Credit Card Tutorial by GenX @ http://www.GenXGenYGenZ.com

Before you proceed with this tutorial, I suggest you read the following FREE tutorials for Credit Cards Beginners:

After you have read the above mentioned prerequisite course, then only proceed to take my FREE Credit Card Tutorial starting with Introduction To Credit Cards 2016 – CC101 (click here).

To learn more on how credit cards can make you poorer by the day, click here to read my tutorial Credit Card Fees & Interest Rate – CC114

INTRODUCTION

The main reason why we want a credit card is, it is more convenient than carrying cash around. But nowadays, debit cards serve the same purpose.

The argument that it is safer to have a credit card than carrying cash no longer holds true because there have been cases where the criminals will force their victims to release information regarding their cards’ pin numbers and then go withdraw cash with their cards and then murder them by cutting them into parts!!! Not only that, your cards and my cards are prone to fraud cases where it may be used for unauthorized transactions. Every single time we use our credit cards, we are taking a risk because another party now has our information i.e. our card numbers, our name on the card, the expiry date and also the CCV security number (some smart people cover the CCV number at the back of the card).

If you ask me, a debit card is much better than a credit card in terms of controlling the damage in the event of fraud cases. This is because we can actually control how much money can be spent with the debit card by depositing only the necessary amount of money into the account. What if your wallet was stolen with your credit cards in them. Well, if you immediately report your credit card was stolen, then you are only liable for up to RM250/card. However, if you only realized that your credit card was stolen after a day or so and the credit card was used for unauthorized transactions hitting your credit limit (not necessarily all credit cards will send out SMS alerting you on the transactions, or maybe your phone got stolen too), the card issuer may insist that you are liable for the unauthorized transactions because you were negligent and failed to report it was stolen!

If you have yet to read my article Credit Card Fraud and SMS Alert, please click here to read it for your own good. Nowadays, there is this thing called Caller ID Spoofing where one will receive phone calls showing actual genuine phone numbers (e.g. police station, bank’s customer service number, etc) and the person on the other end of the line will know your name and in some cases what credit card you have too! Never ever release your personal info to anyone over the phone.

The other set back of having a credit card over a debit card is that we may overspend like what I mentioned in my prelude to this series. We Malaysians like to go to the malls to enjoy free air-conditioned environment and studies have shown that those with credit cards tend to spend more. And with many merchants offering installment plans, it allows a credit card holder to buy non-essential stuff which otherwise they cannot afford. And if we charge our expenses to our credit card more than the cash we have to pay back in full when the time comes, then we end up being in the shit hole of debt.

And the worst scenario is when our wife/girlfriend goes on a spending rampage hitting our credit cards’ credit limit when they are pissed off big time with us!!! If you ever give your partner a Supp card and you know she/he ( yeah nowadays many toy boys around too) is mad with you, I guess it is good to be kiasu and call Customer Service to temporary suspend her/his Supp Cards, hahaha.

The above introduction is to point out some of the cons of having a credit card before I proceed to the benefits 🙂

BENEFITS OF CREDIT CARDS

Well, most credit card users are aware that they are rewarded with reward points for using their credit cards whereby they can use the points to redeem for stuff/cash vouchers. Nowadays, many credit cards offer cash back/rebate instead of points. So it makes sense to use credit card instead of paying with cash and get nothing in return.

However, let me inform you that merchants are imposed some fees by the card issuers ranging from 1% to 5% on the amount that we transact with our cards. Most merchants would have considered this fee when they price their products. However, some merchants (especially the ones with low turnover and thus not enjoying special lower price from the product manufacturers) may impose surcharge when we use our credit cards and some of us may argue that this is not appropriate. In my opinion, if the merchant was upfront and transparent in informing that the price of their product is for CASH ONLY, then it’s fair that they impose a surcharge fee because no one is forcing the cardholder at gun point to use his/her credit card. However, if the merchant fails to inform or put notice on this surcharge, then I will say that it is unfair to impose any surcharge on the agreed price (they offer by displaying the price tag and we accept).

REWARD POINTS TO REDEEM STUFF/CASH VOUCHER

In order to entice us to use credit cards, card issuers have been rewarding the card users for decades with reward points.

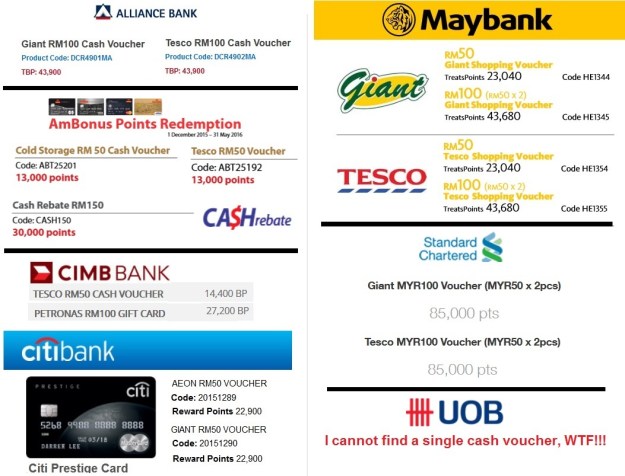

Here are some examples of points required for redemption of Giant or Tesco cash vouchers (as of 1 January 2016):

AmBank: 13,000 Points for RM50 Tesco Cash Voucher OR 30,000 Points for RM150 Cash Rebate.

Alliance Bank: 43,900 Timeless Bonus Points for RM100 Giant Cash Voucher.

CIMB Bank: 14,400 Bonus Points for RM50 Tesco Cash Voucher

Citibank for Prestige Visa: 22,900 Reward Points for RM50 Giant Cash Voucher.

Maybank: 43,680 Treats Points for RM100 Giant Cash Voucher

Standard Chartered Bank: 85,000 Points for RM100 Giant Cash Voucher

UOB Bank: No Cash Vouchers but all useless gifts which I do not need!!!

Based on the above, I will now teach you how to calculate the returns you will earn, in terms of Equivalent Cash back, when you redeem your Reward Points for Cash Vouchers:

Alliance Bank Visa Infinite – 2X and 5X Timeless Bonus Points which is equivalent to 0.45% and 1.14% cash back for local and overseas spending respectively.

For those who are blur as to how I came up with the equivalent cash back above for local spending, I will now show you a sample calculation:

In order to earn 43,900 Timeless Bonus Points from your local spending, you will need to spend RM21,950 with the Alliance Bank Visa Infinite.

Therefore the equivalent cash back =

RM100 Cash Voucher/RM21,950 spent x 100% = 0.45558%

AmBank WorldMasterCard (based on 30,000 Bonus Points = RM150 Cash Rebate) – 1X and 5X (non-online) AmBonus Points which is equivalent to 0.5% and 2.5% cash back for local and overseas spending respectively.

CIMB World MasterCard (based on 27,300 BP = RM100 Petronas) – 1X and 2X Bonus Points which is equivalent to 0.367% and 0.735% cash back for local and overseas spending respectively.

Citibank Prestige World MasterCard – 1X and 2X Reward Points which is equivalent to 0.21% and 0.44% for local and overseas spending respectively.

ENTRY LEVEL Maybank 2 Gold Cards Visa or MasterCard – 1X Treats Points for both local and overseas transactions, which is equivalent to 0.217%

ENTRY LEVEL Maybank 2 Gold Cards American Express – 5X Treats Points for both local and overseas transactions, which is equivalent to 1.08%

Maybank Visa Signature (based on 40,000TP = RM100 Cash Back) – 1X and 5X Treats Points which is equivalent to 0.25% and 1.25% for local and overseas spending respectively.

Maybank Visa Infinite – 2X and 5X Treats Points which is equivalent to 0.49% and 1.08% for local and overseas spending respectively.

Maybank 2 Cards Premier AMEX Reserve – 5X Treats Points for both local and overseas transactions, which is equivalent to 1.08%

Standard Chartered Bank Visa Infinite – 1X and 5X Reward Points which is equivalent to 0.11% and 0.58% for local and overseas spending respectively.

UOB Bank – WTF!!! I can’t seem to find any cash vouchers to redeem with my UNIRinggit for 2016!!! All I see are useless gifts!!!

From the above, you are shown the following:

- Premier Credit Cards DO NOT necessarily give you more in returns compared to a FREE FOR LIFE Entry Level Credit Card. From the above, you can see how useless the Citibank Prestige World MasterCard and Standard Chartered Bank Premier Banking Visa Infinite are compared to the Entry Level Maybank 2 Cards Gold AMEX.

- For local spending, except for the Maybank 2 Cards Gold/Platinum/Premier, all Visa and MasterCard credit cards will earn you 0.5% or less in returns!!!

- For overseas spending (including online), even with 5X Reward Points, you will only get about 1% cash back equivalent when redeeming for cash vouchers!!! However, the AmBank World MasterCard is pretty good if you travel overseas often as you can earn 2.5% cash back from your NON-online overseas transactions.

Click here to read my VergonDC’s review of the AmBank World MasterCard where he was my Guest Columnist at Generations XYZ Blogspot.

From the above, the returns we get nowadays from Reward Points credit cards are so damn pathetic and there is no point in getting them except for the following cards:

- Maybank 2 Cards Gold/Platinum/Premier American Express where we can earn 5X Treats Points from our local transactions. And before you say that AMEX is not useful, please click here and read my review of the Maybank 2 Gold/Platinum Cards where I listed essential expenses that can be paid with the American Express cards.

- Maybank Visa Signature (a hybrid card that earns you 5% cash back for Petrol and Groceries too)

- AmBank World MasterCard and Visa Infinite for overseas non-online transactions where you can earn 2.5% cash rebate.

Having said the above, there is one really good benefit of owning the right credit card that earns you reward points where you can convert them to Enrich Miles or Kris Flyer Miles or Asia Miles and redeem “FREE” air tickets. I will touch on this very soon.

You must be logged in to post a comment.