Another Personal Finance tutorial by GenX @ http://www.GenXGenYGenZ.com

UPDATE Sep 2022

Effective 1st October 2022, the Public Bank Quantum MasterCard is as good as useless!

UPDATE August 2022

Effective 1st September 2022, Malaysia Credit Cards Treats Points redemption for Air Miles will be inflated!

This is FREE Personal Finance Express Tuition for all credit card users, not necessary for newbies only but for Malaysians (contents applicable for worldwide too except for benefits that comes with cards issued by Malaysian banks).

Before I proceed, the first major set back for credit card fans in 2020 is that effective 1st August 2020, the cash back rate for the Maybank FC Barcelona Visa Signature will be downgraded to just 1%. No more 10% cash back in May or August! Below is the announcement at Maybank’s website:

Update 2022 – click here to read revisions to Public Bank Visa Signature and Quantum MasterCard effective 16th February 2022

LESSON NO.1 – What credit card to choose?

1. Get FREE FOR LIFE credit card without any condition.

I’m sure many of you have been approached by representatives of banks enticing you to sign up for a Free Annual Fee credit card only to find out later that you have been misled when you are later imposed annual fee for the second year because (1) you failed to swipe a minimum of 1 time per month or (2) you failed to swipe 6 or 12 times a year or (3) you failed to spend X amount per year.

Therefore, to avoid being charged unnecessary credit card annual fees (or the need for you to beg for annual fee waiver), it is IMPERATIVE that you sign up for a credit card that is truly FREE FOR LIFE WITHOUT ANY CONDITIONS.

The major advantage of FREE FOR LIFE without any condition is that you won’t be penalized a sen in the event you don’t even use your credit card in a particular year. It is great for those who may be assigned overseas for a few years and/or near retirement (once you retire or laid off, it is very hard to get a credit card if you do not have a steady source of income).

2. In order to maximize the returns from credit cards’ transactions, you must have an American Express Card because it is welcomed everywhere.

Before you go blindly accuse that the American Express Card is useless, let me teach you a thing or two:

The American Express cards are welcome at the following places:

- Departmental Stores & Hypermarkets: AEON, Isetan, Jaya Grocer, Metro Jaya, Mydin, Parkson and Robinson.

- Electronics, Electrical & Computers: AEON, Best Denki, Courts, EpiCentre (Apple iPhones & Macs), Harvey Norman, etc.

- Touch N Go Card – At PLUS Highway Service Centres and Jaya Grocer.

- Pharmacies – Caring, Guardian and Watson.

- Petrol – Petron, Petronas & Shell. Other stations you may need to pay at counter.

- Hospitals – Pantai, SDMC, Sunway, etc.

- Luxury Goods – Channel, Coach, Dior, Gucci, Hermes, LV, MK, etc.

- ROLEX! If your Authorized Rolex Retailer is giving you less discount for paying with AMEX, you are buying your Rolex watch with the wrong retailer, hahaha.

- Jewelers – Habib, Poh Kong, Tomei, Wah Chan, etc.

- Restaurants – Amarin, Alexis, Ippudo, Oriental Group of Restaurants, Tai Thong Group of Restaurants, Pizza Hut, even at McD and KFC!!!

- Hotels – including online hotel bookings with third party, e.g. Agoda, Hotels Dotcom, AirAsia Go, Expedia, etc.

- Airline Tickets – AirAsia, Malaysia Airlines, Singapore Airlines, etc.

- Insurance 1X TP only with the AMEX Reserve or Visa Infinite.

- Telcos and Astro – Astro, Celcom, Maxis, DiGi, Telekom, Unifi, etc

- Cars – BMW, MB, Volvo, etc.

- Books – MPH, Borders. etc.

- Others – 11 Street, Book Depository, Eraman Duty Free and etc.

And below is a fabulous tip shared at my Facebook back in 2018 by En. Ibrahim Rabani on how to earn 5X Treats Points or 5% Cash Back from restaurants/shops that does not accept AMEX.

Now let me show you some of my transactions with my AMEX Reserve where I earn 1 FREE Enrich or KrisFlyers or Asia Miles for every RM1 spent locally:

Touch N Go top up with AMEX at PLUS Service Centres

Duty Free Liquor and Cigarettes with AMEX at Eraman

I have the Eraman Privilege Card that grants me 10% discount for liquor and of course I used my AMEX to pay 🙂 Next time you are at Eraman, sign up for their Privilege Card but it will take months for them to sent it to you.

Cigarettes bought locally also I can earn Cash Back or Airmiles with my AMEX, hahaha

Petrol also I can earn Free Enrich Miles (or KrisFlyer Miles with the AMEX Reserve or 5% Cash Back on weekends with Maybank 2 Gold/Platinum Cards). With the Petron Card, I also earn 1.5% cash back. Many credit cards do not earn you anything from Petrol but not the Maybank AMEX where you can earn both Treats Points and Cash Back..

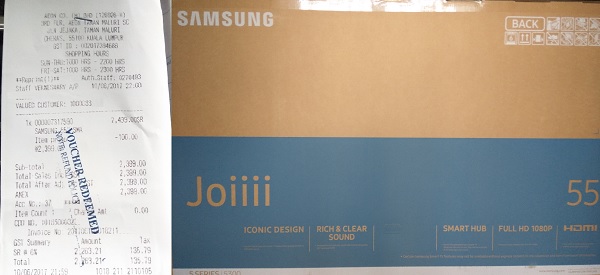

AMEX for LED TV plus RM120 Cash Vouchers from AEON – Earned myself 2K+ Enrich Miles 🙂 The reason why I bought the TV at AEON was I wanted it to be delivered on time for Father’s Day as a gift for my dad. You could probably get a better spec tv for the same price at 11St.

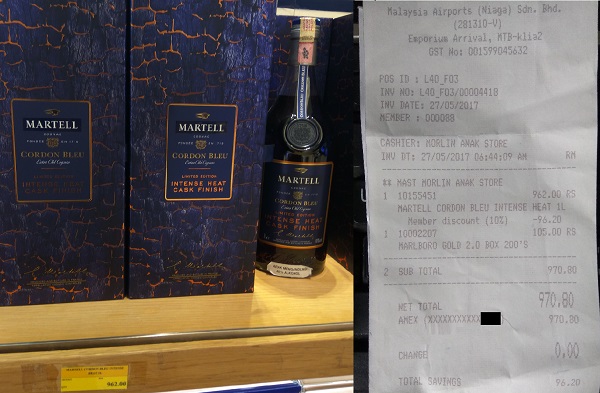

Whiskies, Cognacs or Wines from AEON, AEON Big, Jaya Grocer and Isetan with AMEX for more FREE Air Miles

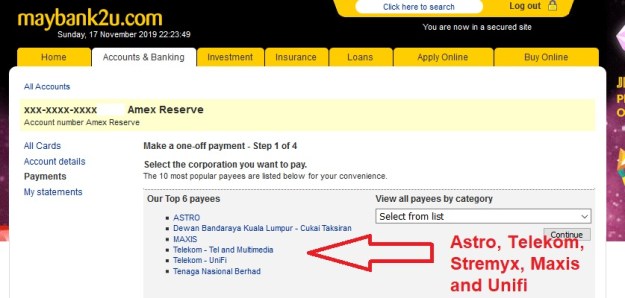

You can use AMEX at M2U to pay for UNIFI

Update Aug 2022 on Bill Payment Via M2U

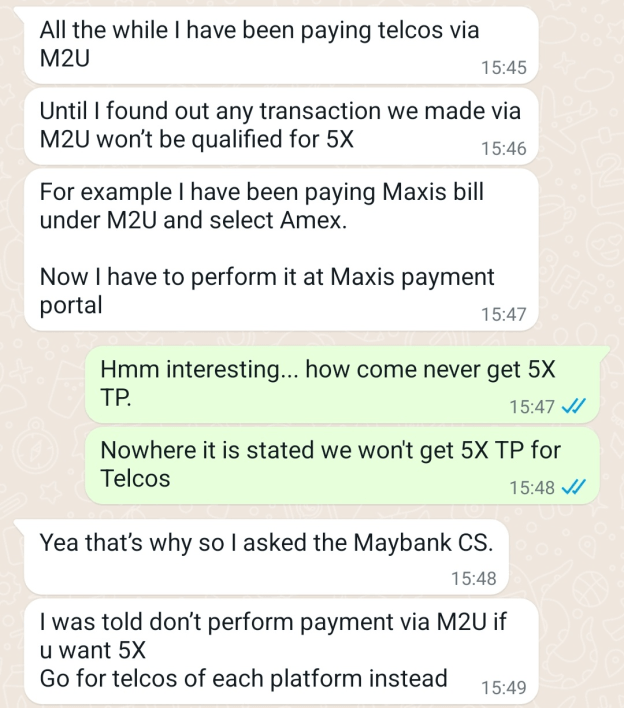

For years I have been telling my followers that Astro, Celcom, DiGi, Maxis, UMobile, Telekom and Unifi are not considered Utilties. And I have shared many times that you can even use your AMEX via M2U to pay these said bills.

HOWEVER, I got bad news, in August 2022, a follower shared with me that Maybank NO LONGER reward us with Treats Points when we make bill payments via M2U!!!

In respect to the above, you have been warned not to use M2U to pay your bills as you won’t be earning Treats Points.

On the other hand, another Bro who was informed of the above new development in August 2022, told me that he still earned 5% cash back with his Maybank 2 Cards Platinum AMEX when he paid his Maxis Bill via Maybank App in July 2022.

Therefore, please keep track to see if you are earning Treats Points or Cash Back if you are paying any bills via M2U or Maybank App.

Update 20th August – in respect to the above, 2 Bros informed me that they still earned Treats Points for they payments via M2U.

3. What FREE FOR LIFE without any conditions credit card to get in 2020?

Many of us Malaysians are really lucky because we are eligible for FREE FOR LIFE credit cards that actually give us back FREE Money when we use them for our essential expenses.

I will now promote for FREE to you 2 fantastic combo credit cards. And why are these cards so fantastic?

1. If you are earning less than RM36K per year. In accordance to Bank Negara Malaysia guidelines, you are only allowed to hold credit cards from 2 card issuers. Therefore by holding the cards I am about to recommend, you are ensured 5% Cash Back for almost all types of transactions.

2. These cards are FREE FOR LIFE without any conditions – YOU DON’T NEED TO SPEND A SEN WITH IT but yet your annual fees will be waived forever. These cards are especially good for young graduates and soon to be retirees.

3. If you and your spouse sign up separately as Principal cardholder, you get double the max monthly cash back.

The credit cards I would recommend are:

(I) Maybank 2 Gold Cards – MasterCard or Visa plus American Express.

a) The Visa or MasterCard that comes with this combo is nothing great and you can actually keep it in your drawer (don’t even activate it if you don’t need it).

b) The STAR of this combo is the American Express credit card where you can earn 5% cash back (maximum cash back RM50/month) for any type of transactions on Saturdays and Sundays except for transactions related to eWallets, Utilities and Government Agencies. Effective 1st June 2019, no Treats Points will be earned on weekends.

What the above means is that you can earn up to RM600/year in cash back with the Maybank 2 Gold/Platinum Cards AMEX from your essential expenses, i.e. Petrol, Groceries, Makan (e.g. Alexis, Ippudo, Absolute Thai, Pizza Hut, Starbucks, Sushi Zanmai, Oriental Group of Restaurants, and even McD), electrical equipment & electronic gadgets (Harvey Norman, EpiCentre, Courts, AEON, Best Denki, All IT, etc), major online shopping sites (e.g. 11St and Book Depository), Plus Highway Centres (to top up Touch N Go), Telcos (Celcom, DiGi and Maxis), Unifi and even to purchase underwear at AEON or other department stores.

c) On weekdays (Monday to Friday), the Maybank 2 Gold/Platinum Cards AMEX with 5X Treats Points is also excellent for collecting Airmiles.

d) Maybank is the only bank in Malaysia that provides TOLL FREE Customer Service for their Entry Level Gold credit cards. And I can tell you, Maybank Credit Card customer service is second to none where your calls will be answered by a human being within minutes.

(II) Public Bank Quantum MasterCard and Visa.

a) Apply for both the Public Bank Visa and MasterCard Quantum credit cards because each card has different benefits.

b) The Quantum Visa earns you 5% cash back for Contactless transactions except for petrol. This is very good as nowadays we can use contactless PayWave at most merchants.

c) The Quantum MasterCard earns you 5% cash back for Online. Great for Shopee and Lazada.

d) However, I have to point out that Public Bank Customer Service for their entry level credit cards may disappoint you if you have been spoiled by the excellent customer service provided by Maybank.

Once again, if you are new to credit cards, I would recommend that you apply for the Maybank 2 Gold Cards (Gold or Platinum) and Public Bank Quantum cards. By combining the cash back, you are entitled to up to RM110 per month FREE Money. And if both you and your spouse sign up for Principal cards, the cash back per month doubles to RM220.

LESSON No.2 – What is the first thing you must do once you get a credit card and what you need to remember throughout your lifetime.

In the previous lesson, I have recommended that you apply for the FREE FOR LIFE Maybank 2 Cards (MasterCard or Visa PLUS Amex) Combo and Public Bank Quantum (MasterCard and Visa) to earn cash back from your essential expenses.

1. So what is the first thing you should do once you activated your new credit cards?

The answer is you must reset the SMS Alert Default Value to RM1.00.

For the Maybank 2 Cards, it is very easy, just call the Toll Free Number behind the American Express Card to speak to the friendly and helpful Customer Service representative and simply request that SMS Alert for all your Maybank credit cards be set to RM1. It’s that simple.

However, if you have signed up with Maybank APP and agreed to Secure2U, you won’t get SMS!!! WTF! Instead you will get notifications at your smartphone. So make sure you allow notification for the Maybank APP!!! I tell you, this stupid decision by Maybank not to sent out SMS notification if we have signup for Secure2U is really bad as we won’t be able to get any notification of unauthorized usages of our MBB credit cards if we do not have data!!!

For Public Bank Quantum, once again call the number behind your card and request that the SMS Alert be set to RM1.00. Now, I do not own any Public Bank credit cards, so I have no idea what is the minimum SMS Alert Value that they are willing to accommodate. In the event that they refuse to set the minimum value of your SMS Alert to RM1, you can email Bank Negara Malaysia and complain. So remember to take down the name of the person whom you spoke to and the date and in the meantime request that the SMS Alert be set to the minimum value allowed.

2. Why is setting the SMS Alert Default Value to RM1 important?

Credit card fraud is very rampant. It is made even easier with the internet where anyone can just use the 16 digit numbers of your credit card to make transactions worldwide. I myself have experienced several times where my credit card numbers have been used for unauthorized online transactions. And the amounts weren’t huge, less than USD50/transaction. But with SMS Alert set at RM1, I was alerted of the fraudulent transactions and immediately contacted my card issuer and they then suspended my account to avoid any further damage.

Nowadays, more and more card issuers are issuing cards with payWave or PayPass where we simply touch the card on a terminal and any transaction below RM250 will automatically be approved!!! Cards having these feature are easily cloned (go google RFID card reader/fraud). Imagine someone having cloned your card, then goes tap here and tap there and tap everywhere at Mid Valley, where each transaction is less than RM250, within 10 minutes, the damage to your account can easily hit RM2K!!!

And if you do receive an SMS Alert for a transaction you did not make, call the number behind your card immediately (not 1 hour later or the next day) so that your card can be suspended. Failure to report any unauthorized transaction immediately may result in your card issuer insisting that you are liable for the transactions.

With the above, I hope I have emphasized the need for you to have the SMS Alert with default value set to RM1. If you do not practice what I mentioned above, you may regret big time when you receive your credit card statement with several thousand Ringgit worth of unauthorized transactions and end up with a major headache.

3. What you need to remember through out your lifetime when owning a credit card.

a) Always pay the Statement Balance in FULL prior to the Due Date. If you only make partial payment, then you have entered the shit hole of debt. So NEVER EVER use your credit card if you do not have cash in hand to settle the credit card bill in full.

Since most credit card issuers only sent the monthly Statements by email, I thought I share with you a sample of what I meant by paying the Statement Balance before the Due Date:

b) Never disclose your personal details (i.e. card number, expiry date, CCV and birthday) to anyone who calls you over the phone or emails or even a third party claiming to be a representative of a bank on the internet (including people who comment at my Facebook account or in Forums).

c) If you receive a call or SMS or even WhatsApp from a Mobile Phone claiming to be from the bank – most likely it is a scam. If you are interested in a product offered by your credit card, all you have to do is call the number behind your card and speak to the Customer Service and they will be more than happy to assist you.

Both my wife and I even received a FAKE SMS Alerts on a so called transaction which we did not make and in the SMS it even had a number for us to call! Once again, the only number to call is the number behind your card and no other number and use the Dialer instead of clicking on “links” in the SMS. Below is the image of the fake SMS I received.

d) If you receive a call from a Landline claiming to be from the bank or even Bank Negara Malaysia or even the Police in respect to a matter relating to your credit card, NEVER DISCLOSE your personal details. What you should do is once again call the number behind your card to verify or seek further clarifications.

e) Never click on any email links if you are asked to do so. If you need to log on to your online account, always open a new window and clear history/cookies before you sign into your Online Account. If you have any doubt or like more info on what’s stated in the email, go to the bank’s website by opening a new window or just call Customer Service (the number behind your card).

f) I tell you, scammers are getting more and more creative. In June 2017, I received a call on my mobile phone and when I answered it, it automatically went to voice message telling me that a transaction was performed with my credit card and if I did not do it, to press 1 (for something), 2 (for something else) and 3 (for something else). I knew it was a fake call and hung up. IF I had indeed used my credit card, surely I would have received a SMS.

Once again, always be kiasu and seek verification on any phone calls, SMS and emails by simply KEYING IN MANUALLY THE NUMBER BEHIND YOUR CARD INTO YOUR DIALER/KEYPAD to contact Customer Service and NEVER EVER “PRESS” ANY NUMBER SHOWN IN THE SMS TO AUTO CONNECT as it may be a link that directs you directly to the scammer.

LESSON No.3 – How to avoid falling into the shit hole of debt.

(1) If you can’t even save 10% of your monthly income every month, DO NOT GET a CREDIT CARD because YOU ARE GUARANTEED TO SPEND MORE chasing after “shiok sendiri” sensations. You may argue that I have been promoting credit cards to earn cash back from our Essential Expenses. Yes, that is true but it is also a fact that credit card is a very dangerous tool that can lead you straight into the shit hole of debt if you have no cash in hand to pay for the purchases.

(2) The most important thing about owning a credit card is that YOU MUST PAY THE STATEMENT BALANCE IN FULL PRIOR TO THE DUE DATE so that you are not imposed freaking high interest rate and not be a slave working for the bank for free. Never ever break this “rule”, because the moment you only pay the minimum or partial amount, you have entered the shit hole of debt. If you don’t have money today, and you keep swiping your credit card, what makes you think that you will have money in the future to pay your debt?

(3) So how to ensure that you are able to make full settlement of the Statement Balance before the Due Date?

A) Before you use your credit card to make a particular transaction, ask yourself if you have the equivalent amount of cash in your savings account (after deducting the amount required for your essential expenses and commitments) to pay for it:

If the answer is YES, then you should be able to pay your credit card Statement Balance in FULL prior to Due Date.

If the answer is NO and you still go and transact with your credit card, you are then spending beyond your means.

Most people with a little common sense will comprehend the above and would not stupidly go swipe their credit card and end up in the shit hole of debt.

B) So in order to entice people with common sense to spend beyond their means, the banks will lay cleverly disguised trap(s) to fool them. The banks in Malaysia are so freaking generous whereby they will offer you 0% interest rate loans to purchase unnecessary and non-durable stuff. And many will think that it’s a fabulous credit card feature where they can get FREE money, not understanding that 0% loan is also a debt.

(i) For those who have money in their savings account to pay in full for an item and then utilize the 0% installment plan, it may (not necessary, read paragraph below) be a smart move as we can earn extra money by depositing the money in an interest bearing account and pay for the purchase over time. Click here to learn more about Fixed Deposit to earn you more pocket money.

Having said the above, many people who have been constantly saving X% of their monthly salary or have money in their savings account to pay in full but opted to utilize the 0% Installment Plan would eventually regret that they did so. After experiencing and “tasting” what it’s like to be in “debt” for months, many would rather swipe/pay in full. This 0% installment plan may result in giving you the false impression that you have more money than you think (because you failed to deduct the balance debt which have yet to be paid) and thus you go swipe your credit card for other non-durable stuff and end up spending more which directly results in your savings shrinking further.

(ii) For those of you who do not have the equivalent amount of the total purchase price of an item in your savings account and opt for 0% installment plan, it means you are spending beyond your means. For example, you have RM1K in your savings account and you purchase an iPhone or Samsung Smartphone costing RM3K with 0% installment plan, it means you have spent beyond your means. Not only have you entered the shit hole, but in no time you’ll be drowning in it!!! Like I mentioned at the start of this post, a credit card is guaranteed to make you spend more. If you are in this situation and you keep swiping your credit card for non essential expenses or if an emergency situation arises where you need cash, you will find that you won’t be able to settle the Statement Balance prior to the Due Date and end up being a slave to the bank.

(4) If you do not have much savings and opt for 0% 12 months installment plan to purchase a non-durable item and just barely able to make full settlement of the Statement Balance before the Due Date to avoid being imposed interest. My advise is that you should forget about the non-durable item and instead invest the money so that you do not lose the opportunity of one year of your working life to accumulate wealth for your future.

Every sen saved will count towards a better future in your retirement years. By you simply saving RM300 every month and with the “magic of compound interest”, you will have RMxxx,xxx in 20 years time!!!

Seriously, if you do not have savings equivalent to the amount you require to survive for 6 months (essential expenses + car loan if any + housing loan if any) in the event you are jobless, do not sign up for any 0% installment plan. Shit Happens and we must be prepared for it. i.e. be kiasu or better still be kiasi, hahaha.

Lesson No.4 – The Best Credit Card in Malaysia is……

There is no such thing as the best credit card as each of us have different spending patterns. If you are new to credit cards, I would suggest you chose a FREE FOR LIFE credit card that earns you cash back from your essential expenses as mentioned in Lesson 1. There are only a few simple rules to follow when owning a credit card and they are mentioned in Lesson 2 (reducing your exposure to fraud) and Lesson 3 (you need to have discipline in controlling your spending).

In order to optimize or even maximize the returns we can get from credit cards, we need to hold the right cards. In addition to the Maybank 2 Gold/Platinum Cards and Public Bank Quantum Cards which I have touched on in Lesson 1, here are more examples:

If you shop frequently at AEON Big, then you should sign up for AEON Big Credit Card.

If you want FREE makan at airport lounges in KLIA or KLIA2 or worldwide, there are many FREE FOR LIFE credit cards that allow you to do so.

If you spend a lot of money at a particular establishment which you frequent, ask them if they offer any discount for any credit card. If yes, go get that credit card!

Generally the Maybank 2 Cards Premier is the best credit cards for accumulating air miles. If any of your friend tells you that his Citibank or HSBC or SCB credit cards are the best for air miles, they are a fool (but don’t tell them else they be pissed off with you). The only card that is better than the Maybank 2 Cards Premier (AMEX Reserve and Visa Infinite) for local and overseas spending is the RHB Premier Visa Infinite but only if you are into Enrich Miles.

Lesson No.5 – Best places to apply for a Maybank Credit Card.

If you reside in Klang Valley, I strongly recommend that you apply Maybank credit cards via their Maybank Card Centres (aka Maybankard Centre) located at One Utama New Wing or The Gardens (near to Robinson).

If you are new to Maybank, you are required to submit your income related documents and other relevant documents. So before you go to a Maybank Card Centre to apply for the new Maybank 2 Gold/Platinum Cards, call them and ask what documents you are required to bring along. So that you don’t need to waste time in the event you did not bring a relevant document.

Maybank Card Centre Contact Number @ The Gardens – 03-2288-8988

Maybank Card Centre Contact Number @ 1 Utama New Wing – 03-7728-5451

Please note, it makes a lot of difference on what documents Maybank requires from you, depending if you are a salaryman (with EPF – straight forward) or self employed (even a Director of a company where you are not paid a monthly fixed salary falls into this category).

If you apply for the Maybank 2 Gold/Platinum Cards at a Maybank Card Centre prior to lunch time on a working day, you may get your new Maybank 2 Gold/Platinum Cards cards within a few hours on the same day. However, for other cards, it may take several days.

The benefit of applying through a Maybank Card Centre is that you are ensured that your application will be expedited unlike applying through a branch where your documents may be misplaced by the bank officer or lost in the process.

And be kiasu like me, never ever give away your personal details to anyone who claims online (in forums, facebook, other social media or even ads) to be an agent for a particular bank unless you are looking forward to have a big gigantic headache.

For existing Maybank credit card holders, you can simply walk into Maybank Card Centre empty handed to apply for any other Maybank credit card of same level or lower.

On the other hand, you may have an existing Maybank Gold credit card which you applied many years ago but your income has since then jumped and you would like to apply for the Maybank 2 Cards Premier. Because Maybank has no records of your existing income, you may need to submit additional proof of income to satisfy the eligibility requirements.

Lesson No.6 – Final Lesson. Always read the T&C before applying for a credit card and never trust 100% what the sales person tells you because his/her only job is to entice you to sign up so that he/she can get commission. Same applies to websites promoting credit cards.

Last but not least, you should read the T&C before applying for any credit card. For years, most credit cards do not reward you any points for petrol. But now, more and more credit DO NOT reward you for transactions relating to Insurance, Government, Education and even Business related transactions. And many banks will mislead you by claiming that their cards are FREE FOR LIFE until you read the fine print which states that you need to spend X amount or swipe X times. FREE FOR LIFE means WITHOUT ANY CONDITIONS.

Oh yes, nowadays most of our Debit Cards and Credit Cards have PayWave and PayPass features where amount up to RM250 will be automatically approved without needing any Pin Number. PayWave and PayPass feature also enables one to clone our cards by simply holding a “reader/scanner” to steal info stored in our card(s). Therefore, I suggest you get yourself a RFID Safe/Blocking Wallet. Previously these wallets were made from Aluminum and were bulky; nowadays, we have leather wallets that are RFID Safe too.

I thank you for taking the FREE Express Financial Tuition and I hope what you have read will be useful/beneficial to you.

Another Personal Financial Tutorial by GenX

Another Personal Financial Tutorial by GenX