Credit Card Tutorial by GenX @ http://www.GenXGenYGenZ.com

Before you proceed with this tutorial, I suggest you read the following FREE tutorials for Credit Cards Beginners:

After you have read the above mentioned prerequisite course, then only proceed to take my FREE Credit Card Tutorial starting with Introduction To Credit Cards 2016 – CC101 (click here).

To learn more on how credit cards can make you poorer by the day, click here to read my tutorial Credit Card Fees & Interest Rate – CC114

INTRODUCTION

The main reason why we want a credit card is, it is more convenient than carrying cash around. But nowadays, debit cards serve the same purpose.

The argument that it is safer to have a credit card than carrying cash no longer holds true because there have been cases where the criminals will force their victims to release information regarding their cards’ pin numbers and then go withdraw cash with their cards and then murder them by cutting them into parts!!! Not only that, your cards and my cards are prone to fraud cases where it may be used for unauthorized transactions. Every single time we use our credit cards, we are taking a risk because another party now has our information i.e. our card numbers, our name on the card, the expiry date and also the CCV security number (some smart people cover the CCV number at the back of the card).

If you ask me, a debit card is much better than a credit card in terms of controlling the damage in the event of fraud cases. This is because we can actually control how much money can be spent with the debit card by depositing only the necessary amount of money into the account. What if your wallet was stolen with your credit cards in them. Well, if you immediately report your credit card was stolen, then you are only liable for up to RM250/card. However, if you only realized that your credit card was stolen after a day or so and the credit card was used for unauthorized transactions hitting your credit limit (not necessarily all credit cards will send out SMS alerting you on the transactions, or maybe your phone got stolen too), the card issuer may insist that you are liable for the unauthorized transactions because you were negligent and failed to report it was stolen!

If you have yet to read my article Credit Card Fraud and SMS Alert, please click here to read it for your own good. Nowadays, there is this thing called Caller ID Spoofing where one will receive phone calls showing actual genuine phone numbers (e.g. police station, bank’s customer service number, etc) and the person on the other end of the line will know your name and in some cases what credit card you have too! Never ever release your personal info to anyone over the phone.

The other set back of having a credit card over a debit card is that we may overspend like what I mentioned in my prelude to this series. We Malaysians like to go to the malls to enjoy free air-conditioned environment and studies have shown that those with credit cards tend to spend more. And with many merchants offering installment plans, it allows a credit card holder to buy non-essential stuff which otherwise they cannot afford. And if we charge our expenses to our credit card more than the cash we have to pay back in full when the time comes, then we end up being in the shit hole of debt.

And the worst scenario is when our wife/girlfriend goes on a spending rampage hitting our credit cards’ credit limit when they are pissed off big time with us!!! If you ever give your partner a Supp card and you know she/he ( yeah nowadays many toy boys around too) is mad with you, I guess it is good to be kiasu and call Customer Service to temporary suspend her/his Supp Cards, hahaha.

The above introduction is to point out some of the cons of having a credit card before I proceed to the benefits 🙂

BENEFITS OF CREDIT CARDS

Well, most credit card users are aware that they are rewarded with reward points for using their credit cards whereby they can use the points to redeem for stuff/cash vouchers. Nowadays, many credit cards offer cash back/rebate instead of points. So it makes sense to use credit card instead of paying with cash and get nothing in return.

However, let me inform you that merchants are imposed some fees by the card issuers ranging from 1% to 5% on the amount that we transact with our cards. Most merchants would have considered this fee when they price their products. However, some merchants (especially the ones with low turnover and thus not enjoying special lower price from the product manufacturers) may impose surcharge when we use our credit cards and some of us may argue that this is not appropriate. In my opinion, if the merchant was upfront and transparent in informing that the price of their product is for CASH ONLY, then it’s fair that they impose a surcharge fee because no one is forcing the cardholder at gun point to use his/her credit card. However, if the merchant fails to inform or put notice on this surcharge, then I will say that it is unfair to impose any surcharge on the agreed price (they offer by displaying the price tag and we accept).

REWARD POINTS TO REDEEM STUFF/CASH VOUCHER

In order to entice us to use credit cards, card issuers have been rewarding the card users for decades with reward points.

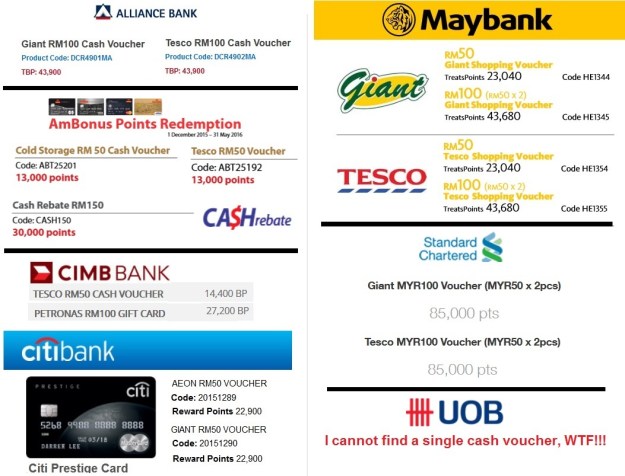

Here are some examples of points required for redemption of Giant or Tesco cash vouchers (as of 1 January 2016):

AmBank: 13,000 Points for RM50 Tesco Cash Voucher OR 30,000 Points for RM150 Cash Rebate.

Alliance Bank: 43,900 Timeless Bonus Points for RM100 Giant Cash Voucher.

CIMB Bank: 14,400 Bonus Points for RM50 Tesco Cash Voucher

Citibank for Prestige Visa: 22,900 Reward Points for RM50 Giant Cash Voucher.

Maybank: 43,680 Treats Points for RM100 Giant Cash Voucher

Standard Chartered Bank: 85,000 Points for RM100 Giant Cash Voucher

UOB Bank: No Cash Vouchers but all useless gifts which I do not need!!!

Based on the above, I will now teach you how to calculate the returns you will earn, in terms of Equivalent Cash back, when you redeem your Reward Points for Cash Vouchers:

Alliance Bank Visa Infinite – 2X and 5X Timeless Bonus Points which is equivalent to 0.45% and 1.14% cash back for local and overseas spending respectively.

For those who are blur as to how I came up with the equivalent cash back above for local spending, I will now show you a sample calculation:

In order to earn 43,900 Timeless Bonus Points from your local spending, you will need to spend RM21,950 with the Alliance Bank Visa Infinite.

Therefore the equivalent cash back =

RM100 Cash Voucher/RM21,950 spent x 100% = 0.45558%

AmBank WorldMasterCard (based on 30,000 Bonus Points = RM150 Cash Rebate) – 1X and 5X (non-online) AmBonus Points which is equivalent to 0.5% and 2.5% cash back for local and overseas spending respectively.

CIMB World MasterCard (based on 27,300 BP = RM100 Petronas) – 1X and 2X Bonus Points which is equivalent to 0.367% and 0.735% cash back for local and overseas spending respectively.

Citibank Prestige World MasterCard – 1X and 2X Reward Points which is equivalent to 0.21% and 0.44% for local and overseas spending respectively.

ENTRY LEVEL Maybank 2 Gold Cards Visa or MasterCard – 1X Treats Points for both local and overseas transactions, which is equivalent to 0.217%

ENTRY LEVEL Maybank 2 Gold Cards American Express – 5X Treats Points for both local and overseas transactions, which is equivalent to 1.08%

Maybank Visa Signature (based on 40,000TP = RM100 Cash Back) – 1X and 5X Treats Points which is equivalent to 0.25% and 1.25% for local and overseas spending respectively.

Maybank Visa Infinite – 2X and 5X Treats Points which is equivalent to 0.49% and 1.08% for local and overseas spending respectively.

Maybank 2 Cards Premier AMEX Reserve – 5X Treats Points for both local and overseas transactions, which is equivalent to 1.08%

Standard Chartered Bank Visa Infinite – 1X and 5X Reward Points which is equivalent to 0.11% and 0.58% for local and overseas spending respectively.

UOB Bank – WTF!!! I can’t seem to find any cash vouchers to redeem with my UNIRinggit for 2016!!! All I see are useless gifts!!!

From the above, you are shown the following:

- Premier Credit Cards DO NOT necessarily give you more in returns compared to a FREE FOR LIFE Entry Level Credit Card. From the above, you can see how useless the Citibank Prestige World MasterCard and Standard Chartered Bank Premier Banking Visa Infinite are compared to the Entry Level Maybank 2 Cards Gold AMEX.

- For local spending, except for the Maybank 2 Cards Gold/Platinum/Premier, all Visa and MasterCard credit cards will earn you 0.5% or less in returns!!!

- For overseas spending (including online), even with 5X Reward Points, you will only get about 1% cash back equivalent when redeeming for cash vouchers!!! However, the AmBank World MasterCard is pretty good if you travel overseas often as you can earn 2.5% cash back from your NON-online overseas transactions.

Click here to read my VergonDC’s review of the AmBank World MasterCard where he was my Guest Columnist at Generations XYZ Blogspot.

From the above, the returns we get nowadays from Reward Points credit cards are so damn pathetic and there is no point in getting them except for the following cards:

- Maybank 2 Cards Gold/Platinum/Premier American Express where we can earn 5X Treats Points from our local transactions. And before you say that AMEX is not useful, please click here and read my review of the Maybank 2 Gold/Platinum Cards where I listed essential expenses that can be paid with the American Express cards.

- Maybank Visa Signature (a hybrid card that earns you 5% cash back for Petrol and Groceries too)

- AmBank World MasterCard and Visa Infinite for overseas non-online transactions where you can earn 2.5% cash rebate.

Having said the above, there is one really good benefit of owning the right credit card that earns you reward points where you can convert them to Enrich Miles or Kris Flyer Miles or Asia Miles and redeem “FREE” air tickets. I will touch on this very soon.

CASH BACK CREDIT CARDS, REAL MONEY INTO YOUR POCKET

Nowadays, there are many credit cards offering cash back when we use them instead of rewarding us with points. Some of the cash back credit cards for general transactions that are worth considering are:

Hong Leong Bank Essential Credit Card (Annual Fee waived with 12 swipes) – UNLIMITED 0.6% Cash Back for Insurance. Other transactions except petrol – 0.6% cash back for first RM5K and UNLIMITED 1% cash back for spending above RM5,000.

OCBC Great Eastern MasterCard (FREE FOR LIFE no conditions whatsoever) – 1% cash back up to RM1K spending and UNLIMITED 0.5% cash back for spending above RM1K. This card was highlighted to me by Devil4life at LYN.

If you spend between RM1K to RM1667 per month, then check out AEON Watami Visa where you can earn 3% cash back.

For online transactions, check out CIMB Cash Rebate MasterCard (FREE FOR LIFE no conditions whatsoever) where you can earn 5% cash back but there is a monthly cap of RM30. Public Bank Visa Signature also gives you 6% cash back for online transactions and the annual fee is auto waived with just 12 swipes a year.

Our government for the last few years have been cutting the subsidy for petrol which directly caused inflation to sky rocket overnight and thus resulted in many of the Rakyat to suffer and be pissed off big time with the BN government. With our spending power reduced, many of us had to adjust our lifestyles and cut down on non-essential stuff but one major item that we have no control over is Petrol. Reason being because Malaysians are a pampered lot and not into car pooling or parents needing to drive their children to school personally because of the many missing children cases.

Most Visa and MasterCard credit cards do not reward their cardholders when they use it to pump petrol. But thank God, there are credit cards that earn us up to 10% cash back for Petrol and Groceries.

- Maybank Islamic MasterCard Ikhwan (FREE FOR LIFE no conditions whatsoever) – 5% cash back on Friday and Saturdays for Petrol and Groceries.

- Hong Leong Bank Wise Visa – Guaranteed 10% cash back (not considering Annual Fee for 2nd year onwards) for Petrol, Groceries and Telco Bills EVERYDAY if you can swipe minimum 10 times and each transaction no less than RM50.

- Maybank Visa Signature (Annual Fee waived with RM50K spending) – 5% cash back for Petrol and Groceries EVERYDAY.

- AffinBank BHPEtrol Touch n Fuel MasterCard – `0% cash back at BHPEtrol but limited to 3 transactions per months and capped at RM50.

The Citibank Cash Back Platinum credit card offers 5% cash back for Petrol; however, the monthly cash back cap is freaking low and there is no annual fee waiver mechanism. After you deduct the annual fee, basically you will earn nothing!

And if you think you are going to earn 8% cash back from your Petrol AND Groceries transactions only with the HSBC Amanah MPower Platinum -i, you have been fooled. Like I said, you should have read my Introduction To Credit Card CC 101 before reading this tutorial.

YOU MAY EARN 10% CASH BACK FOR YOUR UNIFI, ASTRO & TOUCH n GO TOO!

Once again, click here to read Hong Leong Bank WISE credit card review where I shared a post by a “Staff” of LYN by the nickname of fruitie which teaches everyone how to earn 10% cash back for their UNIFI biil, ASTRO bill and Touch n Go top up!

FLY BUSINESS CLASS FOR FREE

Most major commercial banks’ credit cards allow you to convert your reward points to Enrich Miles. And by holding the right credit card based on your spending pattern, you can fly Business Class for FREE sooner than you ever imagine.

I have previously in my Generations XYZ blog published a Comprehensive Tutorial on The Best Credit Cards To Earn Frequent Flyer Miles. This tutorial will show you which credit cards are the best for redeeming Enrich Miles/KrisFlyer Miles and you can get more than 10% Equivalent Cash Back (from both your LOCAL and overseas spending) when you convert your Maybank Treats Points earned with the Maybank 2 Cards Premier to Enrich Miles and redeem for Business Class ticket to London!

If you want to maximize the returns from your credit card transactions, the only method today is to convert them to Enrich Miles and redeem for FREE Business Class tickets where it’s like you will be getting more than 10% equivalent cash back. If you redeem for Economy Class ticket, you may end up earning less in equivalent cash back compared to redeeming cash vouchers! However, you must be holding the right credit card and I will show you which credit cards you should have and those you need to avoid.

Seriously, if you have a child studying in Australia where the Unis do not impose surcharge on tuition fees when using credit cards, you should get the Maybank 2 Cards Premier and you will earn yourself a FREE Return Business Class ticket KL/London every year!

And if you are looking for the best credit card to earn you AirAsia Big Points so that you can fly for FREE, click here to my article titled The Best Credit Cards To Earn AirAsia Big Points @ Generations XYZ.

And if you have or is considering getting the CIMB Enrich World MasterCard, I suggest you click here and read my review and I bet you will switch to the Maybank 2 Cards Premier after reading my review.

SAVE MONEY WITH DISCOUNT AT YOUR FAVORITE RESTAURANT/MERCHANT

Besides cash back and gifts from using our credit cards, we can also save lots of money at participating merchants offering discount with a certain credit card. And best of all, usually the discount starts at 10% and can go up to 50% and is not capped.

For example, CIMB credit cards offers 10% – 15% discount at Eraman Duty Free for liquor and cosmetics. Click here to read my article titled My Hong Kong & Macau Trip 2016 where I bought liquor and my wife her SK II using my CIMB World Master Card and saved more than RM150.

Maybank credit cards are entitled up to 20% discount at Tai Thong group restaurants.

So if you pay with cash at the above 2 mentioned places, you won’t get any discount unless you hold their member card. The Eraman Privilege Member Card gets you 10% discount for liquor and cigarettes too!

So the point is, if you do frequent a particular restaurant or merchant very very often, do ask them if any credit card is entitled to a discount. If yes, go apply for that card. Alternatively, if you are freaking free, go to every bank website and check what credit card offers discounts at the merchants you patronize.

FREE FOOD AND DRINKS AT AIRPORT LOUNGES WORLDWIDE

There are many credit cards that grants the cardholder access to airport lounges for FREE. What is so great about airport lounges you may ask. Well you get FREE food, FREE Coffee, FREE soft drinks, FREE ice cream, FREE beer, FREE liquor, FREE shower and a nice comfy chair to sleep on for FREE. The magic word here is FREE.

Basically, it can be categorized into 4 categories.

1. KLIA Plaza Premium Lounge. Many Platinum credit cards grants the cardholder free access to KLIA Plaza Premium Lounge.

2. KLIA 2 Plaza Premium Lounge. Unlike KLIA where many credit cards do allow free access to the PPL, for KLIA 2 there are less.

3. Worldwide Airport Lounge. A few Premier credit cards do issue the Priority Pass Membership Card that gives the card holder access to 600 airport lounges worldwide for FREE.

4. Green Market at KLIA 2. Only a very few selected credit cards grant you a FREE meal and drink at this place. Priority Pass Membership Cards are not welcome here!

Click here to my Airport Lounge Page to learn more about credit cards that offer you FREE access to airport lounges.

CREDIT CARDS FOR MOVIE TICKETS

If you go to the movies often, there are several credit cards that can benefit you.

Citibank Clear Card (you will be imposed annual fees) entitles you to Free 1 for 1 Movie Ticket every Friday at TGV and GSC.

Hong Leong Bank GSC Credit Card (Annual Fee waived with 12 swipes) – Up to 10% discount at GSC EVERYDAY.

MACH by Hong Leong Bank (Annual Fee waived with 12 swipes) – 10% cash back for all cinemas. If you are into movies, make sure you sign up for Social Package if you are getting this card.

CASH BACK PROMOTIONS

It is common these days for card issuers to offer cash back promotions with our transactions. However, you must always read the terms and conditions for cash back promos because most of the time a certain amount is allocated and is based on first come first serve basis.

HSBC credit cards always have cash back promos back to back and usually the winners are based on first come first serve basis. For example, HSBC would allocate a certain sum every week during the promotion campaign period by offering 20% cash back for shopping at Mid Valley. They may define ‘week’ as commencing every Monday and ending on Sunday. So your chances of winning the cash back is very good if you swipe on a Monday instead of Saturday where the allocation would have been used up.

Once again, you must always read the Terms and Conditions to understand how you can be eligible for cash back promotions before you blindly go swipe your card and assume you’ll be getting the cash back advertised. For HSBC promotions, you usually need to register via SMS.

CONTESTS

There is always some contest going on for credit cards. Many card issuers which do not offer cash back as a card feature would run some contest in order to gain back some transactions lost to cash back cards. Some credit card issuers even offer car(s) as the grand prize. So if you fancy contests, then this is great as you may end up with a BMW or even a Porsche 🙂

However, I know that the odds of me wining the grand prize of a BMW or a Porsche is very slim. In my case, I will not bet/gamble on winning any Grand Prize with a credit card that earns me miserable returns unless that card gives me discount when I use it. Nowadays, I only use my fabulous Maybank 2 Cards Premier that guarantees me 1 Enrich Miles for every Ringgit spent locally or overseas.

For example, say UOB is running a contest where the grand prize is a BMW and for every RM1K spent, one is eligible for 1 entry. And one may have either the UOB Preferred Platinum MasterCard or UOB PRVI Miles or UOB Visa Infinite. And he/she is going to purchase a RM40K Rolex watch, which means he/she would be entitled to 40 entries and thus increasing the his odds of winning the grand prize.

I have shown you earlier, I can’t even redeem a single cash voucher using UOB UNIRinggit. And by using a UOB credit card which only earns the cardholder 1X UNIRinggit to purchase a RM40K Rolex watch, one only earns 40,000 UNIRinggit. If you think 40,000 UNIRInggit is a lot, you are mistaken. With 40K UOB UNIRinggit, one is lucky if he/she can redeem a stuff that cost more than RM50. However if one of the 40 entries wins the cardholder the grand prize, i.e. a BMW, I guess God must be rewarding him/her for the good deeds he/she has done, hahaha.

On the other hand, by using the Maybank 2 Cards Premier to purchase the RM40K Rolex watch at the “right” Rolex Authorized Dealer, one is guaranteed to earn 40K Enrich Miles which enables one to go upgrade an Economy Class ticket KL/London to Business Class one way for FREE!!! 100% you will win! Hahaha.

AIR TICKET DISCOUNT

Before you fly anywhere, click here to Corporate Information Travel Sdn Bhd website and check out Visa credit card offers and you will thank me for saving you more than pocket money.

0% INSTALLMENT PLANS

Many merchants offer 0% installment plans for retail purchases. Most of the electrical outlets like Courts, AEON Big, Harvey Norman, and computer brands like Acer, HP and Dell offer up to 12 months 0% Interest Installment Plans.

You can even buy a Rolex watch with 12 months 0% installment plans at Swiss Watch Gallery and Hourglass. But if you ask me, I think it’s better to go to Hourglass and use our Maybank 2 Cards Gold or Platinum or Premier AMEX and earn ourselves 5X Treats Points. Then go deposit the money allocated to pay for the Rolex watch into FD and earn some pocket money, haha.

On the other hand, Installment Plans with credit cards may not necessarily be a benefit and may even give you headaches. Click here to read my article 0% Interest Rate Installment with Credit Card Is A Trap.

BALANCE TRANSFER/UNSECURED LOAN

Besides Reward Points and Cash Back from our credit cards transactions, 0% Balance Transfer Plans can actually be considered as a “real” benefit based on the following reasons:

1. You can convert your ESSENTIAL and/or emergency transactions to 0% Installment Plans. Unlike Ezy Pay 0% Installments Plans which are designed to entice you to spend on non-essential stuff.

2. If you have the cash in hand to pay for your transactions, you can utilize 0% Balance Transfer Plans to earn extra FREE pocket money.

3. For those in the shit hole of debt, using the right Balance Transfer Plan can save you from interest charges.

However, let me warn you, no two Balance Transfer Plans are the same. Different banks have different terms and conditions for their balance transfer plans and also the time which they take to approve your Balance Transfer Application. Some banks will advertise that they are offering 0% Balance Transfer BUT once you sign up for this plan, your new transactions may be imposed interest even though you settle in full every month. Make sure you UNDERSTAND the terms and conditions of a particular balance transfer plan before you sign up for one.

To learn more on Balance Transfer Plans, please click on the link below to read my article.

Credit Card Balance Transfer Plan 2016. In this tutorial, I will teach you how to earn pocket money from Balance Transfer Plans in the Introduction itself. The example is also applicable as to how you can earn pocket money when you opt for 0% Installment Plans.

Also please note, 0% Interest Free Balance Transfer IS NOT FREE MONEY because it is still a debt and needs to be paid back. By doing Balance Transfer, all one does is transferring his/her debt from one bank to another to save on interest charges.

If you need unsecured Personal Loan for a short term period lke 3 to 6 months, Hong Leong Balance Transfer Plan offers interest rate at around BLR and is kind of unique in a way. Instead of paying to another credit card Outstanding Balance with another bank, in HLB BT Plan, they will deposit the money into your savings or current account (with any bank). However, I wish to emphasize here that this HLB Balance Transfer Program IS NOT A BENEFIT but I thought I might highlight to you guys this facility if you ever need it.

And if you are a Petronas Scholar and are thinking of breaking your bond with them, click here and read Mr-Stingy’s article titled How I Paid Off My RM58K Education Loan where he used credit cards to convert his “education loan” to 0% interest installments.

FREE GREEN FEES AT SELECTED GOLF COURSES

Most Premier and some Platinum credit cards offer complimentary green fees at selected golf clubs in Malaysia and even for overseas.

But to me I think this feature is useless as most of the time the loser will pay for the golf green fees, buggy fees and makan, hahaha. So, if you have been consistently losing and paying for your golf “kaki” meals, better you switch to another hobby and save lots of money. Just kidding.

Below are FREE credit cards that entitle you to a single complimentary green fee at selected golf courses.

AmBank World MasterCard – FREE FOR LIFE no condition whatsoever.

CIMB World MasterCard- FREE FOR LIFE no conditions whatsoever.

Maybank Visa Infinite- Annual Fee waived with RM50K spending.

Maybank 2 Cards Premier (AMEX Reserve & Visa Infinite) – Annual Fee waived with RM80K spending.

OTHER PROMOTION AND BENEFITS

Most credit cards offer some kind of limited time promotions and some exclusive card features.

Citibank PremierMiles offers you a free taxi ride home from KLIA.

Nowadays many Premier credit cards are also introducing FREE Valet parking at selected places but there is a monthly quota based on first come first serve basis.

Travel Insurance – most Gold and Platinum credit cards no longer offer this benefit.

Overseas Medical Insurance – Alliance Bank Visa Infinite and Standard Chartered Bank Visa Infinite. Please go read the terms and conditions. In my case, I would buy a third party Comprehensive Travel Insurance for my overseas trip which includes Medical, P.A., damage to luggage, etc. And third party Travel Insurance is really cheap plus easy to claim.

CONCLUSION

In order for you to determine which card is best for you, you need to breakdown your expenses to see which card offers you the most returns AND if the card offers discounts at your favorite merchants/restaurants. However, what you will most probably conclude is that a particular credit card that offers good discount at your favorite merchants generally do not offer you good reward points or cash back. For example, the Hong Leong Bank GSC credit card is great for movies but you earn nothing with it for pumping petrol.

Like I mentioned earlier, we get reward points and cash back by using our credit cards. However, no two cards are alike even from the same card issuer; as such we may need several cards to optimize the returns we can get from our credit card transactions.

Once again, I would like to reiterate that Credit Card is like money, it is a tool. Use it wisely and you shall benefit from it. On the other hand, if you do not have discipline to control your spending or withdrawing cash as if it is an ATM card, then credit cards can assist you in going down faster and deeper into the shit hole of debt.

I hope my series of articles on Credit Card for Beginners have benefited you in some ways and gave you an insight on credit card’s pros and cons. Thank you for reading my articles and visiting my blog(s).

Click here to my Credit Card Tutorial Page/Menu for more Tutorials and Credit Cards Reviews

Click here to read my article My Hong Kong & Macau Trip 2016 to see how I benefited from using different credit cards.

Click here to my Credit Card Promotion Page to see some of the benefits from CIMB, Citibank, Hong Leong Bank, Maybank, Public Bank, RHB Bank and UOB credit cards.

Click here to my BEST Credit Card Page to see more recommended cards by yours truly based on your income.

A Credit Card Tutorial by GenX

A Credit Card Tutorial by GenX