay the minimum payment due in the BT Account or RM50.00, whichever is higher. If the Cardholder fails to make payment on or before the due date, the 6.99% p.a. interest rate will be retracted and interest at 18% p.a. will be charged on the amount outstanding in the BT Account on a daily basis until full repayment. HLB will impose an early settlement penalty of RM70. Therefore, you need to maintain a nominal amount up to the expiry date and then settle in full the following day (please go to my comments on HLB 0% Months BT Plan above). Please refer to HLB website for latest info on their BT Plans.

CONCLUSION

Once again, if you are using a Balance Transfer Plan to settle your debt (the credit card issuer calls this a Card Benefit or Promotion), then you are living beyond your means. If you really need to do a balance transfer, go for 0% interest rate plans (but the banks know that since you can’t pay up at the other bank, the probability of you paying them 18% interest and giving them fantastic profits after the expiry of the 0% period is very high).

And remember, beware of whatever Balance Transfer Plan that does not create a new separate account. Your new transactions with your credit cards may be subjected to interest charges. Also, if you fail to pay the minimum 5% as stated in your Monthly Statement or the fixed equal installment amount in full, you may end up paying 18% interest ( actually more if there is an Upfront Fee) on the Balance Transfer Amount which defeats the purpose of you doing a BT in the first place.

I would like to reiterate – TRY NOT TO USE THE CREDIT CARD FOR NEW RETAIL TRANSACTIONS WHICH YOU HAVE PERFORMED BALANCE TRANSFER WITH UNTIL YOU SETTLE IN FULL. ESPECIALLY IF NO NEW ACCOUNT IS CREATED FOR THE BT AND IT IS NOT BASED ON EQUAL INSTALLMENTS. And my advise to you is to avoid HSBC and Citibank Balance Transfer Program if you intend to use their credit card(s) for retail transactions prior to you settling in full the BT amount. This is because, many people have reported (in my previous blog(s) and LYN) that they were imposed interest charges on their new retail transactions.

0% Balance Transfer Plans are great for those who have cash in hand to settle their monthly Outstanding Balance. Instead of paying in full one’s Outstanding Balance monthly, he/she does a 0% Interest Balance Transfer and the money in hand can then be deposited into Malaysian Banks’ Fixed Deposit Promotions where we get higher than board rates to earn some pocket money.

However, in order to earn meaningful pocket money, the amount needs to be substantial like RM10K or more. If you’re thinking of doing Balance Transfer of RM2K to earn pocket money, you are simply wasting your time because the interest you earn per month will be less than RM10. You are just inviting unnecessary headaches as you need to keep track of the Balance Transfer.

An article by http://www.GenXGenYGenZ.com Please do not reproduce/reprint this article in whole or part in any form.

Remember, most BT Plans have a penalty if you settle in full early and if you pay a day later, you’ll be imposed interest of 18% on top of the Late Payment Penalty.

It is imperative that you remember that 0% Balance Transfer is NOT FREE money as you are just simply transferring your debt from one card issuer to another. And if you go and spend the cash in hand away and then cannot settle the payment due towards the 0% Balance Transfer Plan, you’ll end up paying 18% interest! This 0% Balance Transfer Plan is another trap laid out by the banks, not only that it entices you to spend and spend more, the possibility of you paying 18% to the bank is high with their complex terms and conditions.

I will repeat once again, if you do a Balance Transfer with even 0.01% interest, it means you are living beyond your means, keep your credit cards in the drawer until you are debt free and out of the shit hole before you actually use your credit card again. The moment you pay a single sen in interest to the bank because you overspent on stuff not required for your survival, it just simply means you are getting poorer and at the same time working to pay the bank and make them richer! It is worst then slavery, at least slaves get “free” makan in return for their work.

Last but not least, if you have discipline and are wise in controlling your spending, you won’t be in the shit hole of debt; thus, there is no need for you to do any Balance Transfer Plan or accidentally falling into the banks’ trap laid out in their complex terms and conditions.

Before you sign up for any installment plans, I suggest you read this article – 0% Interest Rate Installment Plans with Credit Cards Is A Trap.

Click here to my Credit Card Tutorial Page/Menu for more Credit Card Tutorials/Reviews

A Credit Card Tutorial by GenX

A Credit Card Tutorial by GenX